Short End of the Treasury Market Goes Totally Nuts. Doubts Creep in Over Debt Ceiling?

The good folks in Congress are surely too worried about their own wealth, and sheer greed will keep them from pushing the US into default. But…

By Wolf Richter for WOLF STREET.

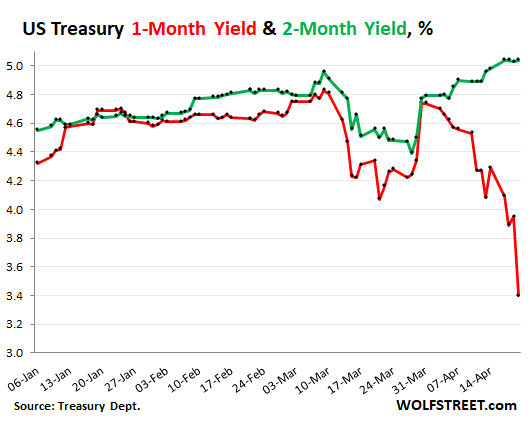

Today was another weird mess – and by far the biggest weird mess – in a series of daily weird messes in the very short end of the Treasury market, with Treasury securities that have remaining maturities of around one month. The one-month yield plunged 55 basis points today to 3.40% at the close – meaning prices of these securities jumped amid huge demand. Intraday was down as much as 75 basis points. Panic-buying frenzy! Since March 31, the one-month yield has plunged 134 basis points (red line below).

But, but, but… the two-month yield – so tracking Treasuries maturing in about two months – was very well behaved, smiled all day long, ticked up 1 basis point to 5.04%, and was up 25 basis points since March 31 (green line).

There is now an unspeakably crazy spread of 164 basis points between the one-month yield and the two-month yield – a sign that some people are panicking and piling into whatever they will be out of at face value in about one month.

The rest of the Treasury market was reasonably well behaved. The two-month to six-month yields all ended above 5%, with the four-month at 5.17%. The two-month yield rose. All other yields fell. For example the two-year yield fell by 10 basis points to 4.14%, after having hit yesterday the highest yield since March 13. The 10-year yield fell 6 basis points. And the 30-year yield fell 4 basis points. It was just the very short end that went nuts.

The cost of insuring US government debt against default has been rising for weeks. Today, the spread on 5-year US credit default swaps jumped further, to a decade high, nearly doubling from the beginning of the year, according to S&P Global Market Intelligence.

There is now a lot of speculation why some people are panickily piling into something that they will get paid back in about one month, and why they’re so eager to pile into it that they’re paying extra to do so, while the rest of the bond market is just sort of fine, within the massive inversion of the yield curve. The stock market doesn’t really care about anything anyway. So for most people, today was a non-event.

But some people are getting antsy about a US default.

The debt-ceiling farce being performed currently in Congress could turn from a mildly entertaining political show that has been played 79 times since 1960, and whose ending everyone knows, into a truly hilarious financial show with a new ending where the debt ceiling isn’t lifted, and where the US will then default on some of its obligations, and where everyone in Congress – these folks are rich – will lose 60% or whatever of the value of their financial assets in no time.

I’m curious to see how they would spin that one. Surely, everyone would blame everyone else. I’m also curious if anyone in Congress is actually hedging their financial assets against that kind of event.

Today’s problem was that tax receipts from Tax Day were somewhat lackluster, which might move the out-of-money-date, the X-date, a little closer than previously anticipated.

The X-date is when the Treasury Department will run out of “extraordinary measures” (I explained those here) and will run out of cash in its checking account, the Treasury General Account at the New York Fed.

The Treasury Department might then begin to prioritize what it will pay and what it will not pay, for example it would stop paying for salaries, travel reimbursements, and toilet paper for everyone in Congress. At least, that’s where I would start.

If the debt ceiling doesn’t get raised quickly after the initial failure to raise it, eventually, the US government might not have enough cash on hand to be able to redeem a bond issue when it matures, and holders of these securities who thought they would get paid face value at the end of June might not get paid anything at the end of June, which would represent a maturity default, which would be very messy. Globally.

Obviously, this isn’t going to happen, knock on wood. The good folks in Congress are surely too worried about their financial wealth, and surely, sheer greed will force them to agree on a deal. But the bet today was that maybe, just maybe, this calculus could be wrong. And it infused a little bit of suspense – as they usually try to do – into the farce so that not everyone will fall asleep, and so that they’ll get a little more political traction with it.

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the beer and iced-tea mug to find out how:

Would you like to be notified via email when WOLF STREET publishes a new article? Sign up here.

![]()

[ad_2]

Source link

Comex Inventory: 17.4 Paper Ounces of Silver for Each Registered Ounce

There’s a problem in the money market, even if US 10Y rates stay below 4%