Now Inflation Is the Millennials’ Fault! Or Is It?

Putin is causing inflation. Greedy corporations are causing inflation. COVID-19 caused inflation. We hear all kinds of reasons for the recent spike in prices. And now we have a new one. It’s the millennials’ fault.

This is all wrong and it illustrates the problem with redefining inflation to be something it isn’t.

Smead Capital Investment chief investment officer Bill Smead told CNBC the size of the millennial generation is causing inflation.

“See, what everyone is not including in the conversation is what really causes inflation, which is too many people with too much money chasing too few goods,” he said, explaining that there are roughly 92 million millennials.

“So we have in the United States a whole lot of people, 27 to 42, who postponed home buying, car buying, for about seven years later than most generations. But in the past two years, they’ve all entered the party together,” he said.

Smead actually gets closer to the cause of inflation than most. He at least recognizes that more dollars chasing the same amount of goods and services causes prices to rise. But he leaves the key question unanswered – where are these people getting all of these extra dollars?

If the number of dollars along with the number of goods and services in the system remained stable, rising spending by one generation would necessarily correlate with declining spending in others. As millennials consumed more stuff, there would be less stuff for other people in the other generations to purchase. Prices would remain stable.

More realistically, the larger generation would produce more stuff, adding to the inventory of goods and services. In a stable monetary environment, prices would generally fall as the larger generation produced additional wealth.

But as Smead explains it, the millennials apparently aren’t producing more. But somehow they have more dollars. Meanwhile, every other generation still has the same number of dollars and they continue to spend at the same pace. Therefore we have all of these extra millennial dollars chasing the same amount of stuff.

Viola — inflation!

But it seems like maybe Smead is leaving out a key player in this scenario.

He is — the Federal Reserve.

The only way millennials can have more dollars without taking dollars from other generations is if somebody is creating new dollars. That somebody, of course, is the Fed.

The Root of the Problem

Somehow, the Fed manages to escape scrutiny in any mainstream discussion of inflation. But the central bank is the root of the problem.

The Fed creating trillions of dollars out of thin air over the last couple of years and injecting them into the economy is the primary reason we see consumer prices spiking through the roof today. Yes, oil price shocks, supply chain issues and other factors drive up prices in certain sectors, but the Fed monetary policy lies behind the more general rise in prices.

The federal government also played a role. In the first place, the US government needed the Fed to monetize its pandemic borrowing and spending spree. Meanwhile, both Trump and Biden administrations took a lot of the newly created money and showered it on consumers with stimulus checks. That put money in people’s pockets even as they were sitting at home producing nothing.

So, how did millennials spend a bunch of money while they weren’t working? The Fed “printed” it and the government gave it to them.

The Fed is the engine that drives it all. The central bank creates the dollars. Without all of those extra dollars, people couldn’t have “too much money” to chase too few goods, as Smead explains it.

One question remains — how does the Fed manage to get off scot-free in every inflation discussion when its policies drive inflation?

Because the politicians, bureaucrats, central bankers and mainstream media pundits have successfully redefined inflation.

Getting the Definition Right

When people use the term “inflation” today, they mean rising consumer prices as measured by the Consumer Price Index (CPI). You’ll often hear CPI referred to as “an inflation measure.”

But rising prices aren’t inflation. They are a symptom of inflation.

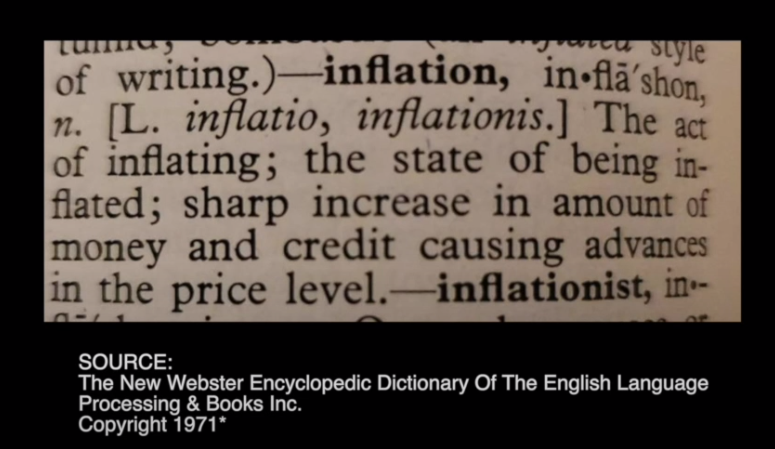

Look at this definition of inflation from a 1971 dictionary.

Notice that the definition mentions rising prices, but only as a symptom of inflation. Inflation itself is defined as “an increase in the amount of money and credit.”

Over the years, the government, along with its apologists in the corporate media and academia, altered the definition to suit government purposes. The standard definition of inflation bandied about today is nothing more than government propaganda.

Why does the government want to define inflation as rising prices?

Because the modern definition allows policymakers to shift the blame. If we use the original definition of inflation as an “expansion of the supply of money,” the culprit becomes clear. Who expands the supply of money? It’s the Fed and the government. So, if you accurately define inflation, you know exactly who’s to blame. But if the government can fool people into believing that an effect of inflation is inflation, they can blame it on whoever, or whatever, is raising the prices – Putin, pandemics and apparently millennials.

The original definition of inflation is the key to understanding inflation. When you misdefine inflation as rising prices, bad monetary policy and bad fiscal policy go on unchallenged.

The inflation blame game is great for the powers that be. It’s not so great for you or me.

Get Peter Schiff’s most important gold headlines once per week – click here – for a free subscription to his exclusive weekly email updates.

Interested in learning how to buy gold and buy silver?

Call 1-888-GOLD-160 and speak with a Precious Metals Specialist today!

[ad_2]

Source link

As Ukraine war drags on, Europe’s economy succumbs to crisis

Fed Officials Lean Into Higher Rates as Inflation Keeps Going