“If You’re Not Scared Here…” – Lagarde Let Europe’s Genie Out Of The ‘Unintended-Consequence’ Bottle

As we detailed earlier, while most headlines are focused on stock market losses recently, a much more dangerous tidal wave of risk-awareness is spreading to peripheral European sovereign spreads (which are always far more susceptible to panic, and then pain).

We noted previously that there is a degree of cognitive dissonance at play (arguably because the market is so used to being precisely guided): Thursday’s statement was basically unchanged, and still included the familiar “present or lower levels” for rates forward guidance and pace of APP run down. For peripheral bonds this isn’t a rates lift-off play (although that’s an inevitable conclusion). This is an ongoing reaction to expectations for an earlier removal of the ECB’s bid — and one that seems to have legs.

And as those legs grow, something very ominous is back on the radar – EUR redenomination risk (the possibility of an exit from the Euro) is on the rise once again in CDS markets…

But, as Bloomberg’s Ven Ram writes, Lagarde has uncorked the genie from Europe’s bottle of unintended consequences.

Last week two-year German yields rose at a pace not seen in years, corporate spreads widened and rates volatility received a kickstart. In effect financial conditions tightened, contrary to the European Central Bank’s avowed intentions.

[ZH: That is a 9 sigma move compared to the last 6 years. Range past six years: 45bps; Range past six days: 41bps. This means risk-models (VaR) will be blowing out in every bank and fund.]

While the ECB’s statement from its policy first review of the year largely reiterated December guidance, President Christine Lagarde uncorked the genie by refusing to rule out a rate increase in her post-review remarks. It wasn’t as though she didn’t throw in sufficient disclaimers: “Don’t assume…immediacy, don’t assume too much.” Or that the ECB “will be faithful to sequencing.” Or even “we are not seeing wage increases as the market sees, we don’t see inflation spiraling.” And don’t forget, “We are not here to rock the boat.”

While it may feel like the markets’ reaction is overdone, they had every reason to — and it was unquestionably the right direction to walk in. If central banks don’t get why the markets are running away with an idea, they need to understand that standing in the middle of the road isn’t something that markets get.

For traders there are no ifs and buts. You can either buy bund futures or sell them, but I don’t yet know of a button that says “maybe, depending on what the data says and what other central banks do.” Markets have a pretty complicated job in pricing the future, and most of the time they do it with aplomb.

If central banks are going to recant their carefully laid-out stance in a matter of weeks — witness how inflation was pretty much as hot back in December (when Lagarde pretty much ruled out a hike this year) as it was with the latest available data print — then volatility is what they will get, and it will almost always go against what policy makers seek.

The tightening of policy conditions is hardly something the ECB would be willing to swallow, much less what it would have hoped to stoke before this month’s review.

Yet, there we are.

If your policy review uncorks so much volatility it means that either you haven’t articulated your stance well enough or the markets haven’t understood your conditionality.

Or it may be that fickle policy-making doesn’t go down well with traders.

So much for not rocking the boat.

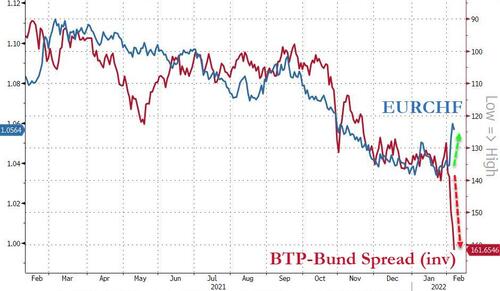

And talking of rocking the boat, another correlation regime imploded last week. Historically speaking, the wider the BTP-Bund spread, the more likely that investors will seek ‘safety’ of Swiss Francs relative to Euros. This last week has seen a dramatic decoupling of that relationship as investors bid for Euros (especially relative to USDs) as EU sovereign spreads exploded. Something’s gotta give there…

While the levels of redenomination risk, or sovereign spreads, remain considerably below the 2011/2012 crisis highs, this significant risk-flare-up puts the central bank saviors back in the spotlight. Simply put, there’s only so much risk re-pricing markets can make before central banks are required to reverse course.

We give the last word to former JPM and Salomon trader Nick Givanovic, who is just old enough to remember why the current market moves should raise the hairs on the back of investors’ necks:

If you are NOT scared here, it’s because you have no experience & have not experienced what could happen before. That’s the kindest way I can put it.

I am scared. And I have nearly 40 years of trading experience. All I can say is that tail risk is currently massive.— Nick Givanovic (@NickGiva) February 4, 2022

Givanoic goes to suggest “Do yourselves a favour, if you have significant positions, hedge up with some options. Both the left and the right tail could go in very rapid succession here.”

Given the sudden demand for credit protection (sovereign and corporate), we suspect the hedging has begun.

[ad_2]

Source link

Why we couldn’t be happier that gold is boring

Bitcoin Hits a Six-Week High as Financial Titans Step Up Crypto Initiatives