Higher Interest Rates and the National Debt

Mar 16, 2022

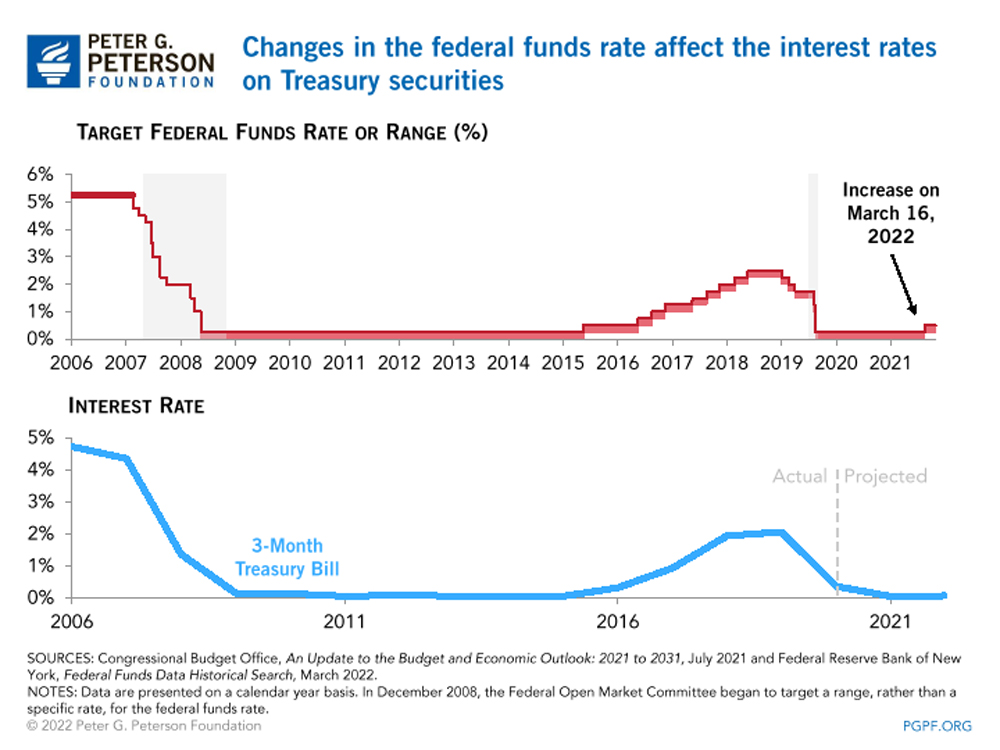

Today, the Federal Reserve announced an increase in the target for the federal funds rate to between 0.25 and 0.50 percent after holding the rate close to zero since the onset of the pandemic to help the economy recover. The increase is meant to help tame rising inflation; however, any changes in interest rates will also have implications for the federal government’s borrowing costs and therefore the nation’s fiscal picture.

Setting the target for the federal funds rate — the interest rate at which commercial banks lend to each other overnight — is an important tool for the Federal Reserve. That rate is the benchmark for Treasury bills and other short-term securities. Expectations about those short-term rates, combined with other factors, may also affect longer-term rates.

TWEET THIS

As interest rates on U.S. Treasury securities rise, so too will the federal government’s borrowing costs. The United States has been able to borrow cheaply to respond to the pandemic because interest rates were historically low. However, as the Federal Reserve increases the federal funds rate, short-term rates on Treasury securities will rise as well — making some federal borrowing more expensive.

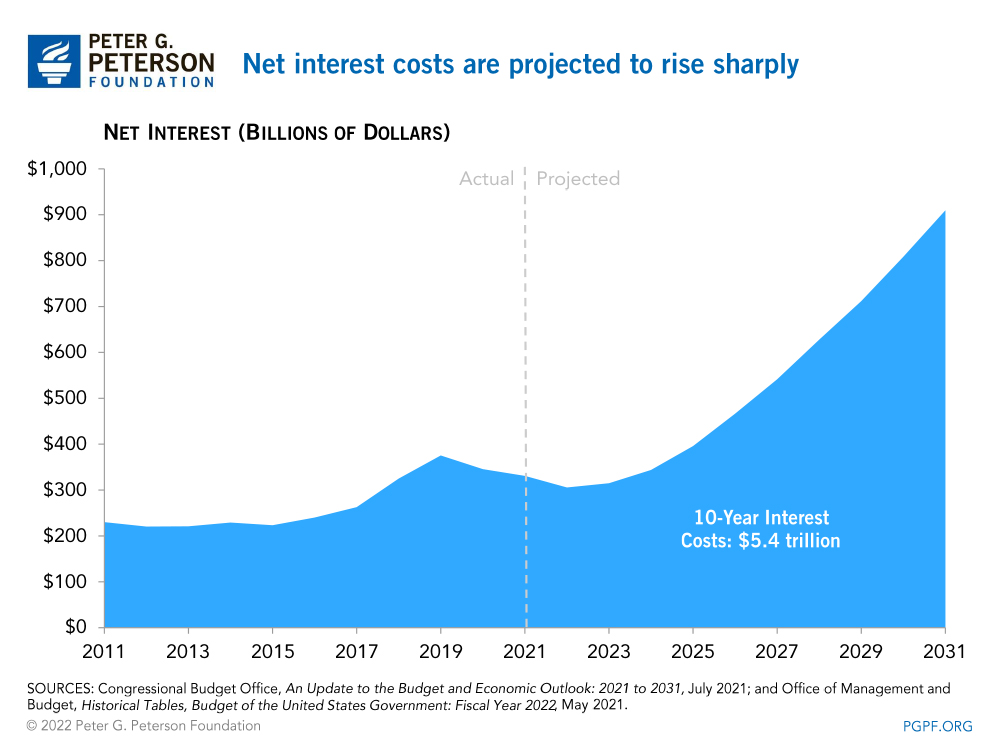

Last year, the Congressional Budget Office (CBO) projected that annual net interest costs would nearly triple over the 2022 – 2031 period, soaring from $306 billion to $910 billion and totaling $5.4 trillion over that period. However, inflation has been much higher than CBO’s projections and the Fed is raising interest rates earlier than the agency projected last year, so such costs may rise even faster than anticipated. For example, interest costs in 2021 were around $20 billion higher than the agency projected last year, and such costs through the first five months of this fiscal year are outpacing interest costs through the same period one year ago by $30 billion.

TWEET THIS

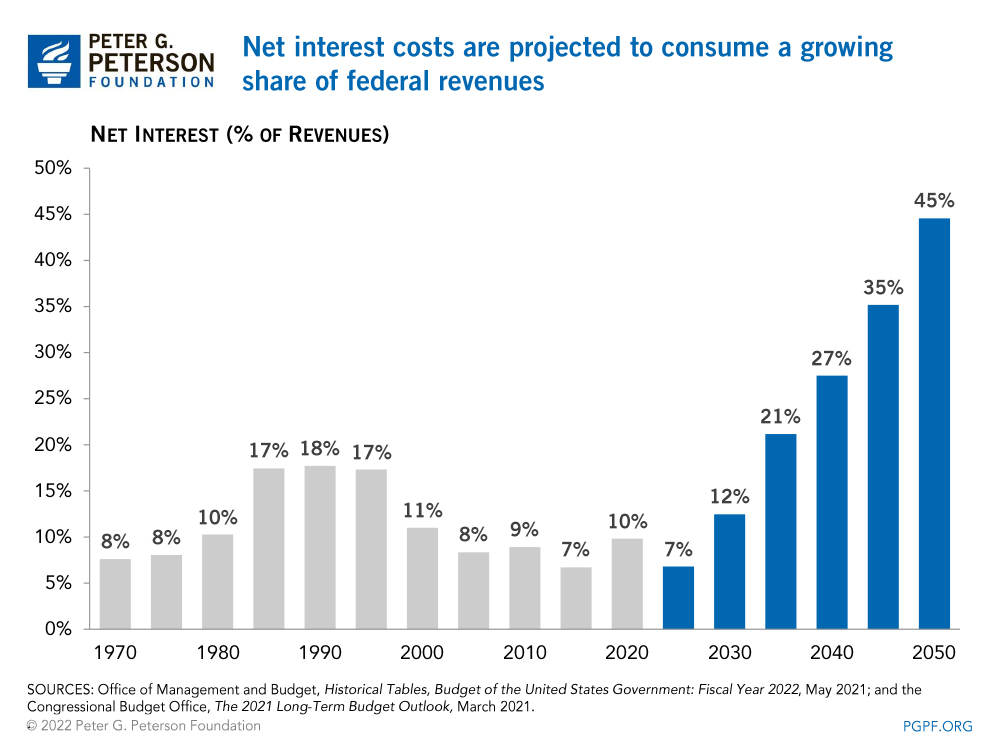

The growth in interest costs presents a significant challenge in the long-term as well. According to CBO’s latest projections, interest payments would total around $60 trillion over the next 30 years and would take up nearly one-half of all federal revenues by 2050. Interest costs would also become the largest “program” over the next few decades — surpassing all discretionary spending in 2043, Medicare in 2043, and Social Security in 2045.

TWEET THIS

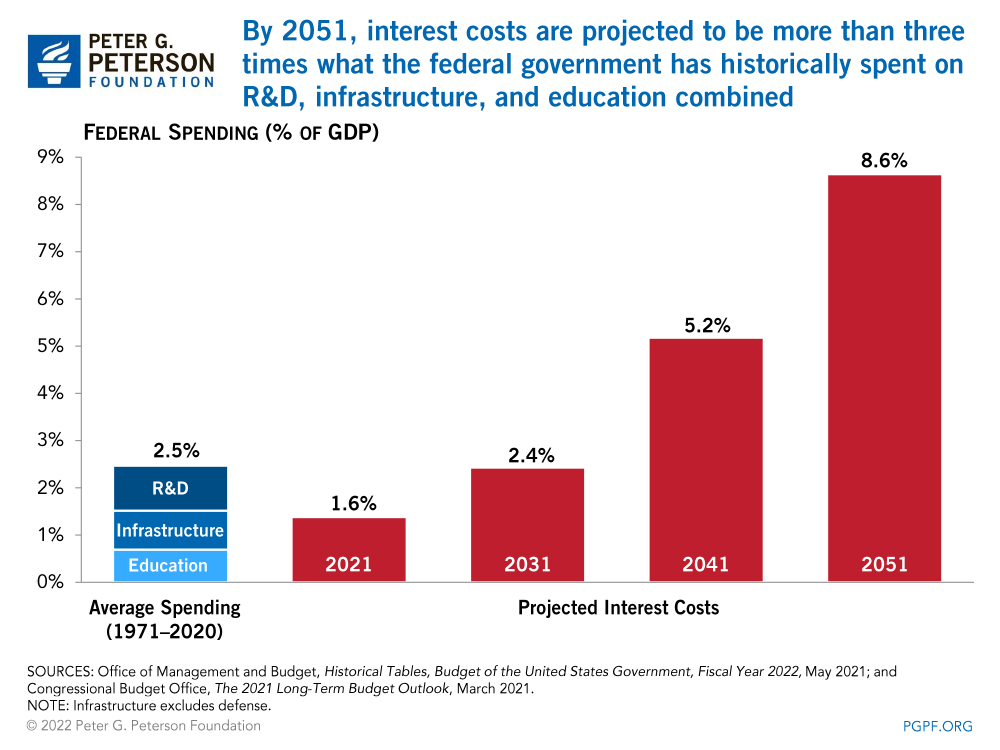

Ballooning interest costs threaten to crowd out important public investments that can fuel economic growth in the future. In their most recent long-term budget report, CBO estimates that by 2051, interest costs are projected to be more than three times what the federal government has historically spent on R&D, nondefense infrastructure, and education, combined.

TWEET THIS

The long-term fiscal challenges facing the United States are serious. Significant borrowing was necessary to respond to the COVID-19 pandemic; however, the structural imbalance between spending and revenues that existed before the pandemic is still large and will grow rapidly in the future. Furthermore, as interest rates rise and the nation’s debt grows, it will become even more expensive to borrow in the future. Congresses and Presidents of both parties, over many years, have avoided making hard choices about our budget and failed to put it on a sustainable path. It is vital for lawmakers to take action on the growing debt to ensure a stable economic future.

[ad_2]

Source link

Gold, Bitcoin Pop After U.S. CPI Data

The Deflating “Inflation Narrative” Stock Market (and Sentiment Results)…