Rent Inflation Re-Accelerates to Red-Hot, All Three Now Agree: Zillow Asking Rents, What Big Landlords Said, and Actual Rents Tracked by CPI

Debacle on the Inflation Front: The Fed’s victory lap about having licked rent inflation was premature.

By Wolf Richter for WOLF STREET.

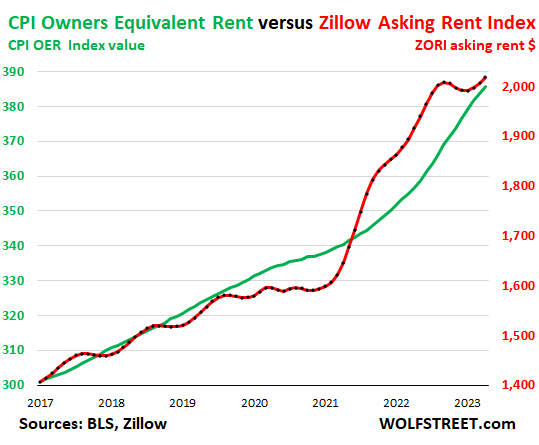

The Zillow Observed Rent Index (ZORI), which is based on asking rents, meaning advertised rents that landlords hope to get when a tenant signs the lease, jumped month-to-month by 0.6% in April, the steepest increase since August, after having already jumped 0.5% in March, and 0.3% in February, to a new record of $2,018. Annualized, the increase in April translates into a jump of +7.4%.

This is really bad news on the inflation front. But it’s not a surprise. It confirms what the biggest landlords in the US told us in their earnings calls, that they got 6% to 8% rent increases both on lease renewals and on new lease signings in April; and it confirms what the rent factors in CPI for April told us, that actual rents paid by all tenants jumped by 0.5% in April from March, and by over 8% year-over-year.

You can see how the ZORI (red, right axis, $) undershot actual rents during the pandemic as depicted by the largest rent factor in CPI (OER, green, index value, left axis), and how it overshot actual rents in 2022, and how it then dipped at the end of 2022 and early 2023, and how it has reaccelerated over the past three months:

Rent accounts for one-third of the Consumer Price Index, split across two rent factors. The CPI for Owners Equivalent of Rent (OER, the larger of the two, accounting for 25.4% of total CPI) jumped by 0.5% in April and by 8.1% year-over-year.

All these measures – asking rents as per ZORI; earnings calls from the biggest landlords in the country; and actual rents for all tenants as tracked by the CPI rent factors – are now showing that rent inflation in April was not slowing down at all, but re-accelerated.

The ZORI was much cited as proof that rent inflation was slowing down and would soon vanish based on the ZORI last year when it actually fell.

For the Fed, for Powell during the press conferences, and for many others, the dropping asking rents last year was the gospel that they had been waiting for, that inflation in actual rents, as experienced by current tenants, would soon abate as the asking rents would become actual rents and lower those actual rents, but that it just hasn’t done so yet because, you know, the CPI rent factors are lagging, etc. etc.

But that didn’t happen.

The year-over-year percentage-change mind-bender.

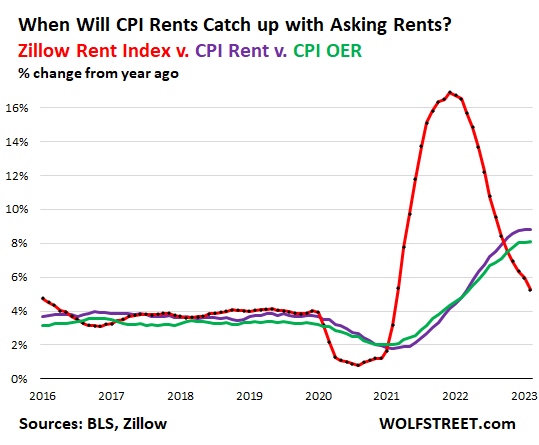

What may have also misled the good folks about rent inflation were the year-over-year changes. As you can see in the chart above, the ZORI undershot actual rent increases in 2020 and early 2021, and then off that low base, showed a massive year-over-year percentage gain in 2022, that caused it to overshoot in 2022.

But that huge percentage gain never made it into actual rents because it was off the undershoot, it just averaged out the undershoot on top of the regular rent inflation of 8%. And now the asking rents per ZORI are back in line on a month-to-month basis with the CPI measures.

This is the type of year-over-year percentage change chart that caused a lot of brains to short-circuit about rent inflation, showing the undershoot in 2020 and early 2021, and off that low base the massive overshoot in late 2021 and nearly all of 2022. This chart also shows the CPI rent factors as year-over-year percentage change.

The Fed’s victory lap.

The Fed divided the core inflation index (without the volatile food and energy products) into three groups: core goods, housing inflation, and core services without housing.

Inflation in core goods has come down a lot from the pandemic highs. Housing inflation measures (such as the CPI rent factors) would also certainly come down because this was already baked in, they said, based on asking rents dropping, and because the CPI rent factors are lagging, they said months ago. So the rent-part of inflation, they said, was already licked. And the only part left where inflation was super-sticky was core services inflation without housing.

So now it turns out, inflation remains nastily sticky in two of the three parts, and the Fed’s victory lap on having licked rent inflation appears to have been premature.

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the beer and iced-tea mug to find out how:

Would you like to be notified via email when WOLF STREET publishes a new article? Sign up here.

![]()

[ad_2]

Source link

‘Warning Lights Flash’ As More Workers Seek Help, Says Citizens Advice

Year of the Pause | GoldSeek