At Year End Its Trading Desk Owned 38 Percent of All 10-30 Year U.S. Treasuries

By Pam Martens and Russ Martens: May 26, 2022 ~

On Tuesday, the New York Fed’s trading desk released its annual report showing what it was up to in 2021. The New York Fed is the only one of the Federal Reserve’s 12 regional Fed banks to have a trading desk operation with speed dials to Wall Street’s trading houses, so we’re always interested in reading the “official” version of what’s been happening there.

The report is a deeply sanitized version of the facts on the ground. (For example, there is nothing in the report to indicate that the New York Fed has established a second trading floor near the futures exchange in Chicago.)

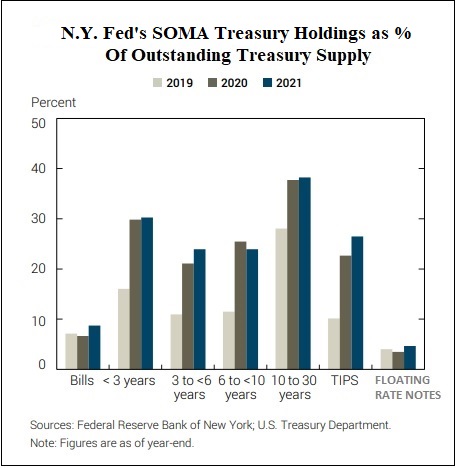

However, there is one paragraph in the newly-released report that took our breath away. It reveals that the New York Fed’s trading operation (officially called the System Open Market Account or SOMA) currently owns 38 percent of all outstanding U.S. Treasury Securities with 10 to 30 years remaining until maturity. (See the last two paragraphs on page 33 of the report.)

There are multiple reasons that this detail takes our breath away. First of all, the U.S. Treasury market is massive – at $22.6 trillion as of year-end 2021. That any one entity controls a big chunk of the market is deeply concerning. (The same report showed that the New York Fed’s trading desk owned 25 percent of all maturities of outstanding Treasury debt.)

The New York Fed’s trading desk owning 38 percent of the 10-30 year Treasuries is also deeply alarming because it is that maturity range that has a dramatic impact on the interest rate of the 30-year fixed-rate residential mortgage, the most popular mortgage among first-time homebuyers historically. It means that the New York Fed’s gobbling up of these 10-year U.S. Treasury Notes and 30-year U.S. Treasury Bonds, to the tune of 38 percent of the market, has created artificial demand for these instruments that would not otherwise exist. That, in turn, means that mortgage rates have been artificially held lower – much lower – than they would otherwise have been.

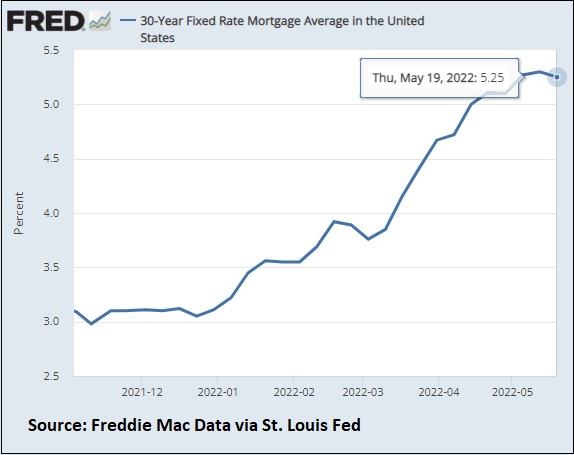

Even more alarming, it means that the recent announcements by the Fed that it will be reducing its purchases of Treasury securities and shrinking its balance sheet by reducing the amount of principal payments that are rolled over into new Treasury securities, is going to have a dramatic impact on residential mortgage rates.

The chart below shows how the 30-year fixed rate mortgage has risen since the Fed made its first announcement of QE tapering on November 3, 2021 and subsequent tapering announcements. The 30-year fixed rate mortgage has spiked from an average of 3 percent to 5.25 percent as of May 19 of this year – an increase of 75 percent. The dramatic spike in the rate over a period of just seven months has priced many first-time home buyers out of the market.

The Fed calls its purchases of Treasuries and other debt instruments “Quantitative Easing” or QE. The Fed embarked on three rounds of QE between 2008 and 2012 in an effort to stimulate the economy and get it back on a sound footing after Wall Street crashed the economy with its derivatives and subprime debt bombs in 2008.

When the repo market blew up in the fall of 2019, the New York Fed cranked up its QE operations again and ramped them up further when the pandemic hit in 2020. In June of 2020, the Fed began purchasing a total of $120 billion in debt securities each month, a larger amount than during the 2008 financial crisis.

The Fed’s balance sheet has grown from $924 billion on December 26, 2007 – prior to the financial crash of 2008 – to $8.99 trillion as of last Wednesday.

[ad_2]

Source link

MMT Alert! US Debt At $10.7 Trillion In Q4 2008, Now At $30.6 Trillion, +186% In 14 Years (M2 Money UP +162.5%) US Unfunded Liabilities At $172.4 TRILLION! – Confounded Interest – Anthony B. Sanders

15 Weakest Currencies in The World in 2024