A Respected Analyst Is Calling for $3,000 Gold Next Year. I Believe It Could Hit $4,000

Will 2023 be the year that gold hits $3,000 an ounce?

Ole Hansen, respected commodity strategist at Denmark’s Saxo Bank, says it’s possible once markets realize that global inflation will remain hot despite monetary tightening. I believe, as I’ve said before, that gold could climb as high as $4,000.

Hansen notes three other factors that could help push the metal to new record highs next year. One, an increasing “war economy mentality” could discourage central banks from holding foreign exchange reserves in the name of self-reliance, which would favor gold. Two, governments will continue to drive up deficit spending on ambitious projects such as the energy transition. And three, a potential global recession in 2023 would prompt central banks to open the liquidity spouts.

The analyst has already said that his comments are less of a forecast and more of a thought experiment, but I don’t think investors should brush him aside so easily. I believe it’s very possible that we could see $3,000 gold—or higher—in the next 12 to 18 months, for all the reasons he mentioned.

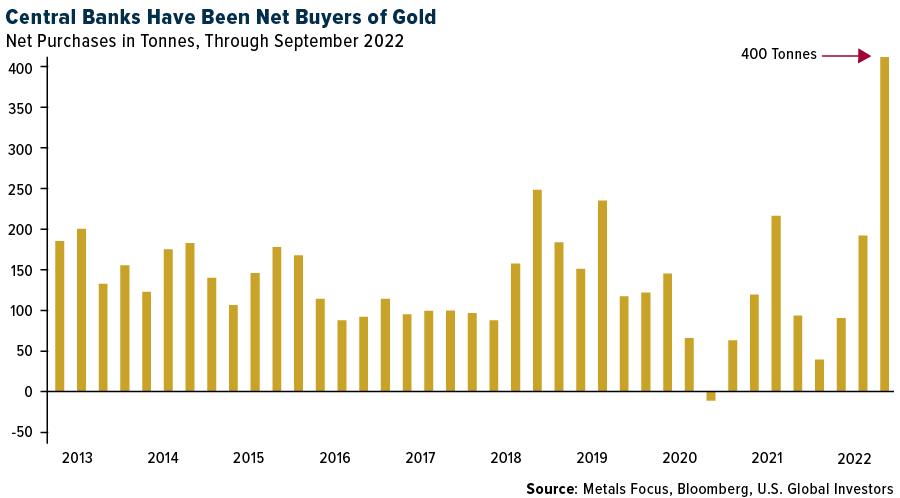

Central Banks on a Gold Buying Spree

Hansen is correct in bringing up central banks’ increasing appetite for gold as a reserve asset. Central bankers and finance ministers may be all about fiat currency, but behind the scenes, they’re gobbling up the yellow metal at the fastest rates in living memory. In the third quarter, official net gold purchases were approximately 400 tonnes, around $20 billion, the most in over a half-century.

Turkey was the biggest gold buyer in the third quarter, followed by Uzbekistan and India.

This week, China’s central bank disclosed it purchased gold for the first time since 2019. The Asian country said it recently added 32 tonnes, or $1.8 billion, bringing its total to 1,980 tonnes.

Despite being the sixth largest holder of gold, not counting the International Monetary Fund (IMF), China still has a long way to go if it wants to diversify away from the U.S. dollar in a meaningful way. The metal represents only 3.2% of its total reserves, according to World Gold Council (WGC) data. Compare that to 65.9% of reserves in the U.S., the world’s largest holder with more than 8,133 tonnes.

This is very bullish, and I predict we’ll be seeing a lot more buying from China in the coming months.

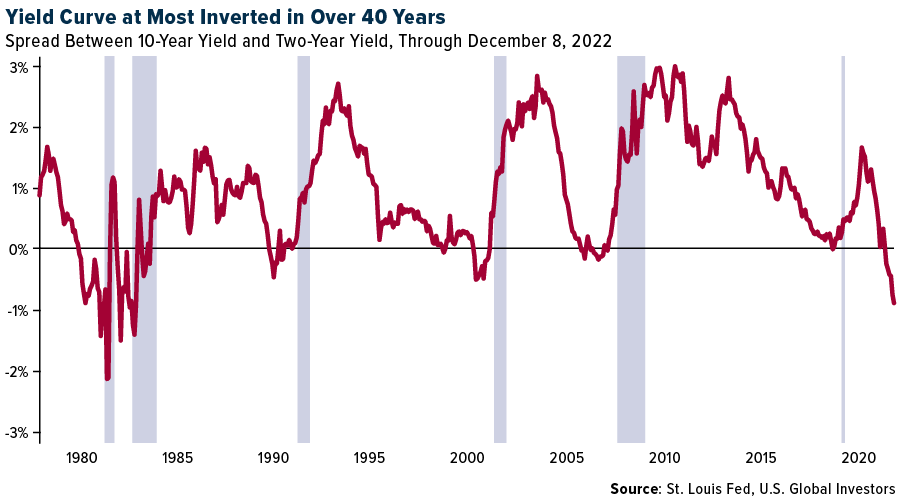

Overtightening Risk and Recession Watch

With inflation looking to persist into next year, a small to moderate recession appears more and more likely. There’s the risk that the Federal Reserve will overtighten, and this has strong macroeconomic implications for gold.

An indicator we keep our eyes on is the spread between the 10-year Treasury yield and two-year Treasury yield. Over the past 40 years (at least), every recession has been preceded by a yield curve inversion. As of today, the yield curve is at its most inverted in over 40 years, suggesting a recession is all but guaranteed. The question is not if, but when.

In recent days, most banks and ratings agencies have slashed their global growth estimates for 2023 on expectations of persistently high consumer prices and rapid monetary tightening. Buying gold now could prove itself to be a wise investment choice. In five out of the last seven recessions, gold delivered positive returns, according to the WGC, providing some protection to investors.

Gold Setting Up for a Rally?

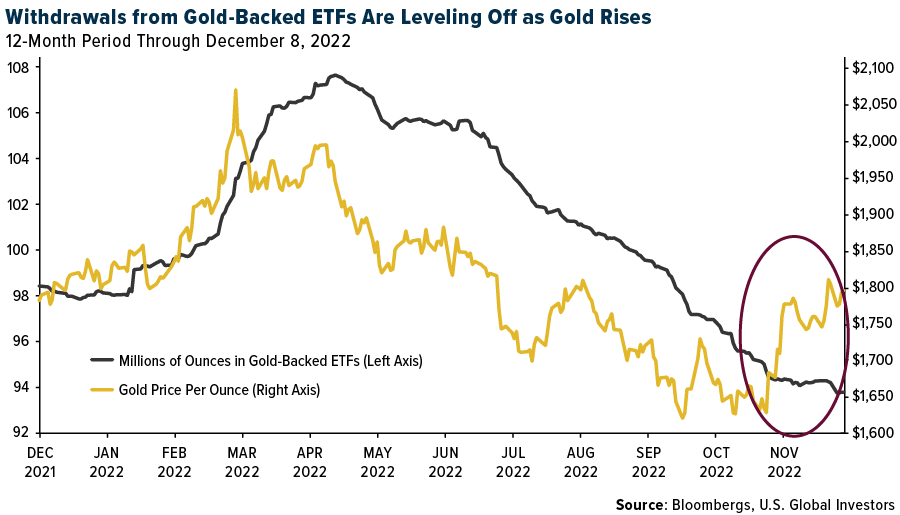

Technically, gold is starting to look attractive right now, the metal having broken above its 50-day and 200-day moving averages. After breaching the key $1,800-an-ounce level last week, gold is again testing the psychologically important price point.

If 2022 ended today, this would mark the second straight year that gold has declined. And yet, at negative 1.75%, the yellow metal has remained one of the best assets to hold this year.

It hasn’t always been easy. Holdings in all known gold-backed gold ETFs have declined for seven months straight as of November 2022. However, we’re starting to see these declines level off as gold begins to push higher.

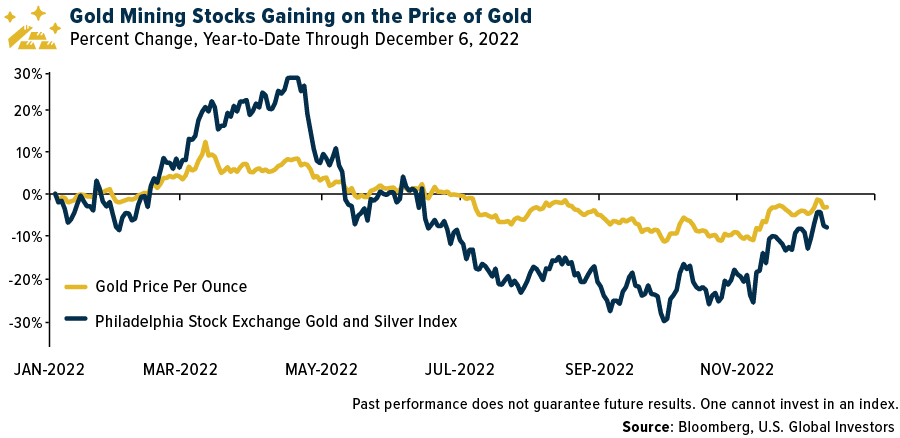

A gold rally—possibly to $3,000, as Ole Hansen forecasts—would also be highly constructive for gold mining stocks. These companies are much more volatile than the price of the underlying metal. As you can see below, when gold has jumped, gold mining stocks have historically jumped higher. (The reverse has also been true.)

Could Gold Be Poised for a Comeback in 2023?

I’ll be co-hosting a webcast this coming Monday, December 12, at 2:00pm Eastern. We’ll be covering the gold market and sharing our outlook for the metal in 2023. If you’d like to join us, please email me at [email protected] with the subject line “Gold Webcast.”

Index Summary

- The major market indices finished down this week. The Dow Jones Industrial Average lost 2.77%. The S&P 500 Stock Index fell 3.37%, while the Nasdaq Composite fell 3.99%. The Russell 2000 small capitalization index lost 5.06% this week.

- The Hang Seng Composite rose 7.14% this week; while Taiwan was down 1.77% and the KOSPI fell 1.86%.

- The 10-year Treasury bond yield rose 10 basis points to 3.593%.

Airlines and Shipping

Strengths

- The best performing airline stock for the week was China Eastern, up 20.2%. IATA data shows that the global air travel recovery continued in October, with solid international traffic up 102.2% year-over-year with softer domestic trends due to China restrictions. Relative to 2019 levels, international traffic improved to -27.9% in October versus -30.1% in September. IATA noted that forward bookings continue to paint a positive outlook despite macroeconomic headwinds.

- Comments from Asian liners including COSCO, Yang Ming and some Asian intra-region players provide some optimism, as all of them do not expect normalized freight rates to go below operating break-even levels, even if near-term the rates overshoot on the downside, (with such a view echoed by Mitsui O.S.K.). Two key highlights: 1) busier-than-expected intra-Asia peak season suggests activity is stabilizing; 2) oversupply concerns in 2023/2024 are likely to be partly mitigated by delivery slippages and “overdue” scrapping as IMO 2023 regulations are expected to have phased-in capacity reduction effects.

- European airline bookings as a proportion of 2019 levels improved significantly by 18 points to -2% in the week, mainly driven by higher international volumes as well as a lower base. Total net sales were up 14% this week. Intra-Europe net sales improved by 12 points to -15% versus 2019 and were up 4% this week.

Weaknesses

- The worst performing airline stock for the week was Allegiant, down 11.7%. Delta Air Lines and its pilots’ union leadership reached an AIP. It includes an at least 18% wage increase or at least a 34% raise over four years. Fleet banding simplification results in wages for select aircraft types increasing the base 18%. The increase compares to 21% in ALK’s ratified contract, albeit the new Delta wages are 11% higher. The AIP includes a “me too” clause that ensures Delta pilot pay exceeds United/American Airlines rates by at least 1%.

- Shipping rates decreased 6.2% week-over-week (WoW) and 59.5% year-over-year (YoY) on North American routes to the west coast, and 7.0% WoW and 36.3% YoY to the east coast. Rates on European routes were down to northern European locations, and down to those around the Mediterranean.

- Airbus said it wouldn’t make its 2022 target of 700 aircraft deliveries but that it maintained its 2022 EBITA and free cash flow guidance. The company also said it was adjusting the speed of its planned production ramp up in the next two to three years.

Opportunities

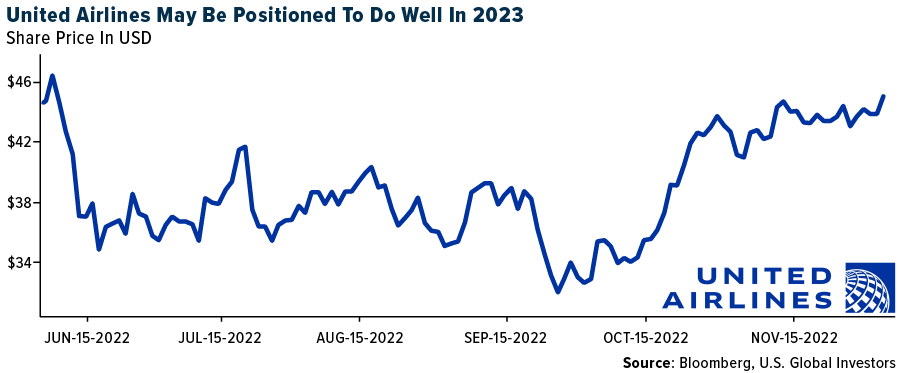

- According to Cowen, United Airlines has the greatest exposure to the ongoing recovery in higher-margin international travel among U.S. airlines. The carrier has more lie-flat seats than all other U.S. airlines combined and its hubs position it well to capture spending by high-net-worth consumers. United is tackling structural challenges through its United Next plan that should improve both unit revenues and unit costs, increase customer loyalty, and lessen exposure to lower-yielding revenue.

- U.S. airlines’ trailing seven-day website visits are up 10% year-over-year for the week. All of the U.S. airlines saw visitation improve this week versus last week on a year-over-year basis except Hawaiian, which saw website traffic decelerate to -18% year-over-year. Out of the “big four,” Southwest Airlines has the highest visitation on an absolute basis and American is the only one that has visitation down on a year-over-year basis.

- Morgan Stanley remains bullish on the air travel outlook for the third year in a row but its order of preference changes slightly. Legacies move to the top of the group’s preference list – Delta is the new top pick. 2023 could be a “Goldilocks” year for the U.S. airlines when market conditions are “just right.” The last three years have seen extreme conditions – 2020 and 2021 were “too cold” due to the lingering pandemic and 2022 was “too hot” with pent up demand and inflation. Similarly, while leisure demand and pricing are arguably “too hot”, corporate/international are still running cold.

Threats

- China’s domestic air traffic still bounced along the bottom at 25% of 2019 levels in the second half of November, down from 28% in the first half of November. Unsurprisingly, domestic traffic at both Beijing and Guangzhou was most disrupted at 5-10% of 2019 levels in the second half of last month, while Shanghai and Hainan performed largely in line with the industry at 30-35% of 2019 levels.

- Goldman expects container shipping to enter a downcycle with oversupply due to softened demand from the U.S. and Europe, relieved port congestion and new ship delivery. As a result, the bank forecasts fuel-adjusted shipping rates to peak in 2022 and decline by 46%/26%/21%in 2022-2025. While shipping rates have started to correct, Goldman sees further downside to rates as the market is yet to recognize the high-capacity addition with 6%/4% in 2023/24E.

- In China, the “10 New Covid Measures” only focus on domestic Covid policy loosening; a key question could be whether there will be any changes to the quarantine requirement for inbound passengers in the near term, as the quarantine requirements for close contacts of Covid cases and inbound passengers used to be similar before the changes.

Emerging Markets

Strengths

- The best performing country in emerging Europe for the week was Romania, gaining 2.8%. The best performing country in Asia this week was Hong Kong, gaining 7.2%.

- The Czech koruna was the best performing currency in emerging Europe this week, gaining 0.3%. The Chinese yuan was the best performing currency in Asia this week, gaining 1.4%.

- Hong Kong equites continue to outperform as the government is considering easing many of its Covid restrictions including those covering overseas entries and quarantine rules. After a sharp spike in Covid cases, authorities in Hong Kong reported a four-fold increase in the number of Hong Kong residents who have taken the fourth Covid vaccination shot in the past week (with the most taking the BioNTech shot designed to protect against omicron variant), FactSet reported.

Weaknesses

- The worst performing country in emerging Europe for the week was Hungary, losing 3.5%. The worst performing country in Asia this week was Indonesia, losing 4.3%.

- The Hungarian forint was the worst performing currency in emerging Europe this week, losing 2.0%. The Indian rupee was the worst performing currency in Asia this week, losing 1.4%.

- China recorded smaller profits from trade. In the month of November, the trade balance surplus declined to $69.84 billion from $85.15 billion in October. Exports declined 8.7% year-over-year and imports dropped by 7.1%.

Opportunities

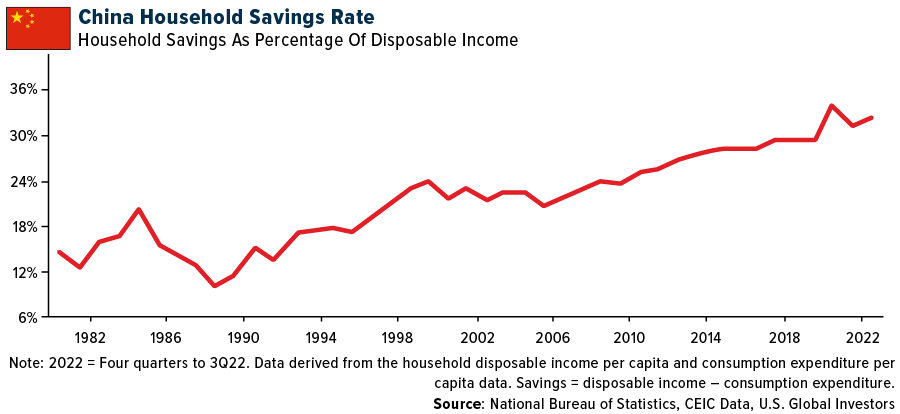

- Christopher Wood in his Greed & Fear publication from December 1, titled “Closet Easing and Face” stated that China’s household savings rate has risen 29.9% in 2019 to 32.3% in the fourth quarter of 2022. High cash-on-hand may lead to strong consumption, just as has been seen in many other markets when lockdowns were ended, and borders were re-opened.

- The final inflation reading for the Eurozone, which will come out next week, may confirm a small correction in the consumer price index (CPI). The preliminary CPI was reported at 10%, below the expected 10.4%, and October’s CPI of 10.6%. The Central Bank of Europe would like inflation to gradually fall back to 2%.

- For now, it seems that Russia will keep exporting oil despite G-7 countries agreeing to set a price cap on Russian oil exports at $60 dollars per barrel. Some members wanted the oil cap price to be much lower (at $30-$40 level) in order not to fund Putin’s war in Europe, but it was set at $60, and at a big discount to international benchmark, which slid to $80 this week. The oil cap at $60 is high enough for Moscow to keep selling oil as Russia is selling oil at a discount, at around $45 per barrel (and way below the cap imposed by G-7 members at $60).

Threats

- China’s recent steps to reopen its economy were well taken by investors, with equites moving higher after years of strict zero-Covid policy depressed the economy and consumer sentiment. While the reopening should lead to normalization of economic conditions, many predict that once the Covid restrictions are relaxed, the medical system may overheat and as many as 2 million people could die in China.

- This week, Russia claimed that Ukraine attacked Russia’s airbases deep inside the country, killing three military personnel. The blasts at sites hundreds of miles from the border between the two countries were the result of a Ukrainian drone attack, Russia’s defense ministry said. Ukraine did not take responsibility for the attack. If the acquisition by Russia is accurate that Ukraine was behind the attacks on Russia territory, this is a serious escalation of the conflict.

- Division among Eurozone members regarding support for Ukraine is growing. Hungary has blocked an €18bn package of EU financial support for Ukraine, which needs close to $40 billion from partners next year to maintain public services.

Energy and Natural Resources

Strengths

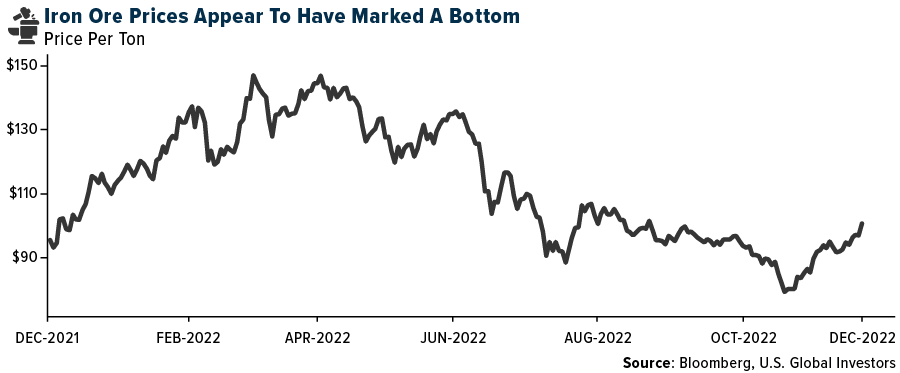

- The best performing commodity for the week was zinc, rising 5.96%, partly on the China reopening trade. However, Nyrstar announced that its zinc smelter in France will remain closed indefinitely. It had been shut since October for maintenance. Iron ore prices continued to rise this week as constructive Chinese policy decisions boosted sentiment and steel prices, while met coal prices have stabilized. The most recent bout of Chinese policies was the central bank cutting the reserve requirement ratio by 25 basis points for banks and the reiteration of easing Covid restrictions.

- Qatar Energy and ConocoPhillips signed 15-year LNG agreements with Germany for the supply of up to 2 million tons per year from Qatar’s ongoing North Field East and North Field South expansion projects, where ConocoPhillips is a key partner. The announcement marks the first-ever sizeable LNG supply deal between Qatar and Germany.

- China boosted energy purchases last month as winter approached, while copper imports continued to defy a slowing economy by reaching their highest level this year. Commodities imports broadly are still lagging the pace set in 2021 as strict virus curbs and the crisis in the property market cast a cloud over consumption.

Weaknesses

- The worst performing commodity for the week was WTI crude oil, falling 10.65%, on anticipation of weaker demand going forward. President Xi Jinping, while visiting Riyadh, expressed closer ties to the region for future energy purchases, the sharing of nuclear technology, big data, and aerospace. In addition, the Chinese currency will be used for all oil and gas trade settlements. U.S. natural gas consumption was down 5% year-over-year this past week on the back of lower residential and commercial demand, power burn, and industrial demand. Total demand was down 11.1 Bcf per day week-over-week.

- In addition to oil weakness, Powder River Basis steam coal fell more than 7% and the Sprott Physical Uranium Trust pulled back about 3%. Natural gas rose less than 1% for the week.

- Mosaic Co. has curtailed potash production at its mine in Saskatchewan as weaker demand sent fertilizer prices on a downturn. Fertilizer prices spiked with the Russian invasion of Ukraine but have since slumped with buyers on strike. However, the U.S. is still importing fertilizer from Russia and that has taken some of the pressure off prices recently as imports have surged.

Opportunities

- According to JPMorgan, the super-cycle is in the early innings, with upside risk to $150 per barrel in 2023-2024 led by tighter spare capacity and potential supply outages; LT $80 per barrel is well underpinned. The group sees limited risk premium in current pricing owing to; 1) the ‘all-in’ breakeven for the global oil producers (including variable shareholder distributions, de-leveraging and now windfall levies) sits at $75 per barrel; this represents the marginal oil price needed to drive incremental investment in supply growth and supports LT $80 per barrel outlook; 2) low OECD inventories; and 3) limited OPEC spare capacity.

- Mass Timber, a new trend in more cost-efficient construction and sustainability, grew despite the recent period of record lumber pricing – (investors are very bullish on the prospects for mass timber with North America seeing a similar adoption/demand curve to that experienced in Europe). Building codes changing are accommodating the trend for mass timber, with 12-story buildings allowed in Canada and 18-story buildings in the U.S.

- According to JPMorgan, commodities are on pace to deliver a second consecutive year of double-digit returns. As global growth slows in 2023 but commodity supply remains constrained and critically low inventories persist, commodity prices may stay elevated despite a decline in economic activity. As in 2022, JPMorgan is most constructive on energy, but unlike 2021, returns will be driven by oil—especially if oil raises roll yields and generates a rebound in investor positioning—whereas U.S. natural gas prices are forecasted to decline 40% by year-end 2023.

Threats

- CIBC revised its commodity price assumptions with notable updates including lowering its 2023E copper price to $3.50 per pound from $3.95/lb., which is below consensus of roughly $3.70/lb. Included in its forecast is $3.35/lb. on average in H1/23E, improving to $3.65/lb. In the second half of next year, as the group expects rising inflation and rates, as well as increased recession risk to be ongoing factors in early 2023, and that rate hike easing, a stabilizing economy can provide support for industrial metals in late 2023 and into 2024. CIBC continues to forecast a copper supply surplus in 2023/2024 and expects that in the medium-term (2025/2026) supply demand fundamentals revert to a market deficit and are supportive of higher copper prices.

- Colombian President Gustavo Petro proposed over the weekend a reform to Colombia’s mining code, which was initially issued in 2001. “It must be reformed; it is of no use to us (…) The State should no longer prioritize big mining multinational companies. The State must prioritize the small, traditional miner, small-scale traditional mining and, above all, support the mining effort that is undoubtedly needed, because this is not a war against mining but against the ways in which mining is currently carried out in Colombia,” he said.

- According to Bloomberg, the U.S. and the EU are considering new tariffs aimed at Chinese steel and aluminum imports to reduce global overcapacity and to help their climate agenda. The idea is reported to be still in its infancy stages and has not been formally proposed. At this time, it is unclear what legal provisions the Biden administration might use to implement new tariffs and whether such a proposal would be WTO compliant.

Luxury Goods

Strengths

- Toll Brothers reported better-than-expected fourth quarter results, supported by strong pricing for the luxury home builder. Lennar shares gained this week as well on expectations that the company may also report good quarterly results next week despite rising mortgage rates.

- China continues to ease Covid restrictions. Beijing eased rules related to mass testing and lockdowns and scrapped mandatory hospitalization and mass quarantines. Local media reported that residents will be no longer be required to show a negative PCR test to enter supermarkets, shopping centers, airports, and other public centers.

- MGM China Holdings, a Macau casino and hotel operator, was the best performing S&P Global Luxury stock for the week, gaining 41.1%. Macau stocks surged after China and Hong Kong started to remove Covid-related restrictions.

Weaknesses

- Tesla’s shares continue to decline. Weak demand for Tesla vehicles in China pushed the company to cut production shifts at its Shanghai factory and delay the on-boarding of some new hires.

- Retail sales in the Eurozone declined 2.7% year-over-year in November from -0.6% in the prior month and below the expected decline of 2.6%. Month-over-month sales weakened as well. Europe is an important area for the luxury sector, generating about 27% of revenue in 2021.

- Farfetch, an online retailer selling luxury products worldwide, was the worst performing S&P Global Luxury stock for the week, losing 24.9%. Shares continue to sell off this week after last week’s drop of 35% in a single day on December 1, after the company provided a disappointing outlook.

Opportunities

- According to Altiant’s survey of 1,200 high-net-worth individuals and travelers in 14 countries spanning parts of Asia, Europe, and the Americas during the second half of 2022, tourists are eyeing more international trips next year. The report also found that a majority of the wealthy travelers continue to prefer spending on experiences over tangible goods. Almost 60% plan to spend more on travel in 2023, compared with 10% who say they would cut back. Wellness will remain a key diver in vacation planning for 61% of respondents.

- Marriott International announced plans at the International Luxury Travel Market (ILTM) Cannes to introduce more than 35 luxury hotels in 2023. The company has nearly 500 luxury hotels and resorts in 68 countries and territories today and is poised to further its position as the global leader in luxury hospitality with more than 200 luxury properties in the development pipeline.

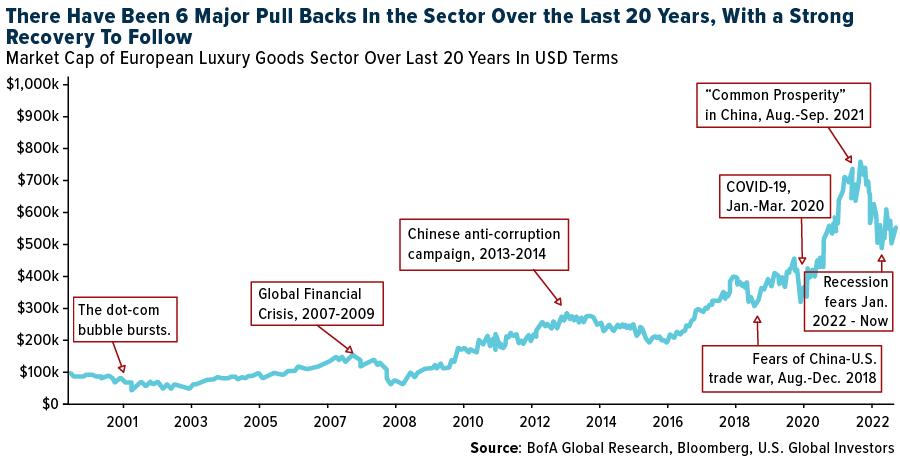

- Bank of America’s Global Research Team believes that the luxury sector presents an attractive buying opportunity. In the chart below, the group shows six prior-major pullbacks in the luxury sector over the past 20 years. The most current pullback has already resulted in a 24% share price decline for the sector since the beginning of the year and more than 35% since the November peak. Strong pullbacks usually lead to a bounce.

Threats

- In November, Apple temporarily shut down its manufacturing plant in Zhengzhou, China potentially leading to a shortage of 6 million iPhone 14 Pro and Pro Max units. The company is planning to expand production into India and Vietnam, but it will take time and money to diversify supply chains. Bloomberg reported that 35% of factories supplying Apple are currently located in China. Ives and Wedbush estimated it would take until 2025 or 2026 for 50% of Apple’s iPhone production to move to India and Vietnam if Apple moved “aggressively.”

- Higher goods and services prices this holiday season compared to last year may put a dent in shoppers’ spending habits. This year, more shoppers may be willing to look for deals rather than blindly buying expensive gifts for friends and family members. The National Retail Federation predicts that holiday sales in November and December will increase 6% to 8% from last year. The annual rate of inflation in October was 7.7%.

- Credit card spending is softening among shoppers who have higher incomes, according to Barclay’s research team. After many years where consumer spending growth on luxury goods has been stronger than spending on basics or discount items, the group now sees spending by luxury consumers clearly lagging.

Blockchain and Digital Currencies

Strengths

- Of the cryptocurrencies tracked by CoinMarketCap, the best performer for the week was Axie Infinity, rising 16.39%.

- Goldman Sachs Group plans to invest tens of millions of dollars in crypto firms, citing an interview with Mathew McDermott, global head of digital assets at the company. The bank plans to buy or invest in crypto firms after the collapse of FTX hurt investors’ interest and valuations, writes Bloomberg.

- Crypto exchange Binance Holdings on Wednesday released its first proof of reserves, based on a snapshot review by accounting. The report shows the exchange having sufficient crypto assets to balance its total platform liabilities, writes Bloomberg. It captures a glimpse of Binance’s Bitcoin holdings at a specific moment in time to reassure customers that its assets and liabilities match.

Weaknesses

- Of the cryptocurrencies tracked by CoinMarketCap, the worst performer for the week was 1inch Network, down 11.82%.

- Circle Internet Financial, the issuer of the cryptocurrency USDC stablecoin, said its planned merger with special purpose acquisition company Concord Acquisition Corp. has been terminated. Under the terms of Concord’s amended and restated certificate of incorporation, Concord has until December 10 to consummate a business combination, writes Bloomberg.

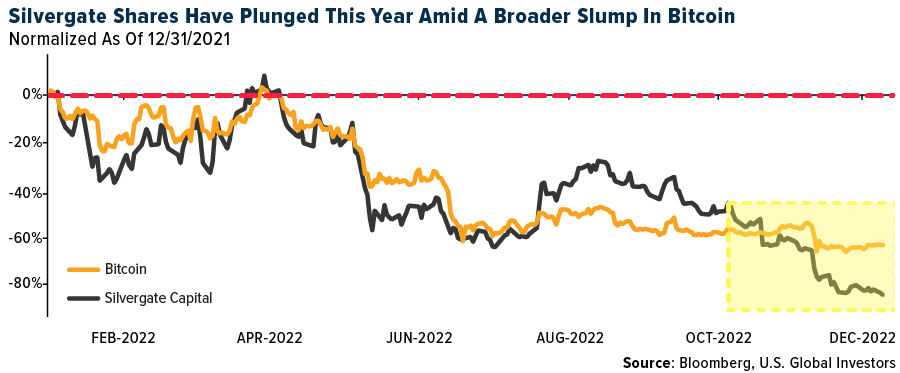

- Crypto bank Silvergate Capital Corp was asked by three U.S. Senators to release all records related to transfer of funds for the collapsed FTX empire of Sam Bankman-Fried. Shares of La Jolla, a California-based bank, fell as much as 8%. The slide extends Silvergate’s losses for the year to more than 84% and has it trading at a fresh 52-week low, writes Bloomberg.

Opportunities

- Coinbase Global Inc. waived fees for converting Tether Holdings stablecoin USDT for the token Coinbase backs, reports Bloomberg, as competition heats up among the three biggest issuers of such digital assets. In a blog post on Friday, Coinbase sought to portray stablecoin USDC as a safer asset amid the turmoil unleashed by the collapse of crypto exchange FTX as month ago.

- The European Union proposed new rules on Thursday to combat tax fraud and evasion in the crypto sector by requiring all digital asset service providers to report transactions involving customers residing in the bloc. The initiative by the EU’s executive arm, part of a package to increase the transparency in the tax system, aims to ensure that the bloc’s residents pay taxes on gains from trading or investing in crypto assets, writes Bloomberg.

- FTX’s new CEO and bankruptcy lawyers met with Manhattan federal prosecutors investigating the cryptocurrency exchange’s collapse and allegations that it misused billions of dollars in customer funds. John J. Ray met this week with the U.S. attorney’s office for the Southern District of New York, writes Bloomberg.

Threats

- Digital assets are already a year into one of the industry’s worst slumps, but judging from recent announcements of steep headcount reduction, crypto executives seem to be bracing for more pain. Crypto exchanges Bybit and Swyftx over the past two days said they’re laying off 30% and 35% of their staff, respectively. The announcements came less than a week after bigger rival Kraken unveiled a similar workforce scrapping, writes Bloomberg.

- Orthogonal Trading said in a tweet on Tuesday that it had been “severely impacted by the collapse of FTX and associated trading activities” making it unable to repay on a $10 million crypto loan, reports Bloomberg. That prompted the entity that runs the lending pool on DeFi protocol Maple to issue a notice of default for all the fund’s active borrowings.

- Amber Group, one of Asia’s leading crypto platforms, has continued to lay off staff and put a funding round on hold amid turmoil in the digital-asset sector following the bankruptcy of the FTX exchange. The job cuts at the Singapore-based company, whose backer includes Temasek Holdings and Sequoi China, according to an article published by Bloomberg.

Gold Market

This week gold futures closed at $1.806.90, down $2.70 per ounce, or 0.15%. Gold stocks, as measured by the NYSE Arca Gold Miners Index, ended the week lower by 2.14%. The S&P/TSX Venture Index came in off 3.60%. The U.S. Trade-Weighted Dollar rose 0.38%.

| Date | Event | Survey | Actual– | Prior |

|---|---|---|---|---|

| Dec-5 | Durable Goods Orders | 1.0% | 1.1% | 1.0% |

| Dec-8 | Initial Jobless Claims | 230k | 230k | 226k |

| Dec-9 | PPI Final Demand YoY | 7.2% | 7.4% | 8.1% |

| Dec-13 | Germany CPI YoY | 10.0% | — | 10.0% |

| Dec-13 | Germany ZEW Survey Expectations | -26.4 | — | -36.7 |

| Dec-13 | Germany ZEW Survey Current Situation | -57.0 | — | -64.5 |

| Dec-13 | CPI YoY | 7.3% | — | 7.7% |

| Dec-14 | FOMC Rate Decision (Upper Bound) | 4.50% | — | 4.0% |

| Dec-14 | China Retail Sales YoY | -3.9% | — | -0.5% |

| Dec-15 | ECB Main Refinancing Rate | 2.500% | — | 2.000% |

| Dec-15 | Initial Jobless Claims | 234k | — | 230k |

| Dec-16 | Eurozone CPI Core YoY | 5.0% | — | 5.0% |

Strengths

- The best performing precious metal for the week was palladium, up 3.12%. Anglo American Plc warned this week that production across its operations will be lower than expected over the next couple of years. Platinum group metals were hit especially hard as total output could fall as much as 12.5% by 2025. Earlier in the week, Glencore lowered its forecast for 2023 on most of its commodities.

- Gold steadied after touching the highest level since July as traders weighed more U.S. economic data and China’s relaxation of its strict zero-Covid policies. Bullion had been hurt by the Fed’s aggressive rate hikes this year, but recent indications that the central bank is becoming less hawkish have boosted the metal, pushing it past $1,800 an ounce last week.

- The world’s largest gold exchange traded fund (ETF) is to store some of its inventory outside London for the first time, in a move aimed at facilitating further expansion. The $52.5 billion SPDR Gold Trust (GLD) has held all of its bullion in HSBC’s London vaults since its inception as the first physically backed gold ETF in 2004. However, it is now adding a second custodian, JPMorgan, utilizing the U.S. bank’s vaults in Zurich and New York, as well as in London. It is believed to be the first time a gold ETF has had multiple custodians.

Weaknesses

- The worst performing precious metal for the week was gold, off 0.15%. After last week’s near-2.43% gain in gold, bearish investors tried to send a message of weakness with the Monday open. Investors sold off 0.47% of total known gold ETF holdings, which is a significant quantity relative to normal daily flows. The selloff message didn’t resonate however, with gold climbing in price each subsequent day of the week.

- Gold’s rebound above $1,800 an ounce has been met with selling by some of the largest players in the market, raising questions about the sustainability of the rally. Bullion-backed ETFs cut their holdings by 13.7 tons, according to an initial tally by Bloomberg. The biggest daily drop in 20 months pushed down gold by the most since September.

- The Perth Mint reported sales of gold coins and minted bars back to 114,304 ounces in November from 183,102 ounces in October. Silver coins and bars fell concurrently. The Mint noted, despite the fall back, sales were still at their second highest level this financial year.

Opportunities

- China reported an increase in its gold reserves for the first time in more than three years, reports Bloomberg, shedding some light on the identity of the mystery buyers in the bullion market. The People’s Bank of China raised its holdings by 32 tons in November from the month before, according to data on its website on Wednesday. That brought its total to 1,980 tons, the sixth-biggest central bank bullion hoard in the world, the article continues.

- M&A will continue into 2023, with numerous senior companies having publicly commented on looking at M&A as part of their growth strategy. Transactions that provide diversification and less risk concentration would garner shareholder support. There may be further consolidations in the streaming space (between the smaller players).

- India’s trade ministry is discussing a reduction in import taxes on gold to rein in illegal shipments, according to people familiar with the matter. The world’s second-largest consumer of the precious metal, almost all of which is purchased from abroad, has asked the Finance Ministry to consider reducing the tariff to about 10% from 12.5%, two of the people said, asking not to be identified as the deliberations are private.

Threats

- Gold Field’s key rationale for its Yamana offer was an emerging “gap” of production decline to 2.0 million ounces by 2030, which was reiterated on November 28 as a reason to continue to look at M&A. The gap is not an urgent strategic weakness for Gold Fields; the company may have a production decline to 2.3 million ounces in 2029, but with $8 billion free cash flow 2023-2030E and a debt-free balance sheet to reinvest over the long term, it will be able to find new avenues of production.

- Google searches for “diamonds” in the U.S. appear to have decoupled from their historical trend of sharply rising into the holiday season. This could be indicative of weakening consumer appetite for these stones, as evidenced by the softening for polished prices across the size spectrum as well as the weaker-than-expected DeBeers’ site sales.

- Extortion is how mining executives in South Africa are describing “Mafia” like groups organizing to disrupt mining operations with a threatening letter, a derailed train, blocked roads, burned vehicles, and workers locked up, reports Bloomberg. In November, a train derailed on the main export route for coal miners. Transnet SOC Ltd, said the incident occurred “against a backdrop of threat and disruptions to the company’s operations by disgruntled groupings seeking business combinations.” South Africa is now ranked 75 out of 84 jurisdictions, compared to 40in 2019, by the Frazier Institute’s Annual Survey of Mining Companies.

This commentary should not be considered a solicitation or offering of any investment product. Certain materials in this commentary may contain dated information. The information provided was current at the time of publication. Some links above may be directed to third-party websites. U.S. Global Investors does not endorse all information supplied by these websites and is not responsible for their content. All opinions expressed and data provided are subject to change without notice. Some of these opinions may not be appropriate to every investor.

Holdings may change daily. Holdings are reported as of the most recent quarter-end. The following securities mentioned in the article were held by one or more accounts managed by U.S. Global Investors as of (09/30/22):

ConocoPhilips

Wesdome Gold Mines

Mandalay Resources

Yamana

COSCO Shipping Holdings

Yang Ming Marine Transport

Mitsui OSK

Delta Air Lines

American Airlines

United Airlines

Airbus SE

Southwest Airlines

Hawaiian Holdings

Marriott International

Anglo American Plc

*The above-mentioned indices are not total returns. These returns reflect simple appreciation only and do not reflect dividend reinvestment.

The Dow Jones Industrial Average is a price-weighted average of 30 blue chip stocks that are generally leaders in their industry. The S&P 500 Stock Index is a widely recognized capitalization-weighted index of 500 common stock prices in U.S. companies. The Nasdaq Composite Index is a capitalization-weighted index of all Nasdaq National Market and SmallCap stocks. The Russell 2000 Index® is a U.S. equity index measuring the performance of the 2,000 smallest companies in the Russell 3000®, a widely recognized small-cap index.

The Hang Seng Composite Index is a market capitalization-weighted index that comprises the top 200 companies listed on Stock Exchange of Hong Kong, based on average market cap for the 12 months. The Taiwan Stock Exchange Index is a capitalization-weighted index of all listed common shares traded on the Taiwan Stock Exchange. The Korea Stock Price Index is a capitalization-weighted index of all common shares and preferred shares on the Korean Stock Exchanges.

The Philadelphia Stock Exchange Gold and Silver Index (XAU) is a capitalization-weighted index that includes the leading companies involved in the mining of gold and silver. The U.S. Trade Weighted Dollar Index provides a general indication of the international value of the U.S. dollar. The S&P/TSX Canadian Gold Capped Sector Index is a modified capitalization-weighted index, whose equity weights are capped 25 percent and index constituents are derived from a subset stock pool of S&P/TSX Composite Index stocks. The NYSE Arca Gold Miners Index is a modified market capitalization weighted index comprised of publicly traded companies involved primarily in the mining for gold and silver. The S&P/TSX Venture Composite Index is a broad market indicator for the Canadian venture capital market. The index is market capitalization weighted and, at its inception, included 531 companies. A quarterly revision process is used to remove companies that comprise less than 0.05% of the weight of the index, and add companies whose weight, when included, will be greater than 0.05% of the index.

The S&P 500 Energy Index is a capitalization-weighted index that tracks the companies in the energy sector as a subset of the S&P 500. The S&P 500 Materials Index is a capitalization-weighted index that tracks the companies in the material sector as a subset of the S&P 500. The S&P 500 Financials Index is a capitalization-weighted index. The index was developed with a base level of 10 for the 1941-43 base period. The S&P 500 Industrials Index is a Materials Index is a capitalization-weighted index that tracks the companies in the industrial sector as a subset of the S&P 500. The S&P 500 Consumer Discretionary Index is a capitalization-weighted index that tracks the companies in the consumer discretionary sector as a subset of the S&P 500. The S&P 500 Information Technology Index is a capitalization-weighted index that tracks the companies in the information technology sector as a subset of the S&P 500. The S&P 500 Consumer Staples Index is a Materials Index is a capitalization-weighted index that tracks the companies in the consumer staples sector as a subset of the S&P 500. The S&P 500 Utilities Index is a capitalization-weighted index that tracks the companies in the utilities sector as a subset of the S&P 500. The S&P 500 Healthcare Index is a capitalization-weighted index that tracks the companies in the healthcare sector as a subset of the S&P 500. The S&P 500 Telecom Index is a Materials Index is a capitalization-weighted index that tracks the companies in the telecom sector as a subset of the S&P 500.

The Consumer Price Index (CPI) is one of the most widely recognized price measures for tracking the price of a market basket of goods and services purchased by individuals. The weights of components are based on consumer spending patterns. The Purchasing Manager’s Index is an indicator of the economic health of the manufacturing sector. The PMI index is based on five major indicators: new orders, inventory levels, production, supplier deliveries and the employment environment. Gross domestic product (GDP) is the monetary value of all the finished goods and services produced within a country’s borders in a specific time period, though GDP is usually calculated on an annual basis. It includes all private and public consumption, government outlays, investments and exports less imports that occur within a defined territory.

The S&P Global Luxury Index is comprised of 80 of the largest publicly traded companies engaged in the production or distribution of luxury goods or the provision of luxury services that meet specific investibility requirements.

Free cash flow (FCF) is the cash a company generates after taking into consideration cash outflows that support its operations and maintain its capital assets.

The Philadelphia Stock Exchange Gold and Silver Index is a capitalization-weighted index which includes the leading companies involved in the mining of gold and silver.

[ad_2]

Source link

A Reset that Serves the People