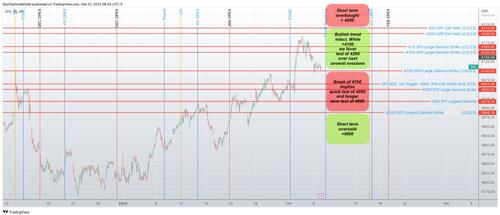

Market Spooked By Large S&P 4,050 Put Buyer, Spike In VVIX

With both BofA’s Michael Hartnett (last week) and Goldman’s biggest FICC bull, Scott Rubner (this morning as pro subs know already, and we will have more on this in a subsequent post) now calling for a mid-February peak in risk assets and predicting a slide in stocks following the CPI report, sentiment appears to be shifting and as our friends and derivative gurus over at SpotGamma discuss this morning, they have “received a large number of inquires into two, linked points”: first, the spike in the VVIX which we first discussed yesterday (this takes place as the VIX lifted back up to around 20 as options traders begin to price in event risk around next week’s CPI print)…

… and second, the Large 25k ES 2/17 4050 put buyer (who according to some unconfirmed twitter reports may be Carl Icahn, although there is zero evidence of this). That said, there has been only a change of 18k OI at that strike for today.

So what’s going on?

First, as Spotgamma explains in regards to the 4050 ES puts, as long as the SPX holds above what has emerged as a key 4100 level (and SpotGamma’s key market support), “these puts will lie fairly dormant with little market impact. Note even though they are short dated, they will likely not significantly decay until Tuesdays AM CPI print.”

However, in line with SpotGamma’s potential “bear triggers” (a break of 4100 and the opening of OPEX weakness) these options are likely to invigorate volatility to the downside, particularly post CPI. This is because under 4100 they add negative gamma that peaks at 4050 into Friday.

The other area that received a lot of attention yesterday was the pop in VVIX, first discussed here. As SpotGamma notes, we have been under a regime of IV compression as discussed here. Realized volatility is not declining as markets have rallied, and are threatening to peak. Despite this, implied volatility has come down sharply, and so the spread between IV/RV has collapsed. From this standpoint one could argue that IV’s path of least resistance is higher.

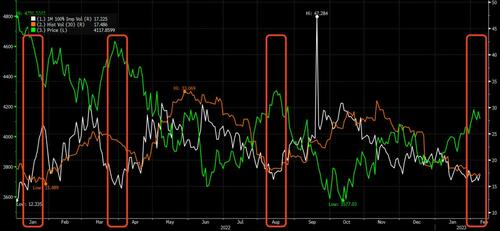

Shown below is the SPX (green) vs 30 day IV (white) vs 30 day RV (orange). As you can see over the past year when IV/RV compress at lows, it has market major highs in the SPX.

The idea at this time was that the recent FOMC may usher in this period of calm, which could allow realized volatility to decline – and subsequently implied volatility. Instead what seems to be happening is the market now “really needs to see this next jobs/CPI/etc” do be convinced things are all clear. As such, RV isn’t dropping, and we are seeing some fairly large hedges hit the market (like the ES trade from above).

In addition, SG has also been seeing several large VIX call trades over the past week, as shown below. This fuels VVIX, which is just VIX skew.

This all circles back to the key ranges SpotGamma has been outlining, and the importance of the risk window opening at 2/13 or on a break of 4100. Incidentally, SG feels that “traders who are betting on downside *today* are fighting a lot of positive gamma in the 4100-4200 area, and resistance releases into OPEX.” On the other hand, as we will show shortly, even Goldman’s biggest FICC bull just turned bearish .

To the upside we will likely see markets first stage at 4200 (rather than blow through it). Should we stage at 4200 and then see Call Walls roll higher, its our signal that more upside is “available” to the S&P.

We will follow up this post with an extended analysis (available to pro subs since this morning) from one of the most promiment Goldman trading desk bulls who just turned uncharacteristically bearish saying “I am flipping to a tactical bear for a few weeks right here, after the best start to the year for the 60/40 since 1987.” Stay tuned.

Loading…

[ad_2]

Source link

Americans Expect Worsening U.S. Economy in 2023, WSJ Poll Finds

Notable Quotable | Today’s top gold news and opinion