Era of Stimulus-Distorted Consumer Credit Ends: Auto Loans, Delinquencies, Prime & Subprime

Auto-loan balances surge on sky-high prices, despite sales plunge. Delinquencies rise to pre-pandemic lows, subprime delinquencies return to 2016-2019 levels.

By Wolf Richter for WOLF STREET.

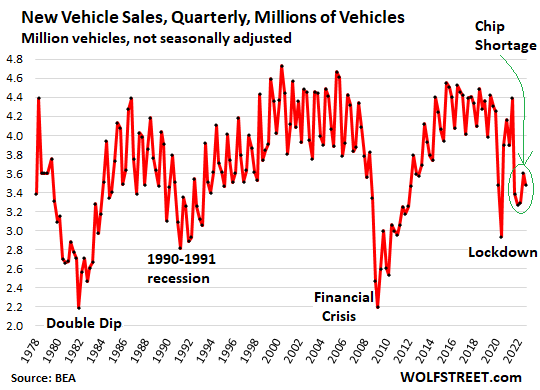

The balance of auto loans and leases continued to surge in Q3 even though new-vehicle sales in Q3 were at levels first seen in the late 1970s – and that’s not a typo – with the number of vehicles sold down by 19% in Q3 compared to Q3 2019; and with used-vehicle unit sales down about 15%.

Auto loan balances surged because new-vehicle prices surged as automakers keep going upscale because that’s where the money is, and because they’re supply constrained and are trying to boost their dollar-revenues and profit margins by prioritizing more expensive models and by price increases even as sales of new vehicles are in terrible shape.

Auto loans also surged because used-vehicle prices had spiked in a ridiculous manner though there were never any shortages of used vehicles. Some of those price spikes have finally started to back off a little.

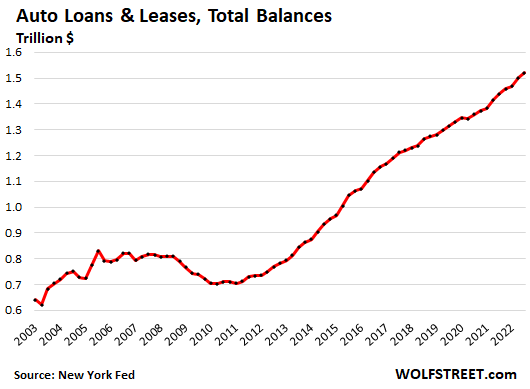

So balances of auto loans and leases increased by 2.2% in Q3 from Q2, and by 6.1% year-over-year, to a record $1.52 trillion, according to data from the New York Fed’s Household Debt and Credit Report, on a mix of surging prices, going upscale because that’s where the money is, and dropping unit sales, leading to fewer but bigger loans with longer terms:

But in terms of the number of units delivered to the ultimate customer, new vehicles sales in Q3 plunged by 19% compared to Q3 2019. But sales had also been declining in the years before the pandemic. Compared to Q3 2016, sales were down by 22%. At 3.48 million vehicles, sales were back where they’d been in the late 1970s.

Price increases and going upscale are driving the industry – even as more and more Americans are priced out of the new vehicle market – and that process has been happening for many years:

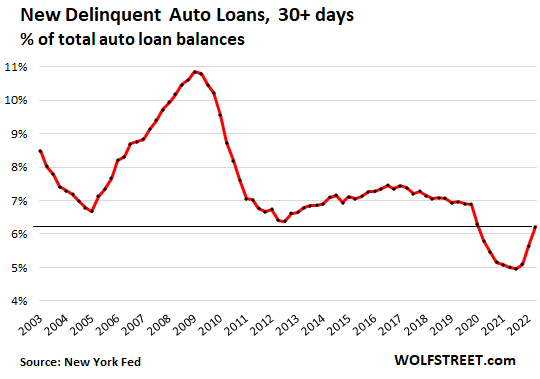

Delinquencies rise to Good Times lows from historic lows.

The rate of all auto loans and leases – prime and subprime – that were 30 days and more past due rose to 6.2% in Q3, according to the New York Fed’s Household Debt and Credit data. This was still below the record lows before the pandemic.

In 2020 and 2021, consumers used their stimulus money and extra unemployment benefits and their PPP loans and the cash left over from not having to make rent or mortgage payments to get caught up on their auto loans. And some borrowers were able to enter their delinquent auto loans into forbearance programs, which turned “delinquent” loans into “current” loans. And the delinquency rate plunged to record historic ridiculous lows, one of the many distortions of the pandemic stimulus economy.

But this era has ended, and delinquency rates are returning to the pre-pandemic Good Times lows, and that’s what we’re seeing here: delinquencies are normalizing at very low levels.

This doesn’t mean it’s going to stay this way: The delinquency rate began rising in late 2005, in lockstep with the Housing Bust, more than two years before the Great Recession, because borrowers under mortgage stress also fell behind on their auto loans. The delinquency rate continued rising into the Financial Crisis and peaked in 2009 at nearly 11%, and then began to decline.

But today, unemployment is at very low levels, the number of unemployment insurance claims is near historic lows, and the economy is far from the type of unemployment crisis it had during the Great Recession. So for now, consumers are still taking good care of their auto loans.

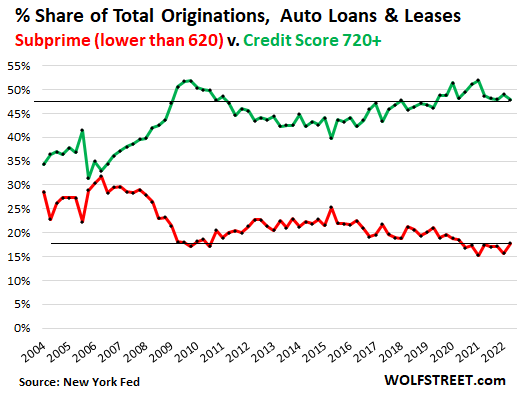

Subprime loans and delinquencies.

The share of subprime auto loans – borrowers with credit scores below 620 – that were originated in Q3 ticked up from record lows to a share of 17.8% of total auto loan originations in the quarter, and remained in the same low range of the past two years. Before the Financial Crisis, the share of subprime auto loans that were originated ranged between 25% and 30%-plus (red line).

By contrast, prime loans with a credit score of 720 and higher that were originated in Q3 had a share of 47.8% of total originations, in the upper portion of the range (green line).

This means that overall credit quality of auto loans that were originated in Q3 – as viewed by credit scores – was relatively high.

Total subprime auto loans outstanding amounted to about $250 billion, according to data from Experian. So the dollar amounts are not huge.

Subprime auto-loan delinquencies dipped to 5.1% of subprime auto-loan balances in October, according to the Fitch Auto Loan 60+ Days Delinquency Index that tracks subprime loans that have been rolled into Asset Backed Securities (ABS) and sold to investors.

The October delinquency rate of 5.1% was down from the October 2019 rate of 5.4%. The index has been in this range since 2016, after more aggressive subprime lending and securitizations became all the rage starting in around 2014.

Securitizations of subprime auto loans spread the risk and make them immensely profitable due to the high interest rates, the relatively easy recovery of the collateral, and the liquidity of the used-vehicle wholesale market where these repossessed units are sold. Most subprime loans finance the purchase of used vehicles that are several years old, and losses for lenders when they repossess the vehicle and sell it at auction are generally not huge.

In terms of the lenders: most of them securitize their subprime auto loans and sell them to investors, so if there is a hiccup, investors carry a big part of the risk. Lenders have some skin in the game by having to retain a small equity portion of the ABS that takes the first losses.

Some smaller specialized subprime lenders collapse periodically because they got tripped up in some way. Some of them did that before the pandemic. And there will be more of them, but that’s how it goes. During an employment crisis of the 2009 variety – if we get another one like that – most of the losses will be borne by investors such as bond funds, pension funds, life insurers, etc.

But the amounts are just not huge: the total amount of subprime auto loans outstanding is only about $250 billion, and this is spread all around mostly in the fixed-income portfolios of investors

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the beer and iced-tea mug to find out how:

Would you like to be notified via email when WOLF STREET publishes a new article? Sign up here.

![]()

[ad_2]

Source link

China Stockpiles Record Cash In Sign of Slow Fiscal Stimulus

Gold jumps as rising Ukraine tensions spur safe-haven demand