Why I’m Skeptical of Powell’s Claim Red-Hot Rent CPI Will Just Vanish: Landlords Report the Opposite, even for April

High demand by renters of choice trying to outwait the housing turmoil pushes up actual rents in a range of 6% to 8%.

By Wolf Richter for WOLF STREET.

Landlords and tenants are throwing a bucket of cold water on hopes that rent inflation will back off – it just doesn’t seem to be happening.

These reports have been coming in from the largest landlords of single-family houses and from multifamily landlords. The largest landlords of single-family houses are publicly traded, and so they report operational details, such as actual rent increases for lease renewals for newly executed leases on a same-house basis. The apartment data is based on millions of actual transactions, renewals and new leases.

They’re actual rents that tenants pay. Changes in actual rents for specific rental units are also the base for the rent inflation measures in the Consumer Price Index and the PCE price index.

None of them include “asking rents,” which are the advertised rents that landlords want to get for their vacant apartments, whether or not they’re actually able to lease at those asking rents. Zillow, Zumper, Apartment List, and others report “asking rents.” The double-digit spikes last year occurred in asking rents, not in actual rents.

Rent increases reported by the largest single-family rental landlords.

Invitation Homes [INVH], in its earnings call for Q1 on May 2, said that rent growth in April showed “further acceleration” in newly executed leases:

- April new lease rent increase: +7.5%

- April renewal rent increase: +7.2%

- April blended rent increase: +7.3%.

In terms of Q1, it said, “We have also seen stronger demand return following the winter leasing season, with new lease rent growth accelerating sequentially each month during the first quarter”:

- Q1, new lease rent increase: +5.7%

- Q1, renewal rent increase: +8.0%

- Q1, blended rent increase: +7.3%.

American Homes 4 Rent [AMH], in its Q1 earnings call on May 5, said that “strong demand continues to fuel solid occupancy and rental rate growth,” in Q1 and continued in April.

- April new lease rent increase: +9.4%

- April renewal rent increase: +6.2%

- April blended rent increase: +7.1%

Which were “well above our seasonal pre-pandemic norms,” it said.

- Q1 new lease rent increase: +7.8%

- Q1 renewal rent increase: +6.8%

- Q1 blended rent increase: +7.1%

Which “drove same-home core revenue growth of 7.7% for the quarter,” it said.

John Burns Research & Consulting reported some “takeaways” from the National Rental Home Council Industry Leaders Conference, including this:

“Rent Increases Driven by a Substantial Shift to Renters by Choice.”

“The tenant profile in professionally managed build-to-rent and single-family rental communities is significantly shifting. There is a growing trend of even more tenants choosing to rent single-family homes rather than buy one. More prospective homeowners believe that prices and rates will come down and more resale buying opportunities will emerge, so they are delaying their home buying.

“This shift has led to a rise in the number of renters who are less rent-sensitive, creating demand for higher-quality rental properties.

“These renters, by choice, value superior interior finishes, better amenities, and overall design, which were not commonly available 15 years ago. As a result, property owners and managers can command a premium for such properties.”

Multifamily apartment rents continue to surge.

The National Multifamily Housing Council last week released its industry benchmark report for January (the delay is to comply with federal antitrust guidelines, it says). This data is based on executed transactions tracked by RealPage from over 13 million rental apartments in over 400 markets. “Asking rents” for vacant units are not included:

- New leases (per square foot): +8.9%

- Rent at renewal (effective rent on the same unit): +8.4%.

You get the idea.

Lots of demand for rentals, given the high cost of ownership. A lot of people are now asking the question why buy the house, when you can lease a similar house for a lot less and outwait the situation – falling home prices and high mortgage rates.

And this relatively high demand by people who are renters of choice, who got the biggest wage increases in 40 years, is pushing up rents. That dynamic has been in place for a couple of years. And it hasn’t vanished at all, but appears to accelerate, based on these reports from the industry.

Rents are a big factor in CPI and PCE price index.

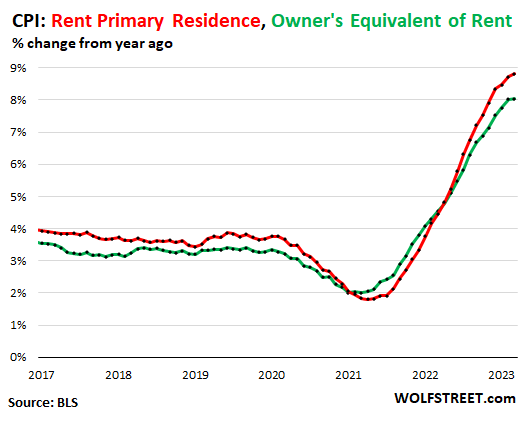

The Consumer Price Index for April will be released this week. About one-third of the CPI is “shelter,” based on two rent factors: Owner’s Equivalent of Rent and Rent of Primary Residence.

Both factors have shot up last year and this year. In March, OER was 8% and Rent hit 8.8%. The incremental increases slowed in March, and will likely slow further, and the year-over-year increases likely peaked, with annual rent inflation eventually dipping below that 8% level.

And those indices continue to be in line with what landlords are reporting.

We can see in the data reported by landlords that 6% to 8% increases in actual rents – renewals and newly executed leases, which is also how CPI measures rents – are currently playing out. So this is a little slower than the CPI rent increases in the range of 8% to 9%.

But the 6% to 8% range is a far cry from the hoped-for massive decline in rents – hopes that were espoused by big drops in “asking rents” off of the double-digit spike last year. But neither the spike nor the drop-off from that spike made it into actual increases that tenants are actually paying at renewal and when signing new leases.

So it seems unlikely that Fed chair Jerome Powell’s assumption will play out that rent inflation will be slowing sharply in a few months, and that actual rents are already going down, and that rent inflation will reach the point where it will no longer be an issue, and that the CPIs for rent are heading back to the 2% to 3% range, and that this decline is already baked in because the rent indices are lagging indicators, etc. etc.

It seems much more likely, based on these actual rent increases, that rent inflation will remain well in the hot range, above 6%, and that it will not help push down the services inflation measures and “core” inflation measures that the Fed is now so focused on.

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the beer and iced-tea mug to find out how:

Would you like to be notified via email when WOLF STREET publishes a new article? Sign up here.

![]()

[ad_2]

Source link

Q&A With Peter Schiff | SchiffGold

Central Banks Continue to Have an Appetite for Gold