America is drunk on credit–and polarized politics complicate the Fed’s unenviable challenge of ending easy money

I would not want to be in the seat of Federal Reserve chair Jerome Powell. Whether the Fed continues to hike interest rates or not, Powell will be blamed for a recession that is almost inevitable at this point.

The savings that Americans accumulated during the pandemic and the money the government handed out in various ways (stimulus, loan forbearance, tax credits) are gone, and the country is–yet again–drunk on credit.

So much credit that credit-card debt is nearing $1 trillion and, according to Stansberry Research, mortgage credit is growing at an annual rate that is similar to the years leading up to the financial catastrophe of 2008.

The problem is that the Fed started to hike interest rates more than a year ago when it realized that the many years (if not decades) of Fed-induced easy money had finally caused inflation to take off. Inflation had been evident in other parts of the economy but prices took a while to directly affect all consumer products. Now, with households submerged in debt, the prospect of new interest rate hikes to tame an inflation rate that is still nearing 6% officially (while in real life several key items are experiencing much higher price increases) is terrifying.

Many politicians are warning the Fed against maintaining its anti-inflationary policy–but inflation erodes the consumer’s finances just as much as too much debt (the two are related), putting Mr. Powell in that most unenviable position: damned if you do, damned if you don’t.

According to a Bankrate report, more than a third of households have more credit-card debt than savings for emergency situations. Almost 70% would not be able to pay for one month’s worth of living expenses if they lost their main source of income. The number of people who are at least two months late making their auto loan payments is up by 20% compared to last year, according to Cox Automotive. Clearly, American consumers, who had been forced by the Covid lockdown to remember what it was like to save money, decided, once the economy opened up, that they were invulnerable once again. After all, they were awash in cash–from their forced savings and the various forms of fiscal and monetary stimulus.

All of this leads to one conclusion: American consumers are going to stop buying soon, and many U.S. corporations and small businesses are going to suffer. The notion that you can wash over the excesses of the economy–of which too much credit and inflation are symptoms–with just one year of interest rate hikes is ludicrous.

Recessions are the inevitable way of purging those excesses and getting back on track. The U.S. economy has been living in la-la-land for far too long. The conundrum in which the Fed finds itself is the result of four decades of easy credit and, therefore, too much debt and too much spending, a large part of which was facilitated by the Federal Reserve itself.

The Fed would do well to remember this now that it is under so much political pressure.

The Fed needs to continue to reduce its crazy balance sheet (by at least $95 billion per month, as in recent months) and raise real interest rates. They are still in negative territory if you factor in inflation, meaning that they are far from where they need to be in order to restore some sanity to the monetary system and the economy.

Just look back at the fabled Paul Volcker years (1979-87) at the Fed. He inherited a stagnant economy, coupled with high inflation–“stagflation.” And it took severe rate hikes and a tough recession for the economy to regain its health in early 1986, more than six years after Volcker assumed the Fed’s helm.

Hanging over the current economy, of course, is the next presidential election. No time is good for politicians to accept–and endorse–the hard realities of economic life, much less when populism has such an overwhelming presence in both political parties and is likely to play a major role in the primaries.

If the economy tanks in the months ahead, Powell will get the blame. If we avoid a recession, the politicians will claim credit.

Álvaro Vargas Llosa is a senior fellow of the Independent Institute. His latest book is Global Crossings: Immigration, Civilization and America.

The opinions expressed in Fortune.com commentary pieces are solely the views of their authors and do not necessarily reflect the opinions and beliefs of Fortune.

More must-read commentary published by Fortune:

[ad_2]

Source link

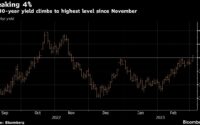

Entire Treasury Market Yields at Least 4%, Now Including 30-Year

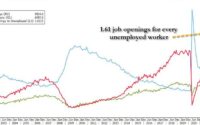

Job Openings Tumble By 500K Even as Number Of Quits Unexpectedly Soars