Treasury Yields Of 5% Coming to Your Screen Soon?

By Ven Ram, Bloomberg Markets Live commentator and reporter

Sometimes, just sometimes, the markets want to hear what they want to and discard what seems discordant — even if policymakers keep hammering home the same message.

And so it was on Monday when Federal Reserve speakers let traders know that they were underestimating their intent on how far rates may climb in this cycle. Fed St. Louis President James Bullard, who has often been an accurate bellwether for where benchmark rates are headed, put it bluntly:

-

The Fed needs to get to the bottom end of the 5%-7% range;

-

Markets are underpricing the risk that the policy committee may be more aggressive; and

-

The Fed needs to move farther into restrictive territory

His New York counterpart, John Williams, followed up with remarks that the Fed will need to stick with a restrictive policy through next year, meaning a rate cut — contrary to market expectations — is unlikely before 2024. For good measure, he has revised up his rate trajectory since the September dot plot.

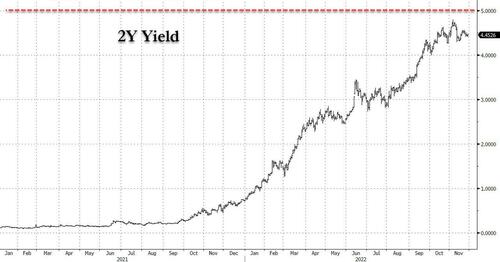

Despite those reminders, Treasuries seem to be singing from a different hymn sheet of late. Two-year yields have basically sleepwalked through November, while 10-year Treasuries have rallied on conviction that the economy is wilting. It’s the reaction at the front end of the curve that seems particularly jarring. Front-end Treasuries don’t seem to give one the impression that they are quite priced for a terminal rate that may be higher than 5%.

Analysis shows that the differential between front-end yields and the Fed’s benchmark has always been positive before the conclusion of monetary tightening. And the Fed hasn’t been able to conclude its tightening cycle before the real funds rates is significantly positive — and at the moment we are at around -1%.

Given all the concerns about the strength of the economy, long-dated Treasuries may still be relatively better bid, but the front end could come for a re-assessment in the days to come.

[ad_2]

Source link

Energy, inflation crises risk pushing big economies into recession: OECD

NASAQ Index Plunges 4% On Fed’s Inability To Cool Inflation (Gimme Some Quantitative Tightening!) – Confounded Interest – Anthony B. Sanders