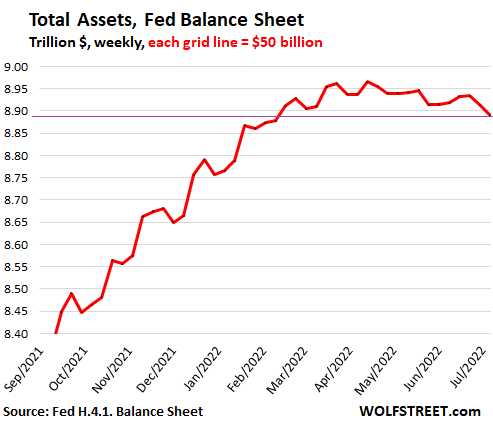

Fed’s QT Kicks Off: Total Assets Drop by $74 Billion from Peak, New Era Begins

QE creates money. QT does the opposite: it destroys money.

By Wolf Richter for WOLF STREET.

Total assets on the Fed’s weekly balance sheet as of July 6, released this afternoon, fell by $22 billion from the prior week, and by $74 billion from the peak in April, to $8.89 trillion, the lowest since February 9, as the Fed’s quantitative tightening (QT) has kicked off. The zigzag pattern is due to the peculiar nature of Mortgage Backed Securities (MBS) that we’ll get to in a moment.

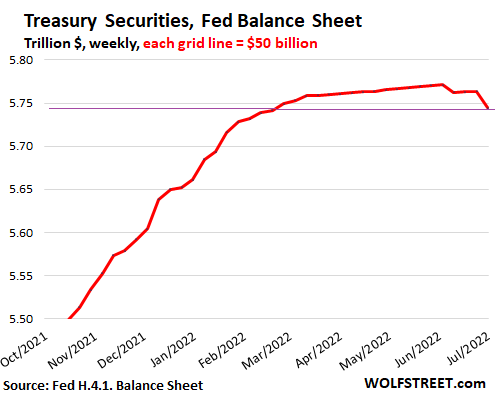

Treasury securities fell by $20 billion for the week, and by $27 billion from peak.

Run-offs: twice a month. Treasury notes and bonds mature mid-month and end of month, which is when they come off the Fed’s balance sheet, which in June was June 15th and June 30th.

Tightening deniers. Last week’s balance sheet was as of June 29 and didn’t include the June 30th run-off. However, the army of tightening-deniers trolling the internet and social media doesn’t know that, and so a week ago, they fanned out and announced that the Fed had already ended QT, or was backtracking on it, because Treasuries hadn’t dropped in two weeks, which was hilarious. Or more sinister: hedge funds manipulating markets through their minions?

Inflation compensation from TIPS adds to balance. Treasury Inflation-Protected Securities pay inflation compensation that is added to the face value of the TIPS (similar to the popular “I bonds”). So if you hold a fixed number of TIPS, their face value will rise with the amount of the inflation compensation. When they mature, you will receive the total amount of original face value plus inflation compensation.

The Fed holds $384 billion in TIPS at original face value. It has received $92 billion of inflation compensation on those TIPS. This inflation compensation increased its holdings of TIPS to $476 billion.

Over the month of June, inflation compensation increased by $4 billion. In other words, until those TIPS mature and run off the balance sheet, the Fed’s holdings of TIPS will increase by the amount of inflation compensation – currently around $1-1.5 billion a week!

No TIPS matured in June. But next week, July 15, TIPS with an original face value of $9.6 billion plus $2.5 billion in inflation compensation will mature, for a total of $12.1 billion, that the Fed will get paid. After that, the next maturity of TIPS on the Fed’s balance sheet is on January 15, 2023. And the TIPS balance will increase from July 15 through January 15 due to inflation compensation.

The thing to remember about the Fed’s TIPS is that the inflation compensation is added to the balance of TIPS and therefore to the balance of Treasury securities, at around $1-1.5 billion a week currently.

The balance of Treasury securities fell by $20 billion from the prior week and by $27 billion from the peak on June 8, to $5.74 trillion, the lowest since February 23:

- Note the two run-offs on the balance sheets on June 16 and today.

- Note the small steady increase of around $1-1.5 billion a week after QE had ended from mid-March into June, which is the inflation compensation from TIPS.

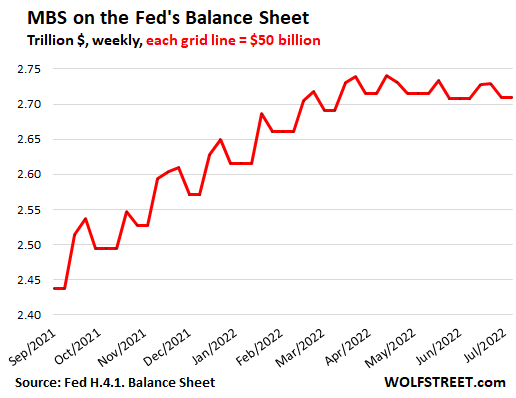

MBS fell by $31 billion from peak.

Pass-through principal payments. Holders of MBS receive pass-through principal payments when the underlying mortgages are paid off after the home is sold or the mortgage is refinanced, and when mortgage payments are made. As a passthrough principal payment is made, the balance of the MBS shrinks by that amount. These pass-through principal payments are uneven and unpredictable.

Purchases in the TBA market and delayed settlement. During QE, and to a much lesser extent during the taper, and to a minuscule extent now, the Fed tries to keep the balance of MBS from shrinking too fast by buying MBS in the “To Be Announced” (TBA) market. But purchases in the TBA market take one to three months to settle. The Fed books its trades after they settle. So the purchases included in any balance sheet were made one to three months earlier.

This delay is why it takes months for MBS balance to reflect the Fed’s current purchases. The purchases we san show up on the balance sheet in June were made somewhere around March and April.

And these purchases are not aligned with the pass-through principal payments that the Fed receives. This misalignment creates the ups and downs of the MBS balance, that also carries through to the overall balance sheet.

In addition, MBS may also get called by the issuer (such as Fannie Mae) when the principal balance has shrunk so much that it’s not worth maintaining the MBS (the issuer then repackages the remaining underlying mortgages into new MBS).

Tightening deniers. So when the tightening-deniers – including a hedge-fund guy with a big Twitter following – trolled the internet and the social media about QT not happening because MBS balance ticked up by $1.2 billion on the June 23 balance sheet, they got tangled up in their own underwear. The following week, the MBS balance fell by $19.5 billion. That’s how MBS on the Fed’s balance sheet work. These folks just didn’t know, or more insidiously, tried to manipulate the markets.

The thing to remember about the Fed’s MBS balance is that it declines due to pass-through principal payments, and occasionally because they’re called, and this is an uneven process.

The Fed’s MBS holdings fell by $31 billion from the peak.

The up-moves in the balance come from purchases in the TBA market during the phase after QE and before QT, when the Fed was trying to keep the MBS balances flat. It has since reduced those purchases to small amounts, but they won’t show up for a couple of months. When they do show up, the up-moves will be much smaller, and will eventually vanish, and only the down-move will continue, and the overall balance will drop faster:

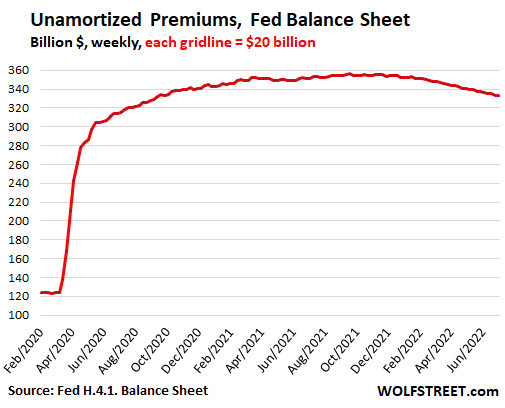

Unamortized Premiums declined.

Unamortized premiums accounts for the amount that the Fed paid in “premiums” over face value when it purchased Treasury securities, MBS, and agency securities in the market.

Bond buyers, including me and the Fed, have to pay a premium to buy securities if the coupon interest rate exceeds the market yield at the time of purchase.

But unlike me, the Fed books securities at face value and books the premiums in a separate account on its balance sheet. This adds some transparency. The Fed amortizes the premium to zero over the life of the bond, against the higher coupon interest payments. By the time the bond matures, the premium has been fully amortized, and the Fed receives face value and the bond comes off the balance sheet.

The unamortized premiums peaked with the beginning of the taper in November 2021 at $356 billion and have now declined by $23 billion to $333 billion:

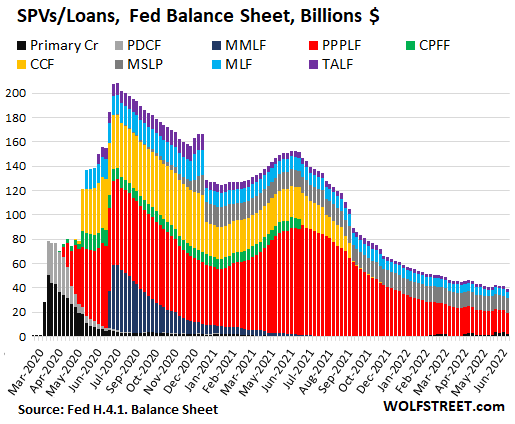

The SPV creatures almost gone.

The Fed set up the Special Purpose Vehicles (SPVs) during the crisis to do QE with assets that it was not allowed to buy otherwise. Equity funding was provided by the Treasury Department. The Fed lent to the SPVs, and shows these loans plus the equity funding from the Treasury Dept. in these SPV accounts.

Four of the eight SPVs have been completely unwound by now, and their balance has been zero.

The PPP loans that the Fed bought from the banks fell to $18 billion and account for about half of the total SPVs. The remainder: Main Street Lending Program ($12 billion), Municipal Liquidity Facility ($7 billion), and TALF ($2 billion). Also listed is the account for Primary Credit (less than $2 billion). For a total of $39 billion, down from $208 billion in July 2020.

QE creates money. QT does the opposite: it destroys money.

With QE, the Fed creates money that it then pumps into the financial markets via its primary dealers, and this money is used to purchase assets, and as this money chases assets, it inflates asset prices of all kinds, which means it drives down long-term interest rates, including mortgage rates, which further inflates home prices, etc. This is the officially stated reason for deploying QE.

With QT, the Fed does the opposite. QT reverses QE. QT destroys some of the money that QE had created, with opposite effect on yields and asset prices, and home prices, etc., driving up long-term interest rates and deflating asset prices.

The Fed is now tightening its policies – raising rates and kicking off QT – because inflation has exploded to a 40-year high, has spread across the economy and deeply into services, and is becoming solidly entrenched. This inflation is in part a result of QE. And QT is one of the tools the Fed is using to crack down on inflation.

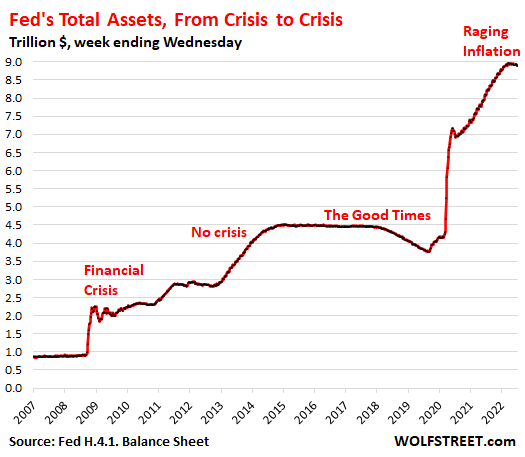

The Fed’s assets from crisis to crisis – money-printing comes home to roost:

In the 15 years of this chart, there are two crises: the Financial Crisis and now the inflation crisis. Today’s inflation crisis pulls into the opposite direction of the Financial Crisis, and dealing with it will require the opposite tools:

Enjoy reading WOLF STREET and want to support it? Using ad blockers – I totally get why – but want to support the site? You can donate. I appreciate it immensely. Click on the beer and iced-tea mug to find out how:

Would you like to be notified via email when WOLF STREET publishes a new article? Sign up here.

![]()

[ad_2]

Source link

Conference Board Confidence Slides In January, Inflation Expectations Rebounded

What would happen if financial markets crashed?