Delinquencies in Subprime Auto-Loan-Backed Securities Have Second-Worst April Ever, Behind only Lockdown April: The Cost of Free Money

In the free-money era, subprime auto lenders took huge risks amid seething demand from yield-chasing investors.

By Wolf Richter for WOLF STREET.

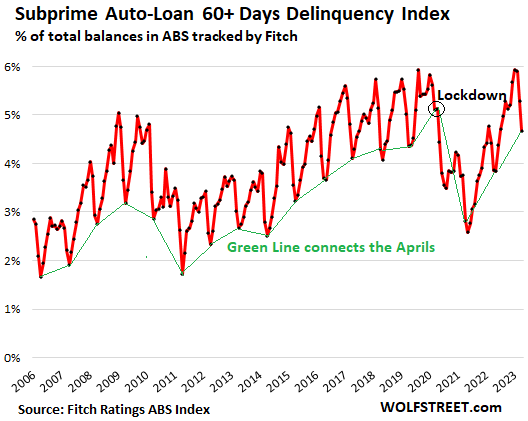

Let me just start with this chart of subprime auto-loan delinquencies of 60 days and over in the Asset-Backed Securities (ABS) rated by Fitch Ratings. In recent years, the worst delinquency rate was set in August 2019, of 5.93% of total balances, nearly matching the all-time worst record of 5.96% in October 1996. Then came the free-money era, when delinquencies plunged. When the free-money era ended, delinquencies spiked, and in January 2023 hit 5.93% again.

Every month since then, delinquencies declined. In April, they dropped to 4.67%. But wait… The drop was entirely seasonal. April is usually the month with the lowest delinquency rate of the year. If not April, then May is the lowest month. So in April 2023, the delinquency rate of 4.67% was the second worst April ever, behind only the lockdown April 2020. The green line connects the Aprils:

The reckless deals of the Free Money Era.

Auto loans are rated “subprime” for the same reason a lot of bonds are rated “junk” (BB+ and below): the borrower has a much higher risk of defaulting on the debt. And investors take big risks to make lots of money.

Subprime auto loans account for only about 14% of total outstanding auto loan balances and leases. The remaining 86% are prime-rated. Subprime auto loans are generally concentrated on older used vehicles with smaller amounts financed.

These subprime delinquencies are not a sign that the overall consumer is getting in trouble or whatever. We can see that because prime-rated auto loans are in pristine shape with a 60-day delinquency rate of only 0.2%, according to the ABS rated by Fitch. In other words, nearly all delinquencies are in the relatively small subprime-rated pocket of auto loans, and the prime delinquency rate remains near historic lows.

But these subprime delinquencies are a sign that subprime lending by specialized lenders had gotten very loosey-goosey, with ridiculous Loan-to-Value ratios and super-loose, often AI-driven underwriting standards. And this was particularly the case during the free-money era of the pandemic.

Subprime is teeming with abuses and scandals. Some subprime loans come with such high interest rates that practically guarantee the loans will default. Occasionally regulators crack down, but settlements and fines are just part of the cost of doing business.

The risk-taking is driven by potentially high profits, and by the ease with which a vehicle can be repossessed and sold at auction.

A lot of times, customers with subprime credit ratings tried and failed to get financing at a regular dealership, and they ended up going to a dealer that specializes in the subprime end of the business, a high-risk, high-profit business.

And periodically, specialized subprime auto lenders collapse, as we have seen a couple of dealer-lender chains do this year. These dealer chains held on to the loans they wrote, and once a year they securitized the big pile of loans into subprime auto-loan Asset Backed Securities (ABS) and sold them to investors, such as bond funds and pensions funds, while retaining the equity portion of the ABS.

These ABS are structured to where the lowest-rated slices take the first losses, and get wiped out first, but they’re also sold with the highest yield to compensate investors for taking those risks. As the losses increase, the holders of the higher slices begin to eat them. The highest slices might carry an “A” rating when issued, and they’re sold with the lowest yield.

Delinquency rates of these subprime auto-loan ABS had fallen to low levels during the pandemic, when the free money was washing through the system. But then they rose back to the high levels of the pre-pandemic years, plus some.

And subprime auto-loan underwriting had gotten very loosey-goosey because there had been huge demand by bond funds and pension funds to buy subprime auto-loan ABS because of their higher yield, in a world where yield had been repressed by central banks. These funds were chasing yield, and these private-equity-backed dealer-lenders made a ton of money supplying those ABS to the yield chasers. Then the loosey-goosey loans turned sour, and the Fed hiked rates, and two of those chains collapsed.

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the beer and iced-tea mug to find out how:

Would you like to be notified via email when WOLF STREET publishes a new article? Sign up here.

![]()

[ad_2]

Source link

Despite Dismal Start To Commodities, Goldman Sees Delayed Surge In Replay Of 2007

Has the IMF Told the World to Buy Gold?