Status of US Dollar as Global Reserve Currency and Exchange Rates: Slow Long-Term Decline on Track

But the Chinese Renminbi didn’t make any progress at all last year.

By Wolf Richter for WOLF STREET.

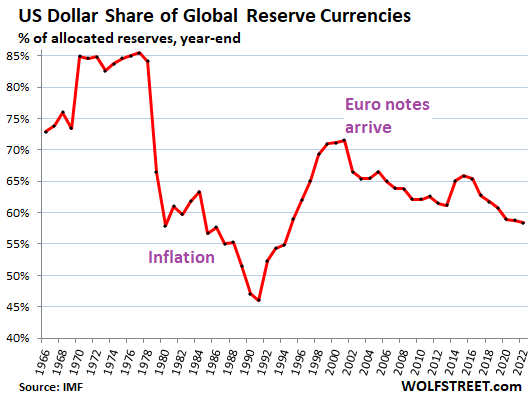

The share of the US-dollar as global reserve currency dropped to 58.4% at the end of Q4, according to the IMF’s new COFER data. This was the dollar’s lowest share of global reserve currencies since 1994.

Back in 1978, the dollar’s share started plunging from around 85% of global exchange reserves as inflation exploded in the US, and other central banks got cold feet holding securities denominated in this stuff. In the 1980s, inflation started to come down. But central banks – and the rest of the world – took a long time to regain confidence in the dollar, and the dollar’s share of reserve currencies didn’t bottom out until 1991, with a share of 46%. Then came the bounce until the euro showed up, which put a stop to the bounce. The chart shows the share of the dollar at the end of each year.

The US dollar as global reserve currency means that foreign central banks and other foreign official institutions hold US-dollar-denominated assets, such as US Treasury securities, US corporate bonds, US mortgage-backed securities, and the like.

These institutions also hold foreign exchange reserves other than dollar-assets. But holdings in their own local currency are not included in foreign exchange reserves; so holdings of dollar-denominated assets by the Federal Reserve are not included; holdings of euro-denominated assets by the ECB are not included, etc. Same for other central banks: their local-currency assets are not included.

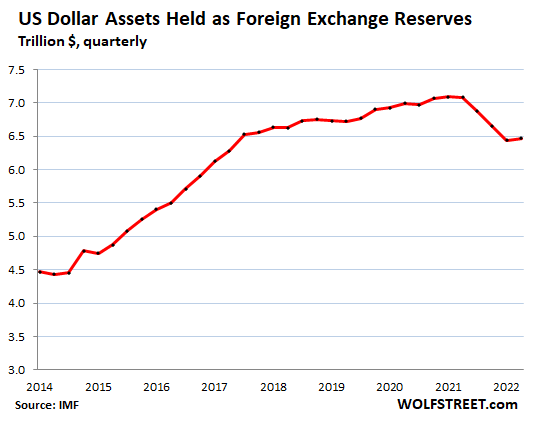

In dollar terms, at the end of Q4, central banks other than the Fed held $6.47 trillion in USD-denominated assets, such as US Treasury securities, US corporate bonds, and US mortgage-backed securities.

Even as the dollar’s share has dropped since 2014, holdings of dollar-assets rose from $4.4 trillion in 2014 to $7.1 trillion in Q3 2021. But then, note the $621 billion drop in USD holdings starting in Q4 2021, which was when the Fed started talking about ending QE and kicking off rate hikes – and by now it has hiked by 475 basis points.

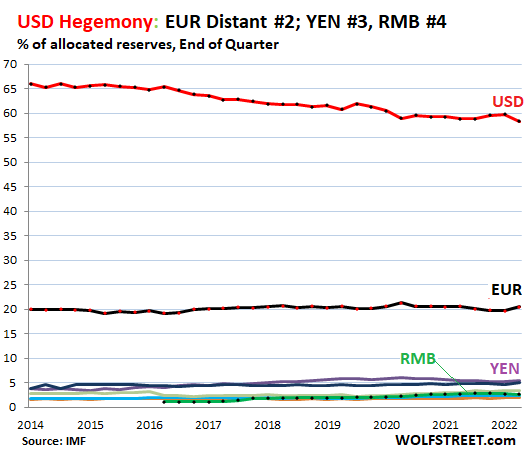

The other major reserve currencies.

The euro is the second largest reserve currency, with a share of 20.5% at the end of 2022. Back in the day when the euro was created, there was talk that it would reach “parity” with the dollar, but the Euro Debt Crisis brought to light the euro’s structural weakness, which ended the parity talk, and the euro has maintained a share of roughly 20% since then.

The yen, the third-largest reserve currency, had a share of 5.5% (purple line at the top of the colorful spaghetti at the bottom in the chart).

The British pound, the fourth largest reserve currency, had a share of 4.9% (blue line just under the yen).

The Chinese renminbi, the fifth largest reserve currency, lost a little ground last year, with its share dipping to 2.7% at the end of 2022. Due the capital controls, convertibility issues, and other issues, it seems central banks are leery of RMB-denominated assets and are moving slowly or not at all. At this pace, the RMB won’t get close to the USD as reserve currency for decades (green line near the very bottom).

The other currencies in the spaghetti: Canadian dollar (2.4%), Australian dollar (2.0%), and Swiss franc (0.2%). There is a number of other currencies with a tiny share each (each less than the Swiss franc’s share), and all of them combined have a share of 3.4%.

Dollar-exchange rates impact foreign exchange reserves.

The values of foreign exchange reserves denominated in euros, yen, British Pound, RMB, and other currencies are translated into USD figures at the exchange rate at the time, for reporting purposes, so that they can be summed and compared.

For example, the value of Japan’s official holdings of euro-denominated assets is expressed in dollars at the EUR-USD exchange rate at the time. So the magnitude, expressed in dollars, of euro-denominated assets held by Japan rises or falls with the USD-EUR exchange rate, even if Japan’s holdings don’t change.

In other words, the exchange rate between the USD and other reserve currencies impacts the magnitude of the non-USD assets.

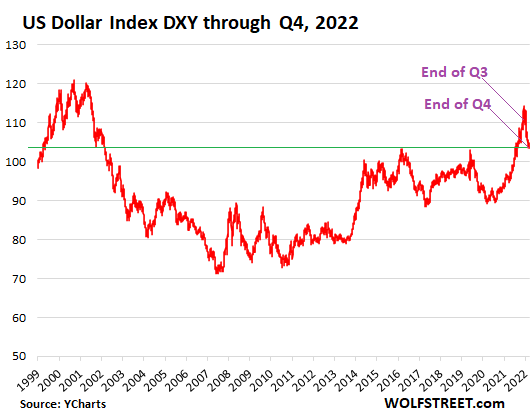

Since 2000, the exchange rates of the major currency pairs have bounced up and down within a fairly wide band, as shown by the Dollar Index [DXY], which is dominated by the euro and yen, but also tracks the British pound, Canadian dollar, Swedish krona, and Swiss franc.

At the end of Q4, the IMF’s cutoff point for this reserve currency data, the DXY closed at 103.4, where it had been in the year 2002, but with a lot of scary rollercoaster rides in between (data via YCharts):

So the dollar’s exchange rate with the euro and the yen at the end of 2022 was roughly where it had been in 2002. But back then, the dollar’s share of reserve currencies had been 66.5%; and at the end of 2022, it had fallen to 58.4%. So the decline in the dollar’s share is not due to exchange rates.

Trade surplus and large reserve currency, no problem.

The Eurozone – whose currency is the #2 reserve currency with a 20% share – has had a trade surplus with the rest of the world in recent years, particularly with the US. This shows that an economy with a trade surplus can also have one of the top reserve currencies, disproving some theories that the country with a large reserve currency must have a large trade deficit.

The big enabler: But having the dominant reserve currency enables the US to run up its twin-deficits: the gigantic US government deficit and the monstrous trade deficit, fueled by Corporate America’s three-decade search of cheap labor, products, and services. If in the future the USD-denominated assets lose a lot of share among reserve currencies, both of these deficits will be more difficult and expensive to fund.

China: It is also likely – and I think good for the global and even the US economy – that China’s RMB-denominated assets, given the huge size of the economy, will eventually ever so slowly become a larger player amid global exchange reserves.

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the beer and iced-tea mug to find out how:

Would you like to be notified via email when WOLF STREET publishes a new article? Sign up here.

![]()

[ad_2]

Source link

An Evidence-Based Look At Inflation, Recessions and Pivots

The Outer Limits of Central Banking: “We Will Control the Horizontal. We Will Control the Vertical.”