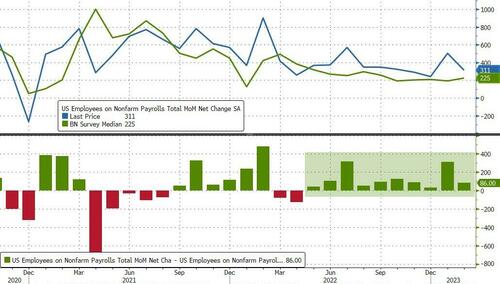

February Payrolls Come In Hot At 311K – Record 10th Beat In A Row – But Unemployment Rate Unexpectedly Rises

If the already jittery market needed another reason to be very confused today, it got it moments ago when the BLS reported February jobs data and which -on one hand – came in hotter than expected at the headline level, with some 311K jobs reportedly created in February, which while was a drop from last month’s downward revised 504K, was well above the 225K consensus and was also above the whisper number of 250K.

The change in total nonfarm payroll employment for December was revised down by 21,000, from +260,000 to +239,000, and the change for January was revised down by 13,000, from +517,000 to +504,000. With these revisions, employment gains in December and January combined were 34,000 lower than previously reported.

Putting this number in context, this was a record 10th consecutive beat to consensus expectations.

But while the headline payroll number was hotter than expected – driven mostly by retail workers and waiters – the not so good data come from the unemployment rate, which unexpectedly jumped from 3.4% to 3.6%, and above the 3.4% consensus estimate as the number of unemployed workers jumped from 5.694MM to 5.936MM, more than the number of Employed workers (which increased from 160.138MM to 160.315MM), while the labor force increased by 1.7 million workers in the past 3 months.

Among the major worker groups, the unemployment rate for Hispanics (5.3 percent) increased in February. The unemployment rates for adult men (3.3 percent), adult women (3.2 percent), teenagers (11.1 percent), Whites (3.2 percent), Blacks (5.7 percent), and Asians (3.4 percent) changed little over the month.

The underemployment rate also rose modestly, from 62.4% to 62.5%.

Elsewhere, the infamous Birth-Death adjustments added 176K, vs a decline of -144K in Jan; there’s half the modeled gain.

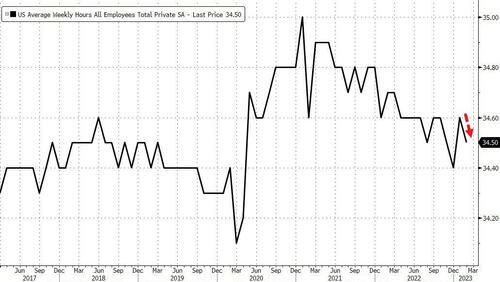

There was also some relief in wage growth, as average hourly earnings rose 0.2% M/M, down from 0.3% in January and below the 0.3% consensus estimate. This translated to a 4.6% increase YoY, which was also below the 4.7% consensus estimate (largely due to a base effect).

The increase may also be due to a decline in the denominator: average weekly hours worked dropped from 34.6 to 34.5.

- The number of job losers and persons who completed temporary jobs increased by 223,000 in February to 2.8 million.

- The number of persons jobless less than 5 weeks increased by 343,000 to 2.3 million in February, offsetting a decrease in the prior month. The number of long-term unemployed (those jobless for 27 weeks or more), at 1.1 million, changed little in February and accounted for 17.6 percent of the total unemployed.

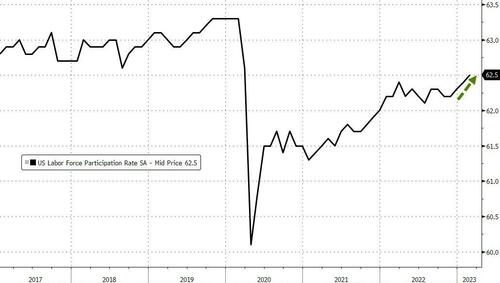

- In February, the labor force participation rate was little changed at 62.5 percent, and the employment-population ratio held at 60.2 percent. These measures have shown little net change since early 2022 and remain below their pre-pandemic February 2020 levels (63.3 percent and 61.1 percent, respectively).

- The number of persons employed part time for economic reasons, at 4.1 million, was essentially unchanged in February. These individuals, who would have preferred full-time employment, were working part time because their hours had been reduced or they were unable to find full-time jobs.

- The number of persons not in the labor force who currently want a job was little changed at 5.1 million in February. These individuals were not counted as unemployed because they were not actively looking for work during the 4 weeks preceding the survey or were unavailable to take a job.

- Among those not in the labor force who wanted a job, the number of persons marginally attached to the labor force was little changed at 1.4 million in February. These individuals wanted and were available for work and had looked for a job sometime in the prior 12 months but had not looked for work in the 4 weeks preceding the survey. The number of discouraged workers, a subset of the marginally attached who believed that no jobs were available for them, also changed little over the month at 363,000.

Drilling deeper into the Establishment report, we find the following details:

- Leisure and hospitality added 105,000 jobs in February, similar to the average monthly gain of 91,000 over the prior 6 months. Food services and drinking places added 70,000 jobs in February, and employment continued to trend up in accommodation (+14,000).

- Employment in retail trade rose by 50,000 in February, reflecting a gain in general merchandise retailers (+39,000). Retail trade employment is little changed on net over the year.

- Government employment increased by 46,000 in February, about the same as the average monthly gain of 44,000 over the prior 6 months. Employment in local government continued to trend up in February (+37,000).

- Employment in professional and business services continued to trend up in February (+45,000), with a gain of 12,000 in management, scientific, and technical consulting services.

- Health care added 44,000 jobs in February, compared with the average monthly increase of 54,000 over the prior 6 months. In February, job growth occurred in hospitals (+19,000) and in nursing and residential care facilities (+14,000).

- Construction employment grew by 24,000 in February, in line with the average monthly growth of 20,000 over the prior 6 months.

- Employment in social assistance rose by 19,000 in February, similar to the average monthly gain of 22,000 over the prior 6 months.

- In February, the information industry lost 25,000 jobs. Employment continued to trend down in motion picture and sound recording industries (-9,000) and in telecommunications (-3,000). Employment in information has decreased by 54,000 since November 2022.

- Transportation and warehousing lost 22,000 jobs in February, including 9,000 in truck transportation. Employment in transportation and warehousing is down by 42,000 since October 2022.

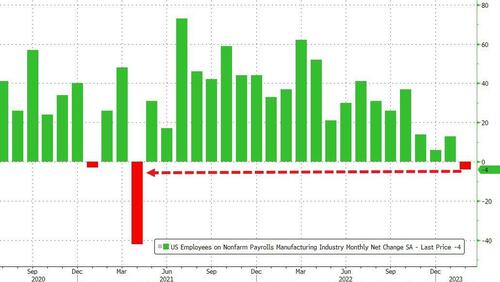

Of the above, perhaps most notable is that manufacturing employment lost jobs for the first time since April 2021.

So what to make of this data, and why are stocks higher after kneejerking lower initially?

Bloomberg’s chief US economist Anna Wong says that “February’s extremely strong jobs report exceeded expectations — and, following January’s blowout report, means the Fed will likely follow through with Powell’s statement in his semiannual congressional testimony about accelerating the pace of rate hikes. That said, there are some signs of weakening in the print — Hours worked slowed, and average hourly earnings cooled faster than expected – that are consistent with our read that the labor market is softening. Still, with inflation elevated, the Fed will have to take the data in this report at face value. We have upgraded our baseline to a 50-basis-point hike at the March FOMC meeting.”

According to TD Securities’ strategist Priya Misra, one of the reasons the market is sharply higher is because it is reacting to average hourly earnings coming in weaker than forecast:

“I guess it lowers pressure on the Fed to go 50bp but the labor market is still strong and wages are running at 4.6% (far greater than the 3.5% that the Fed needs). The Fed will not stop hiking until they see the labor market weaken so we think that the 2s10s curve should flatten. We should see the market keeping some risks of a 50bp hike in March. Not a bad report for risk assets but financials loom larger. We stay long 10s here.”

Here, however, KPMG chief economist Diane Swonk countered “don’t get so excited about the slowdown in earnings” as the payroll gain as more important. “This keeps a half-point hike on the table because of the sheer volume of paychecks that we’re generating, which is buoying demand. At the end of the day what the Fed is worried about is how strong demand is relative to supply. The issue is not wages; it’s aggregate demand. And this is feeding into aggregate demand, which is buoying inflation.”

According to Omair Sharif, founder of Inflation Insights, today’s report is “just what the Fed ordered.”

“This report screams soft landing and looks to be a pretty good one for the Fed.”

If only the US banking sector were screaming the same…

Loading…

[ad_2]

Source link

Zelensky Says Ukraine Needs More New Weapons, Faster

US budget deficit widens to $1.1 trillion in fiscal half year