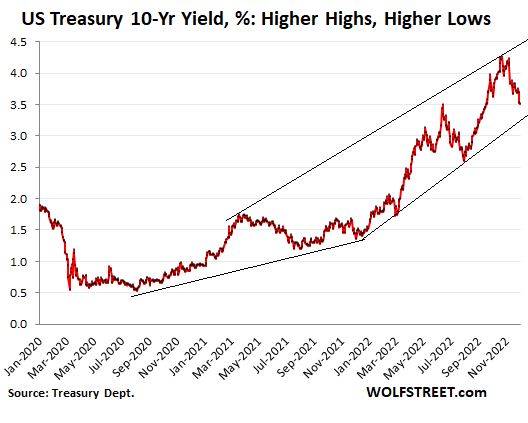

Drop in 10-Year Treasury Yield & Mortgage Rates Is Just Another Bear-Market Rally. Longer Uptrend in Yields Is Intact, with Higher Highs and Higher Lows

“Nothing goes to heck in a straight line.” That’s how functional markets adjust to a new reality: Higher inflation, higher rates.

By Wolf Richter for WOLF STREET.

There has been a lot of discussion and handwringing and Fed-pivot fantasizing about the drop of the 10-year Treasury yield from 4.25% at the end of October to 3.51% at the close on Friday. That’s a 74-basis-point drop. In percentage terms, the yield dropped by 17%. A drop in yield means a rise in prices of these securities. So this drop in yields represents a rally in prices.

But here is the thing: During the summer bear-market rally, the 10-year yield dropped by 25%, from 3.49% to 2.60%. Before then, there were a few smaller bear-market rallies. But the biggest bear-market rally during this bond bear market was from April 2021 to August 2021, when the yield dropped by 30%, from 1.70% to 1.19%.

The 10-year yield closed at 0.52% on August 4, 2020, which marked the end of the 39-year bond bull market. Since then, the 10-year yield has risen sharply, with big surges followed by smaller retracements, followed by big surges, followed by smaller retracements, etc., adhering to the Wolf Street dictum that “Nothing Goes to Heck in a Straight Line.” The 10-year yield, as it went up, marked higher highs and higher lows each time. And the current bear-market rally fits in nicely, and the yield could drop further, and it would still fit in nicely:

Back in August 2020, the 10-year yield hit the low of 0.52% – after months of widespread propaganda by bond- and hedge-fund kings, queens, and gurus in the social media, on CNBC, and Bloomberg that the Fed would push interest rates into the negative, just like central banks had done in Europe and Japan.

This was an effort to manipulate people into buying a 10-year security with nearly no yield, thereby driving yields down further, and prices up further, to make said kings, queens, and gurus a lot of money.

Whoever ended up buying 10-year maturities at the time got a really bad deal because that marked the bottom of the 39-year bond bull market, during which the 10-year yield had descended from 15.8% in September 1981 to 0.52% in August 2020 – and not in a straight line – on declining inflation and declining interest rates, with some big wobbles in between, and since 2008, fueled by money-printing and interest rate repression.

But now we have the fastest Fed rate hikes in 40 years, and the Fed’s fastest QT ever, having unwound $381 billion in six months.

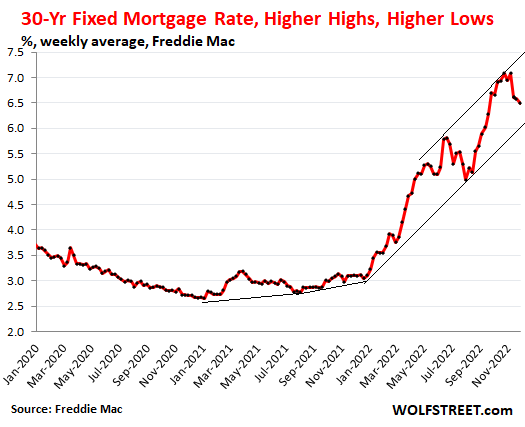

Mortgage rates followed a similar pattern. The 30-year fixed mortgage rate began the rise in early 2021, from a low of 2.65%. But also not in a straight line. By April 2021, it had reached 3.18%, and then it retraced to 2.78% by June 2021. By the end of December 2021, it was back at 3.11%.

And then as the Fed ended QE, and then raised rates, and then embarked on QT, mortgage rates surged – interrupted by big bear-market rallies, most notably the summer bear-market rally when the average 30-year fixed mortgage rate dropped by 14%, from 5.8% to 4.99%, only to surge again to 7.08% at the end of October. As of Freddie Mac’s index released on December 1, the rate has retraced some of that surge, dropping to 6.49%. This represents an 8.3% drop in the average mortgage rates.

Since early 2021, we still have an unbroken uptrend of the 30-year fixed mortgage rate, marked by higher highs and higher lows, and a further drop would still fit in nicely into the overall uptrend:

The trend is your friend. There has been a huge amount of Fed-pivot mongering and rate-cut mongering and the-Fed-will-restart-QE-soon mongering, etc. All this is part of the normal game of how markets are adjusting to new realities, with each side pushing in its own direction, thereby pushing markets up and down in a volatile manner. But this is how functional markets adjust to new realities. Adjustments don’t happen all at once. And if they do, it’s a truly spooky affair. And they don’t adjust in predictable straight lines either. They go about it over time in their rough and tumble way, but ultimately, they get there.

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the beer and iced-tea mug to find out how:

Would you like to be notified via email when WOLF STREET publishes a new article? Sign up here.

![]()

[ad_2]

Source link

Unearthed: The impact of geopolitics on gold ft. Tina Fordham, Fordham Global Foresight | Post by Unearthed Podcast | Gold Focus blog

The Farce and Consequences of the Debt Limit and the Debt