Consumers Can Handle Fed Tightening: Their Debts, Delinquencies, Foreclosures, Collections, and Bankruptcies

But the first upticks in delinquencies from breath-taking record lows are cropping up.

By Wolf Richter for WOLF STREET.

Americans are exiting the weirdest economy ever, a two-year period where the Fed threw $4.7 trillion in printed money at the financial markets, thereby inflating further the greatest Everything Bubble ever, printing millionaires and billionaires on a daily basis; and where the federal government threw $6.6 trillion in borrowed money directly at consumers, businesses, and state governments, topped off by wide-reaching forbearance programs for mortgages and student loans, along with eviction bans.

But now, it’s over. It’s the next morning and bad breath: The worst CPI inflation in 40 years, spiking interest rates to deal with this inflation, and deflating asset bubbles. The hot air is already hissing out of stocks, bonds, and cryptos; and housing, which is very slow moving, is getting in line.

So here’s how consumers are exiting the free-money and credit paradise, based on today’s data from the New York Fed’s Household Debt and Credit Report for the first quarter.

Mortgage balances, delinquencies, and foreclosures.

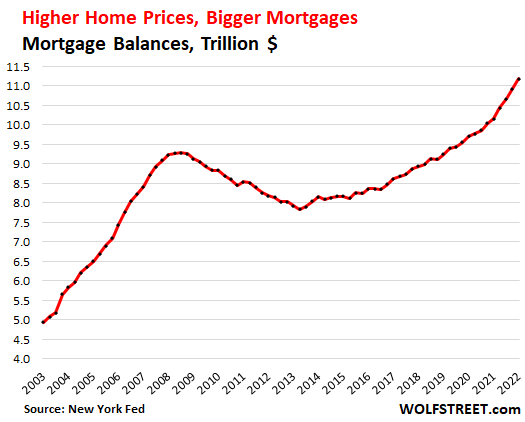

Mortgage balances jumped, as people bought fewer homes but with larger mortgages to fund the spike in home prices of 15% year-over-year according to the National Association of Realtors and of 20% according to the Case-Shiller Home Price Index.

Total mortgage balances jumped by 10% year-over-year in Q1, to $11.2 trillion, even as home sales declined 3.6%:

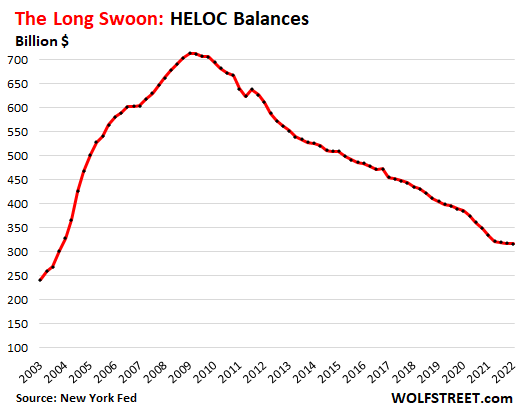

But HELOCs continued to fall out of favor. Since the Financial Crisis, the balance of Home Equity Lines of Credit has declined – replaced by cash-out refi – and in Q1 edged down to $317 billion, the lowest since October 2003:

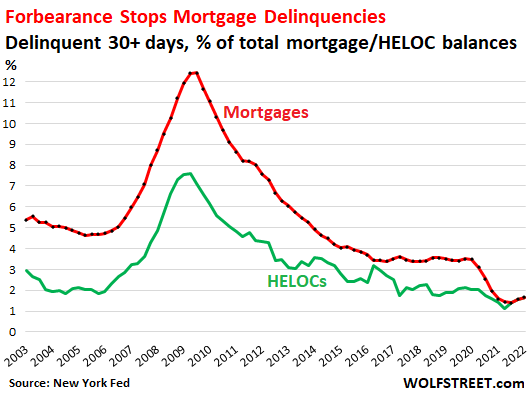

Forbearance cured delinquencies, but now it’s over. Delinquent mortgages that were entered into a forbearance program were reclassified to “current,” though the homeowners stopped making mortgage payments. Then the process started to get homeowners out of these forbearance programs.

The surge in home prices over the past two years had the effect that homeowners could exit forbearance by selling the home, pay off the mortgage, and walk away with cash. This was one way of exiting forbearance.

But lenders, amid the surge in home prices and improving job market and rising wages, helped their customers exit forbearance by modifying mortgages or refinancing them.

The number of homeowners still in forbearance dropped to just 525,000 by mid-April, from 4.3 million at the peak in June 2020, according to the Mortgage Bankers Association. So that issue went away with the explosion in home prices.

Now, with forbearance programs largely over, mortgage delinquencies have started to tick up from the record lows last year.

Mortgage balances that were 30 days or more delinquent rose to 1.66% of mortgage balances in Q1. While a change in trend, it’s still near the record low of 1.39% in Q3, 2021 (red line).

HELOC balances that were 30 days or more delinquent rose to 1.65% of HELOC balances in Q1 (green line):

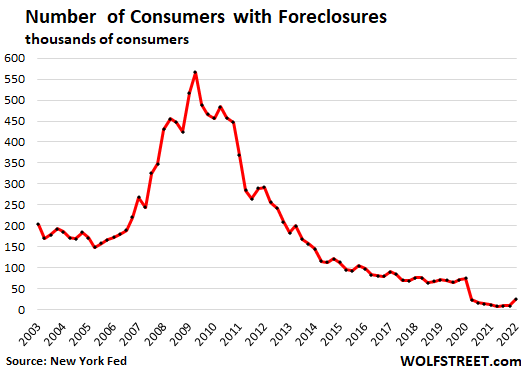

The number of consumers with foreclosures ticked up to 24,240, up from a record low of 8,100 consumers in Q2 last year, and the first real uptick during the pandemic. But it remains near record lows. By comparison, during much of the mortgage crisis, over 400,000 consumers per quarter had foreclosures:

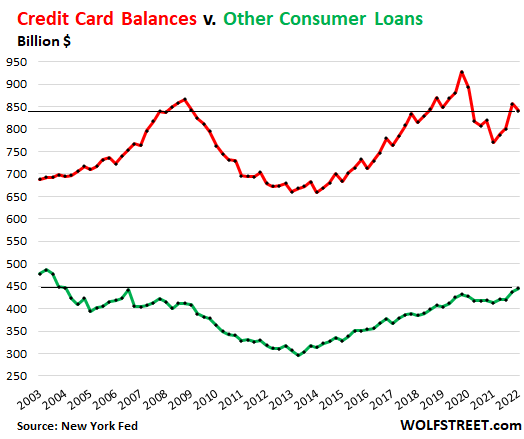

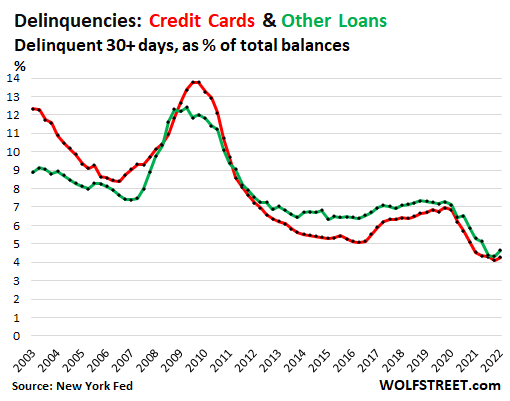

Credit card balances and delinquencies.

Credit card balances, excluding other revolving loans such as personal loans, dipped to $840 billion in Q1, from Q4, right back where they’d been in Q1 2008, and below Q1 2020 and Q1 2019, after 13 years of population growth, inflation, and raging inflation (red line).

This shows that consumers have reduced their reliance on credit cards, which makes sense given the usurious interest rates. But on an individual basis, some borrowers are overextended even during this miraculous stimulus era.

Other consumer loans, such as personal loans, edged up to $450 billion, but was below the highs before the Financial Crisis (green line):

Credit card delinquencies of 30 days or more ticked up a tiny wee bit from the record low in Q4, to 4.27% of total credit card balances, the first uptick during the pandemic (red line).

Delinquencies of other consumer loans, such as personal loans, also ticked up from the record low in Q4, to 4.65% of loan balances (green line):

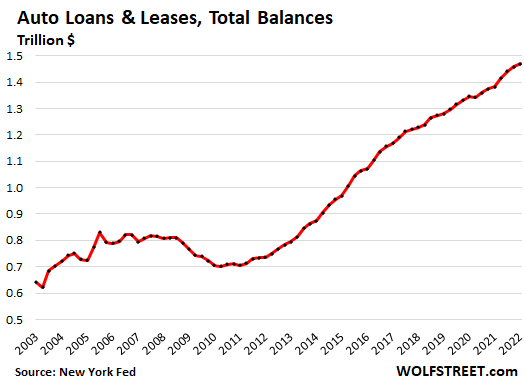

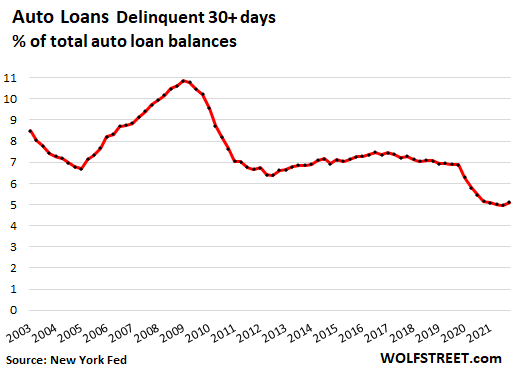

Auto loan balances and delinquencies.

Balances of auto loans rose 6.4% year-over-year to $1.47 trillion in Q1, on much higher vehicle prices and lower volume:

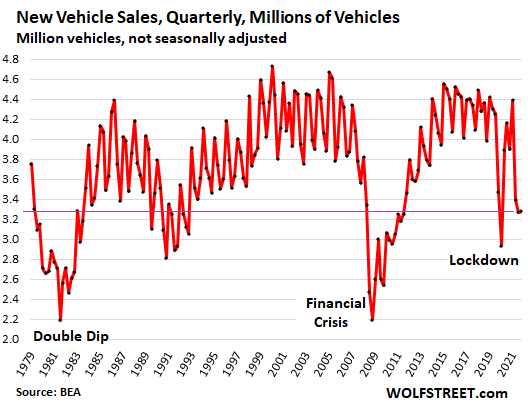

That auto loans rose at all shows just how much more the shrinking number of customers paid for their vehicles because:

- The number of used vehicles sold retail by dealers fell in Q1 fell, including by 15% year-over-year in March.

- The number of new vehicles sold in Q1 fell by 16% year-over-year, to 3.28 million vehicles, right back where they’d been in 1979, due to empty dealer lots.

Auto loan delinquencies of 30+ days ticked up to 5.1% of total auto loan balances in Q1, from the record low in Q4 2021. All that free money, and not having to make rent and mortgage payments helped a lot of folks catch up with their car payments. But now with those programs ended, we can see the first little bitty increase in delinquencies:

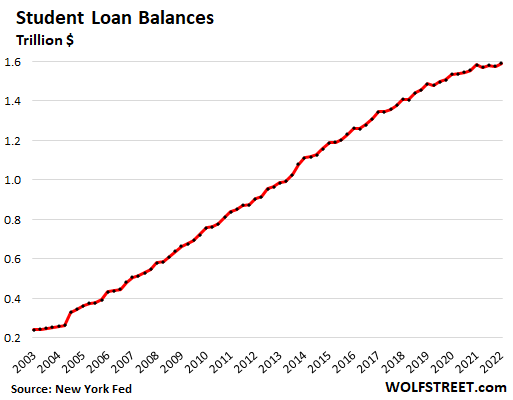

Student loans balances, forborne, and to be forgiven.

I’m at the moment not even sure how to write about student loans anymore. Are they still loans, when everyone expects at least some of them to be forgiven, and some expect all of them to be forgiven? A bunch of loans are already being forgiven even as I write this, and then they’re written off and disappear. It’s a taxpayer asset that just disappears.

Student loans are split into two groups, according to a separate report by the New York Fed:

- Federal student loans: 37 million borrowers, $1.3 trillion.

- Family Federal Education Loans (FFEL) owned by commercial banks, and private loans, combined 10 million borrowers, with $133 billion and $95 billion in loans respectively.

All federal student loans were automatically enrolled in forbearance in March 2020, and borrowers still don’t have to make payments.

Borrowers with FEEL or private loans were not enrolled in automatic forbearance, but were in shorter voluntary forbearance programs and then had to make payments again.

And new student loans are being added. But few pay-downs are being made, and the balances have been flat for a year because loans are being forgiven in big blocks and are written off, just like that, and taxpayers get to kiss their asset goodbye.

The unbearable burden of student loans? So now let’s destroy the ridiculous notion that these poor kids owe $100,000 or $200,000 each, and must therefore be forgiven their student debt because they’ll never be able to pay it off. Surely, some folks, especially those with long graduate programs, such as dentists and doctors, may owe that much, but they’re also much better able to pay for them.

Here is reality – the median loan balance by type of loan. Median means half owe more and half owe less:

- Federal: $18,773

- FEEL: $10,143

- Private: $14,087

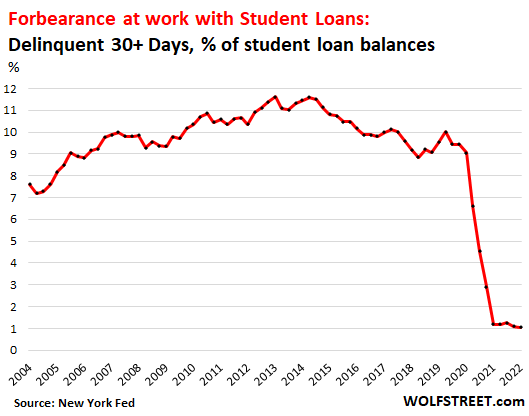

All federal student loans were enrolled in forbearance in March 2020 and delinquent loans were classified as “current,” and the delinquency rate fell to something close to 0%.

The borrowers with delinquent FEEL or private loans are now classified as delinquent.

The delinquency rate here is the combined delinquency rate of all student loans, but nearly all delinquent loans are FEEL or private loans, as the federal loans are still in forbearance. And these forbearance programs caused loan balances that are 30+ days delinquent to plunge from a range of 9% to 11% of the total before the pandemic to about 1% in Q1:

Cleaning up credit scores with stimulus money.

Some of the gazillion dollars handed to consumers and businesses alike, and some of the money consumers didn’t have to pay for rents and mortgage payments, was used to catch up with debts that consumers had fallen behind on. Hence the record low delinquency rates in 2021.

This had the effect that credit scores have been rising, and many borrowers’ credit scores went from subprime to prime, and this played out across the scale, and it improved the “credit quality” across the board of consumer lending.

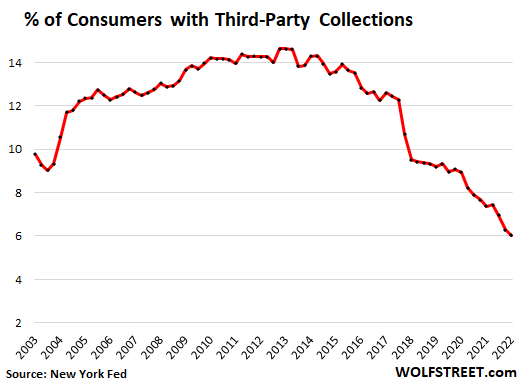

Third-Party Collections.

The percentage of consumers whose loans had been sent to third-party collections plunged throughout the pandemic on a trend that started in 2015, and in Q1 hit a record low of 6.0%. No uptick there yet:

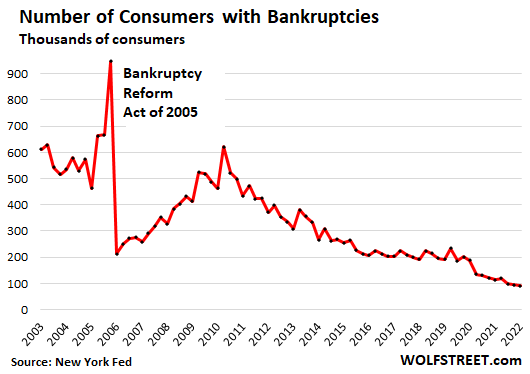

And bankruptcy filings.

The number of consumer bankruptcies in Q1 dropped to a record low of 90,880 consumers. The Bankruptcy Abuse Prevention and Consumer Protection Act of 2005 caused a spike in bankruptcy filings before the deadline. After the new law took effect, bankruptcy filings plunged. The Financial Crisis fueled another surge. Since then, filings have declined:

Higher interest rates are not going to knock over consumers yet.

Consumers might gripe about higher mortgage rates and higher rates for auto loans, and they’re going to buy fewer homes until prices come down far enough. And they might spend a little less on other stuff.

But in terms of their debts, and in terms of delinquencies, foreclosures, and bankruptcies, consumers are “solid” and in “great shape,” as Powell keeps pointing out. Credit scores have improved across the board. Delinquencies are near historic lows. Consumers payed down their credit cards, and they’re off the worry list. And the government is going to perform a miracle with the student loans.

This clean-up of consumer credit is why consumers can handle higher interest rates just fine, and Powell keeps pointing it out. And many consumers – particularly the belittled and denigrated savers – benefit from higher interest rates, and they’ll provide some positive oomph the spending when interest rate repression ends.

Enjoy reading WOLF STREET and want to support it? Using ad blockers – I totally get why – but want to support the site? You can donate. I appreciate it immensely. Click on the beer and iced-tea mug to find out how:

Would you like to be notified via email when WOLF STREET publishes a new article? Sign up here.

![]()

[ad_2]

Source link

U.S. Small Business Optimism Slides to Almost Two-Year Low

The Risk of a US Recession Is Rising. Here’s What That Means for States’ Credit Outlook