People Trying to Dodge Legal Usury: Credit Card Balances, Delinquencies, Third-Party Collections, and Bankruptcies in Q2

Buy-Now-Pay-Later (BNPL) Lenders Face Tougher Reality.

By Wolf Richter for WOLF STREET.

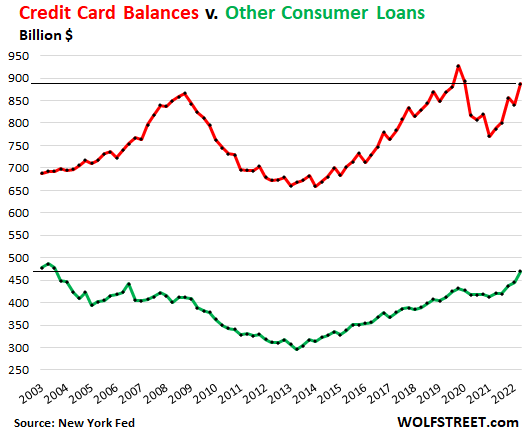

Credit card balances jumped by $46 billion to $887 billion in the second quarter, which was still down by 4.3% from the peak in Q4 2019 and was just a hair above where they had been in 2008, despite 14 years of population growth and inflation. Raging inflation is responsible for much of the increase in Q2, according to the New York Fed’s Household Debt and Credit Report.

Credit card balances also include balances that are paid off at due date the next month, every month, so that no interest accrues. Many Americans use credit cards purely as a payment method (and to collect the 1.5% cash-back or whatever), and not as a borrowing method.

A report from Fitch estimated that the total amount paid with credit cards for goods and services – in the US reached $4.6 trillion in 2021, which would be an average of $1.15 trillion in purchases via credit cards per quarter.

Yet the total credit card balances outstanding in Q2 only grew by $46 billion, which shows to what massive extent credit cards are used as payment method, and to what small extent they’re used as borrowing method, which makes sense, given the usurious interest rates.

The credit card balances of $887 billion in Q2 include transactions incurred roughly in June but paid off in July that are not accruing interest. And this was boosted by the surge in traveling, much of which is paid for with credit cards.

Other consumer loans, such as personal loans, payday loans, and Buy-Now-Pay-Later (BNPL) loans, all combined, rose to $470 billion in Q2, below where they’d been 20 years ago, despite 20 years of inflation and population growth.

Trying to dodge rip-off usurious interest rates: Dwindling importance of credit card debt.

People are borrowing lots of money to finance home purchases and auto purchases where loan balances have shot higher compared to 2008; and they’re taking out lots of student loans, whose balances have spiked since 2008.

But in order to dodge getting ripped off by usurious interest rates, people are practically restrained when it comes to carrying interest-bearing debt on credit cards – shown by the huge amounts that are getting spent via credit cards, nearly all of which get paid in full every month and never accrue interest: Last year, $4.6 trillion was spent on credit cards, and yet, credit card balances only grew by $40 billion over the same period.

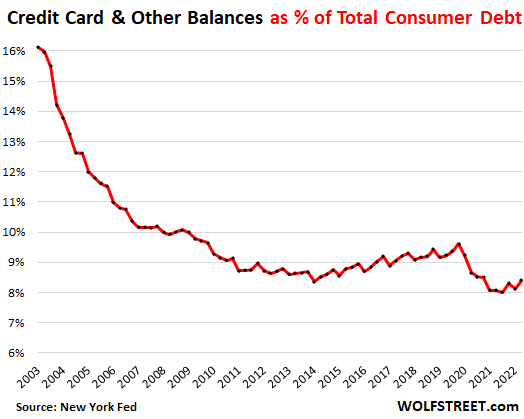

In 2003, credit card balances and other loans combined amounted to over 16% of total consumer debt (including mortgages, auto loans, student loans). During the pandemic, this dropped to the 8% range for the first time and ticked up to 8.4% of total debt in Q2:

A word about Buy Now Pay Later (BNPL)

The New York Fed’s data does not break BNPL loans out. But Fitch estimates that in 2021, $43 billion (with a B) in purchases were made using BNPL loans – compared to $4.6 trillion (with a T) in US credit card purchases. So BNPL loans are minuscule, but growing rapidly.

BNPL loans, which often cater to subprime-rated customers, are short-term installment loans, such as one payment down, three more to go, typically spread over six to eight weeks. These loans are often issued at the point of purchase. They typically carry 0% interest, and are subsidized by the retailer to encourage larger average tickets and fewer cart abandonments. Retailers may partner with a BNPL lender.

If this sounds like the installment plans from decades ago, it’s because that’s what it is, but now imbued with the infallible aura of FinTech and AI.

One of the most hyped specialized BNPL lenders in the US is Affirm Holdings [AFRM], a startup with less than $1 billion in revenue in 2021. It went public in January 2021 amid immense hoopla. In October, its shares hit $176.65 after which they plunged through the IPO price of $49 a share, and today closed at $31.55 a share, down by 82% from the high.

The company has lost oodles of money every quarter, including $55 million in Q1, and $430 million last year.

According to Fitch, the BNPL lenders “have seen delinquency rates more than double over the past few quarters,” while credit card delinquency rates have barely ticked up, as the subprime rated customers that take out BNPL loans are most impacted by the raging inflation.

And as so many times with infallible FinTech and AI, the credit checks are only as good as the folks that wrote the code, and apparently, the code was designed to maximize revenues and not to control risks. Thankfully, this is just a tiny portion of the consumer credit scenario.

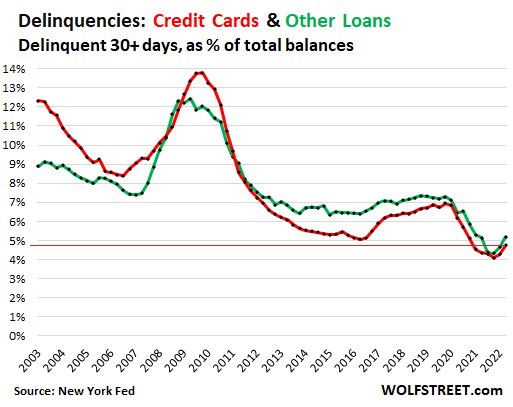

Credit card delinquencies rise from record lows, remain low.

There is still lots of cash floating around, but some people are starting to run low. In 2020 and 2021, people used their stimulus checks and PPP loans, and the extra unemployment benefits plus some of the cash left over from not having to make rent or mortgage payments, to get current on their credit cards. And delinquency rates across the board dropped to record lows. For credit card delinquencies, that record low was in Q3 2021, when balances that were 30 days or more delinquent fell to 4.1% of total credit card balances. Then they started rising.

In Q2, credit card delinquencies of 30+ days rose to 4.8% of total credit card balances, which was still lower than any pre-pandemic low point.

For “other loans,” the 30+ day delinquency rate In Q2 rose to 5.2% of total “other” balances (the record low was in Q4 2021, at 4.3%).

In both categories, delinquency rates are rising but are still below the Good-Times normal. Credit card delinquencies are rising faster and may soon reach the Good-Times normal, and then the not-so-good-times normal. A major employment crisis, such as during the Great Recession, will entail a large increase.

Note how the pandemic stimulus payments of all kinds, and the ability to skip rent and mortgage payments, have pushed down the delinquency rates through mid-2021. But that game is now over, and there’s a trip back to reality. This is a very similar trajectory to auto loan delinquency rates:

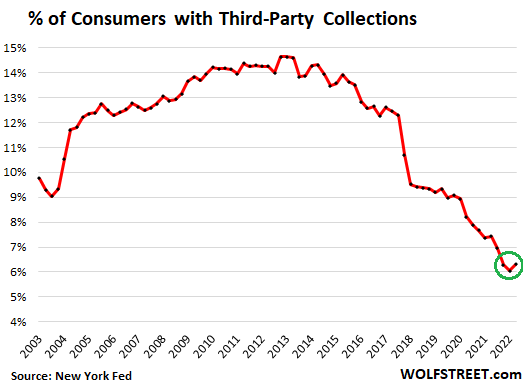

And the first uptick in third-party collections.

The percentage of consumers with third-party collections rose to 6.3% in Q2, less than half of where it had been in 2013 (14.6%). So far, so good:

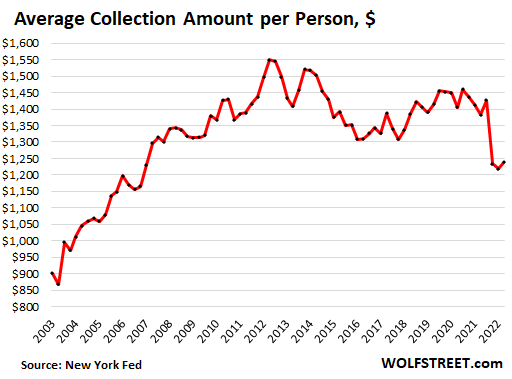

The average amount of collections per person remained roughly stable at around $1,230 for the past three quarters, after the decline during the stimulus era:

Bankruptcies

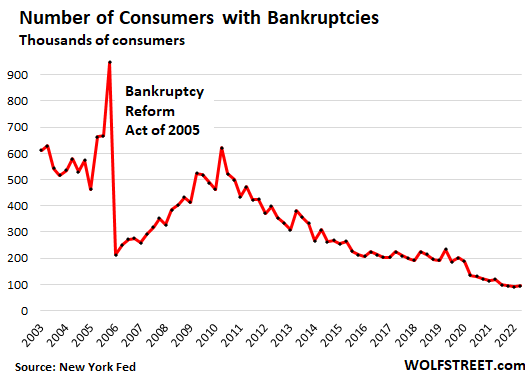

The number of consumers with new bankruptcy filings in Q2 ticked up a hair to 95,200 but remains at historic lows, after the long down-trend that started in 2010 when bankruptcies peaked during the Great Recession. Also note that the number of people filing for bankruptcy in Q2 was less than half the number filing in 2006, the low point just ahead of the Great Recession.

Enjoy reading WOLF STREET and want to support it? Using ad blockers – I totally get why – but want to support the site? You can donate. I appreciate it immensely. Click on the beer and iced-tea mug to find out how:

Would you like to be notified via email when WOLF STREET publishes a new article? Sign up here.

![]()

[ad_2]

Source link

ETFs Add More Gold in April; Total Holdings Just Shy of Record

$491,900,000,000 in US Treasuries Dumped by China in a Decade As Country’s US Debt Holdings Hit 14-Year Low