Think There’s a Strong Labor Market? Then Think Again

The number of hours worked suggests the Gross Domestic Income (GDI) recession view is the correct view.

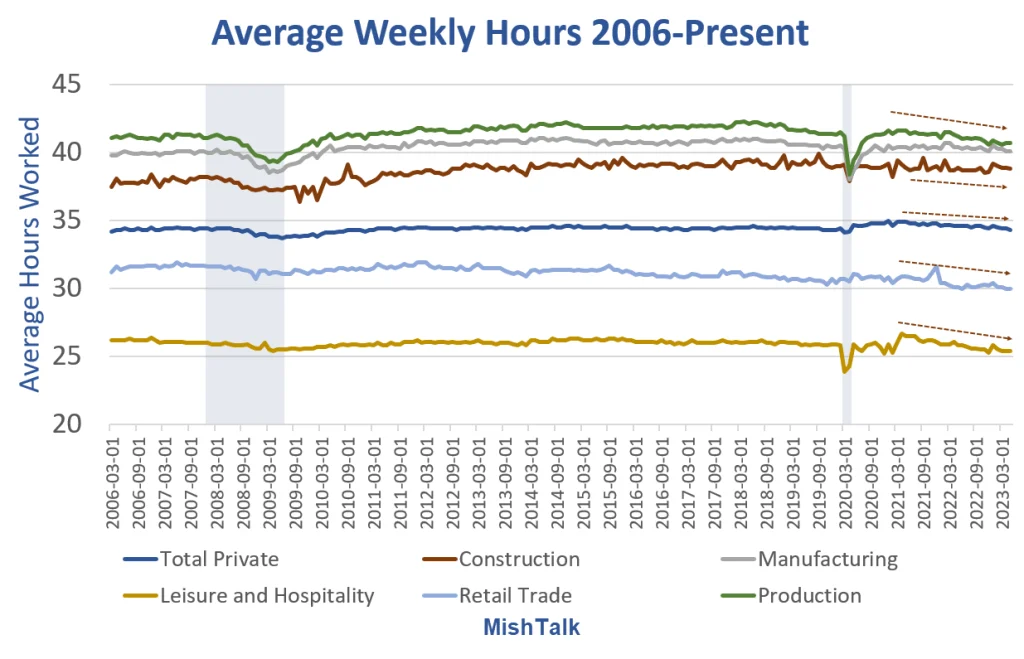

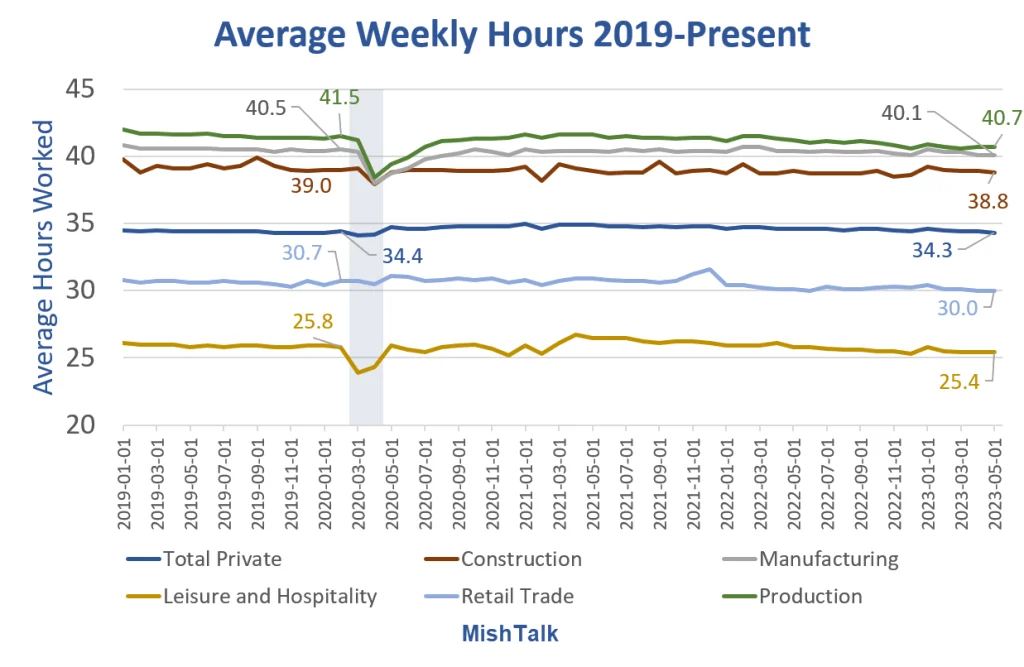

The economy is adding more workers, but they are working much fewer hours on average.

Average Weekly Hours 2019-Present

Across the board, people are working much fewer hours per week than pre-pandemic.

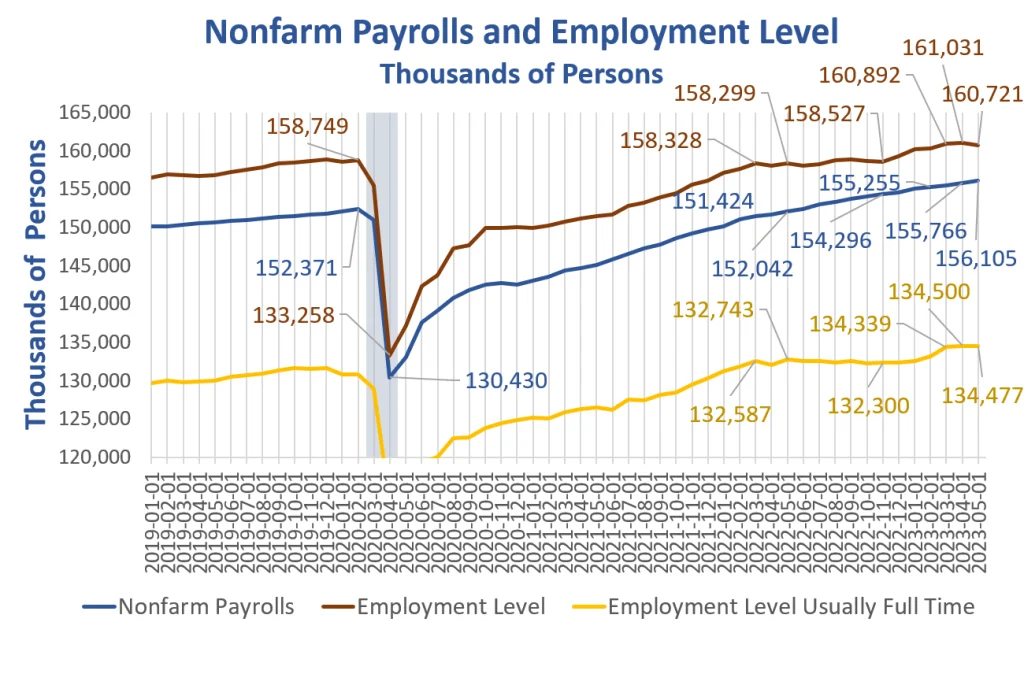

Huge Jobs Divergence Returns, Jobs +339,000 but Employment -310,000

On June 2, I noted Huge Jobs Divergence Returns, Jobs +339,000 but Employment -310,000

Payrolls vs Employment Since May 2022

- Nonfarm Payrolls: +4,063,000

- Employment Level: +2,422,000

- Full Time Employment: +1,734,000

Of the 894,000 rise in employment in January, 810,000 was due to annual benchmark revisions. And the BLS does not say what months were revised, just poof, here you go.

Noise? Where?

A prominent view is the household data is noise.

However, the number of hours worked and the full time data picture matches GDI.

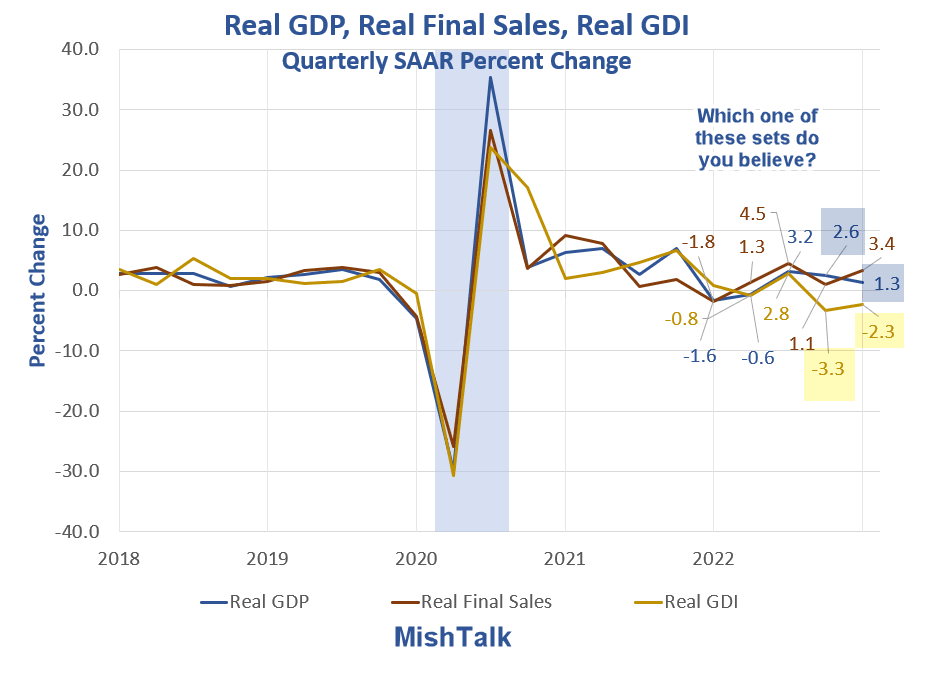

GDP vs GDI

Gross Domestic Income is Telling

- 2022 Q4 GDP: +2.6 Percent

- 2023 Q1 GDP: + 1.3 Percent

- 2022 Q4 GDI: -3.3 Percent

- 2023 Q1 GDI: -2.3 Percent

GDP vs GDI

Gross Domestic Income (GDI) and Gross Domestic Product (GDP) are two measures of the same thing.

They are supposed to match, and with upcoming revisions, they will.

But which way?

Revisions to the Downside

Heading into recessions, revisions are generally to the downside. Heading out of recessions revisions are to the upside.

GDI is very negative for 2 quarters. Hardly anyone discusses GDI but it is supposed to match GDP.

Revisions to GDP and jobs, will be to the downside.

Reckless Lending, Housing, and Recession Odds

For discussion of the GDP vs GDI and the strength of the economy, please see Conversation With a Friend on GDP, Reckless Lending, Housing, and Recession Odds

[ad_2]

Source link

US Beef Prices Hit Record High As Nation’s Cattle Herd Expected To Shrink Through 2025

Global Finance Chiefs to Plot Escape Routes for World Economy