Households Far from “Tapped Out”: Credit Card Balances, Burden, Available Credit, Delinquencies & Collections

Credit cards are a huge payment method but not a big borrowing method.

By Wolf Richter for WOLF STREET.

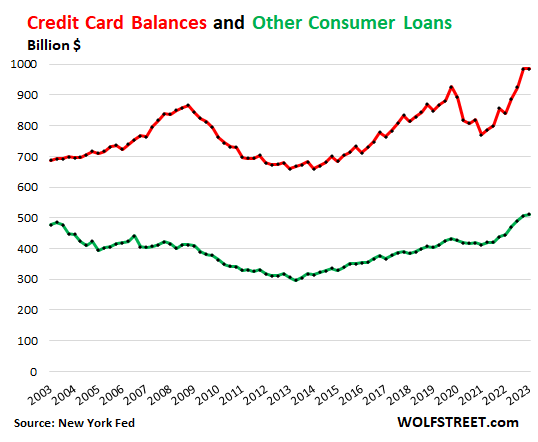

For the first time in at least two decades, credit card balances remained unchanged in Q1 from the Q4 holiday spending binge, rather than dropping. In the data going back to 2003, credit card balances always dropped in Q1 from Q4, and often by large amounts. But this was the first time they didn’t drop. Which shows just how strong spending has been in Q1, because credit card balances are mostly a measure of spending and prices rather than a measure of debt.

At $986 billion, credit card balances were up 17.2% year-over-year, according to the New York Fed today.

Credit cards as payment method not borrowing method. Consumers use their credit cards mostly as payment method and pay off their credit cards every month. According to the Federal Reserve in April this year, consumers used their credit cards to pay for $4.9 trillion in purchases in 2021.

Most of these $4.9 trillion in charges were paid off by due date and never accrued interest. But because the due-date is after the end of the month, the month-end balances that never accrue interest and are paid off a few days later still show up as credit card balances in the reports. So what we’re looking at here is largely a measure of spending via credit cards and to a smaller extent interest-bearing credit card debt.

“Other” consumer loans, such as personal loans, payday loans, and Buy-Now-Pay-Later (BNPL) loans, ticked up by $5 billion, to $512 billion. Over the past two quarters, they finally edged above the high from 20 years ago. Unlike credit card balances, most of these “other” balances are interest bearing, but not all: For example, BNPL loans tend to be interest-free and are subsidized by the retailer.

Credit card balances (red) and “other” consumer credit (green) combined amounted to $1.50 trillion

Banks incentivize the use of cards as payment method by offering 1.5% or 2% cash-back on card spending or frequent flyer miles, etc. The bank that issued the card collects a fee from the merchant, retains part of the fee as profit and kicks part of the fee back to cardholders as an incentive to run more payments through the card so that the bank can collect more fees.

Banks discourage borrowing on credit cards by charging huge interest rates. And a large majority of cardholders got the memo eventually, and they pay off their credit cards every month to avoid interest charges.

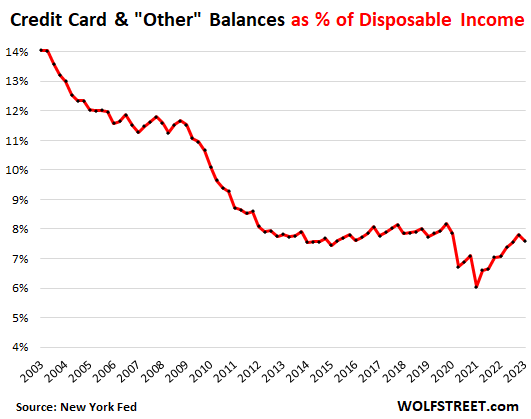

Households are not burdened by these balances.

As a percent of disposable income, credit card balances and “other” consumer debt combined in Q1 dipped to 7.6%, after two years of increases from the historic low during the pandemic (disposable income = income from all sources minus taxes and social insurance payments).

In the good old days 20 years ago, credit card balances amounted to 14% of disposable income:

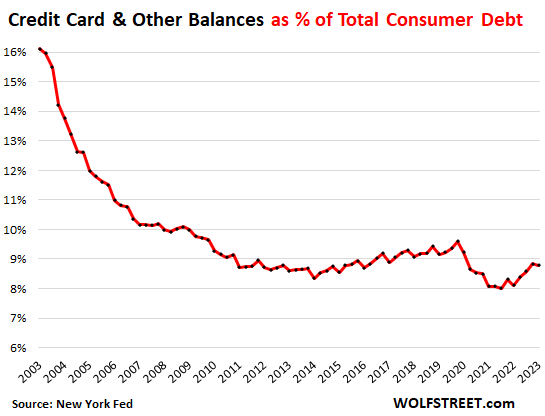

Credit card balances’ share of consumer debt fizzles.

Credit card balances and “other” consumer debt combined amounted to only 8.8% of total consumer debt – which also includes mortgages, HELOCs, auto loans, and student loans. This is down from 16% two decades ago:

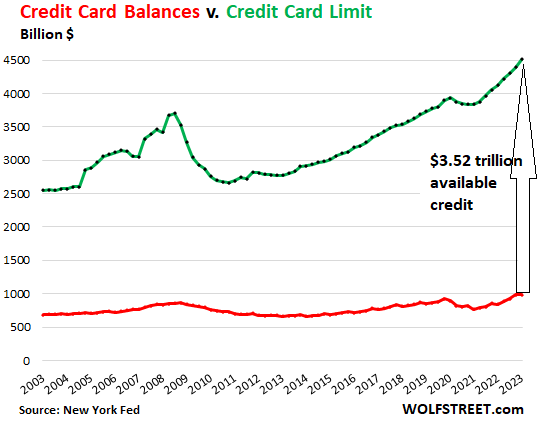

$3.52 trillion in available unused credit.

Despite rumors of a “credit crunch,” banks raised the aggregate credit limits on credit cards to $4.51 trillion. With only $986 billion in credit card balances outstanding, the total available unused credit rose to record $3.52 trillion:

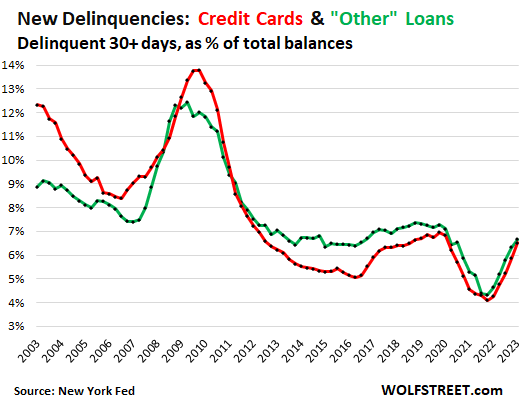

Delinquent balances tick up, but still below pre-pandemic.

The pandemic money, the eviction bans, and the various forbearance programs that washed over consumers had the effect of reducing delinquencies to record low. Those times are over, and delinquencies on credit card balances and “other” consumer credit are reverting to the Good Times levels before the pandemic.

Credit card balances that transitioned into delinquency as they became 30 days or more past due during the quarter rose to 6.5% (red), compared to 6.7% in Q1 2019. During the Great Recession, delinquent credit card balances spiked to nearly 14%.

Balances of “other” consumer loans that transitioned into delinquency rose to 6.7%, compared to 7.3% in Q1 2019:

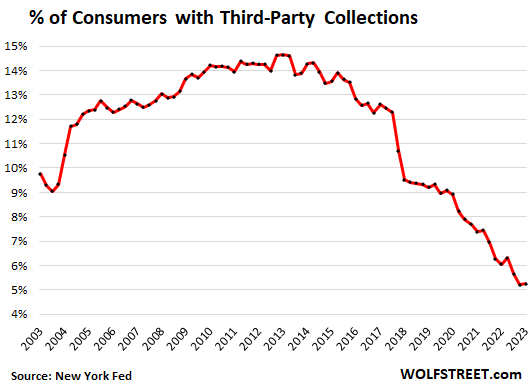

Third-party collections remain at historic low.

Third-party collections are where defaulted credit card accounts and “other” credit accounts tend to eventually end up after banks sell the accounts for cents on the dollar to wash their hands off them. This is our final step in the health checkup of credit cardholders. The percentage of consumers with third party collections remained at the historic low of 5.2%, down from 14.6% of consumers after the Great Recession:

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the beer and iced-tea mug to find out how:

Would you like to be notified via email when WOLF STREET publishes a new article? Sign up here.

![]()

[ad_2]

Source link

Interest Rates and Fed Tightening

Does Gold Really Preserve Purchasing Power? The Case of the High-End Suit