ECB Balance Sheet Plunged by €1.6 Trillion (-18%) from Peak. Bond Roll-Off Speeds Up

Spooked by relentlessly raging inflation in services, ECB puts QT into higher gear.

By Wolf Richter for WOLF STREET.

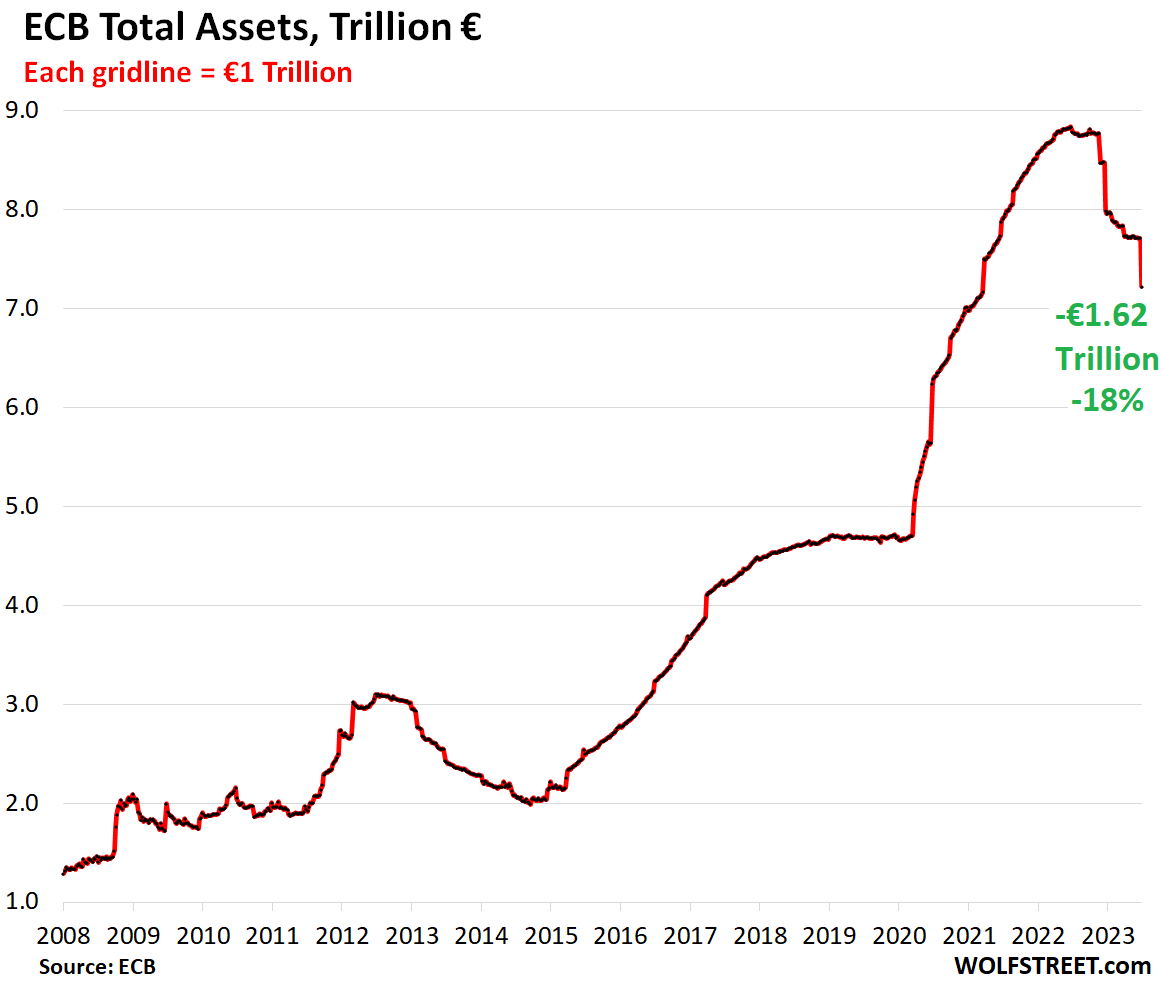

Total assets on the ECB’s balance sheet as of June 30, which was released today, have plunged by €1.62 trillion, or by 18%, from the peak in June last year, to €7.22 trillion, the lowest level since March 2021.

The ECB had two major types of QE that are now unwinding: It offered free loans under very favorable conditions to banks, ultimately handing banks €2.22 trillion in cash to deploy. And it handed €4.96 trillion in cash at the peak to the bond market by purchasing government bonds, corporate bonds, and asset-backed securities.

In October, the ECB announced the first steps of QT, when it made the loan terms unattractive which caused the banks to pay back those loans, thereby removing liquidity via the banks. It later announced the initial steps on unwinding its bond holdings, which started in March. Since then, the ECB has unloaded them at a faster rate than announced.

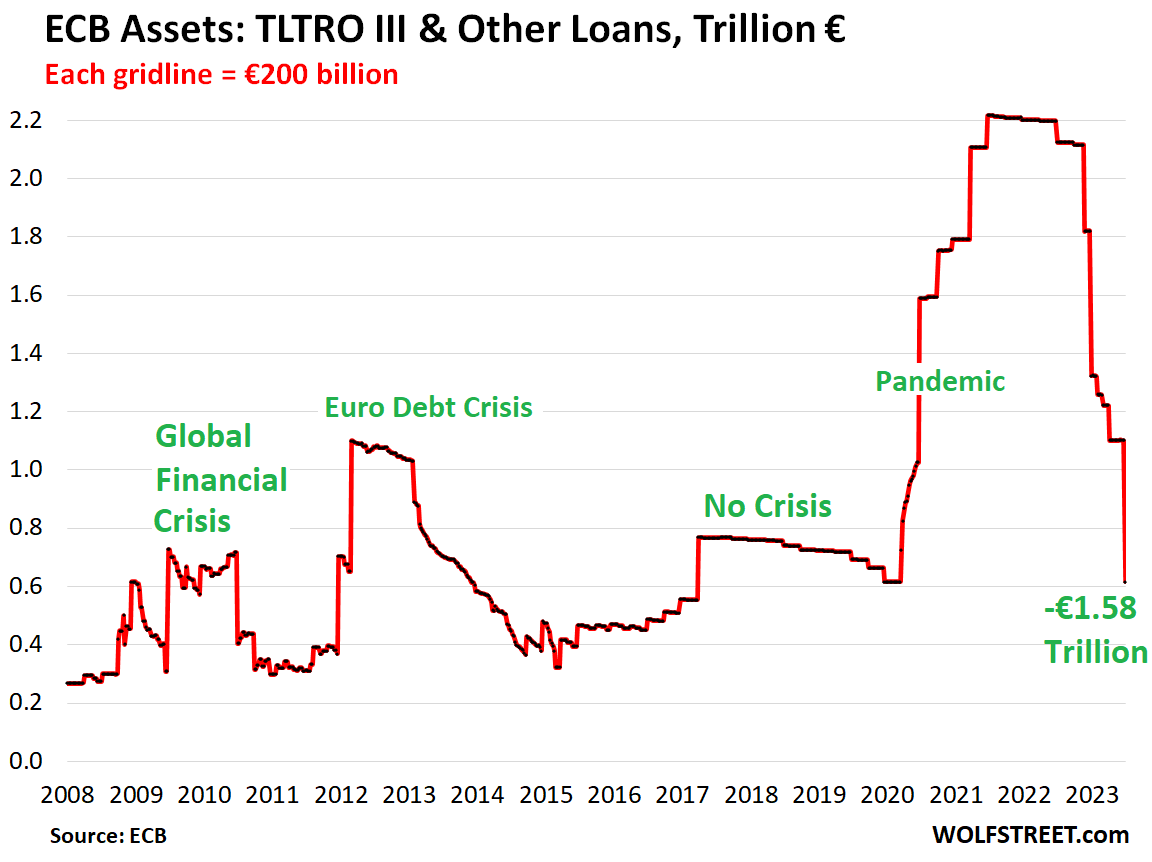

The pandemic-era loan QT unwound: -€1.58 trillion

The ECB has always handled QE via loans – various generations of Longer-Term Refinancing Operations – including during the Financial Crisis and the “whatever it takes” moment of the Euro Debt Crisis in 2012.

During the pandemic, the ECB further expanded these lending operations, called them Targeted Longer-Term Refinancing Operations (TLTRO III), and endowed them with complex incentives for banks. Banks took them and ran with them, to plow this money into whatever. These pandemic-era TLTRO III loans amounted to €1.6 trillion at the peak, which came on top of the still outstanding prior loans, to total at the peak €2.2 trillion.

The loans have dates at which they can be paid back. After the ECB made the loan terms unattractive last October, banks began to pay back those loans. On today’s balance sheet, which is as of June 30, banks paid back another €485 billion in loans, bringing the total reduction of loans to €1.58 trillion so far, with only €617 billion in loans outstanding.

The ECB has now unwound the entire pandemic-era loan pileup and is back at the level where the loan balance was before the pandemic:

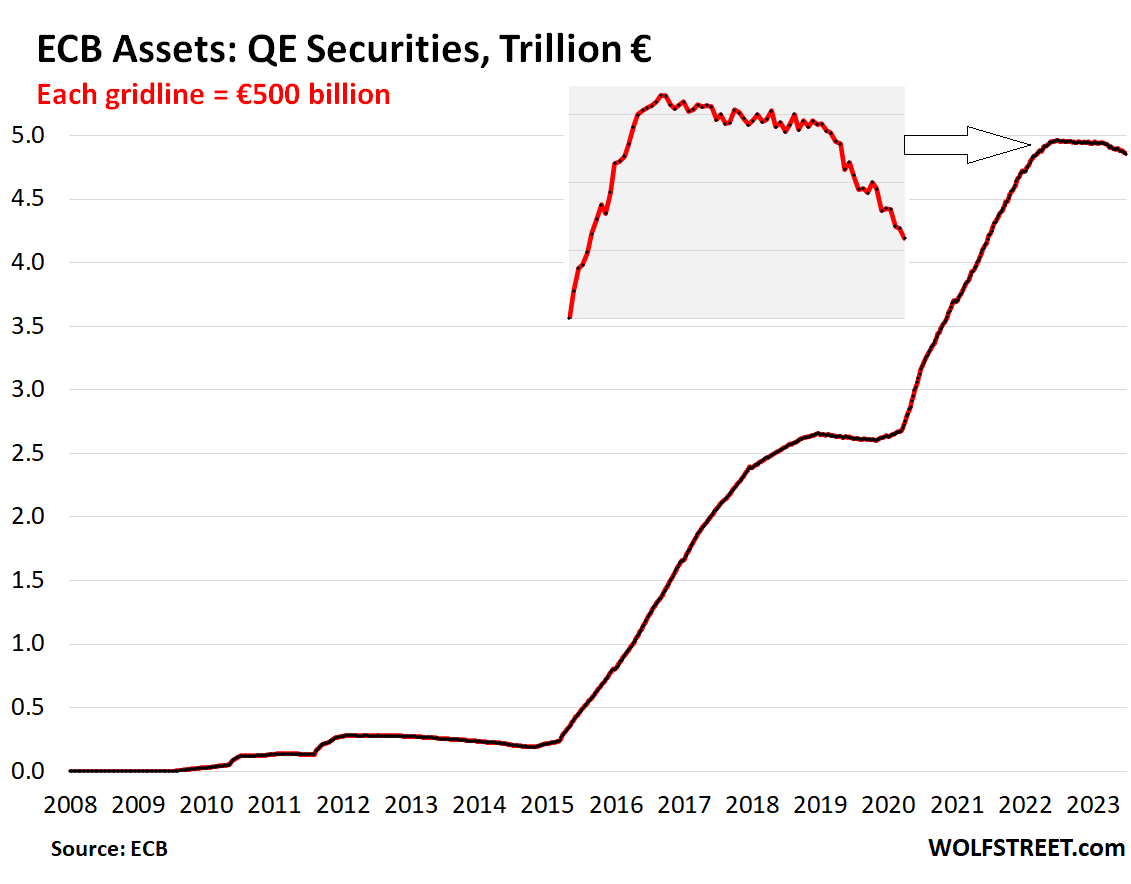

Bond QT faster than announced: -€105 billion

The ECB announced in December that it would let some of its bond holdings roll off, starting in March. It had bought bonds under two programs: APP (asset purchase programme), starting in 2014; and PEPP (pandemic emergency purchase programme), which started in March 2020.

The current roll-off concerns the APP bonds. It said it will maintain its PEPP bond holdings for now.

The APP roll-off was initially capped at €15 billion a month when it started in March through June. At the June meeting, it said that in July it would remove the €15 billion cap from the roll-off of the APP bonds and just let them roll off as they mature.

On the balance sheet released today, as of June 30, the balance of bond holdings was down by €105 billion from the peak a year ago.

The roll-off is proceeding faster than the €15 billion a month pace: Over the past four weeks, its bond holdings fell by €22 billion. Over the four months of bond QT since the beginning of March, its bond holdings fell by €84 billion, averaging €21 billion a month.

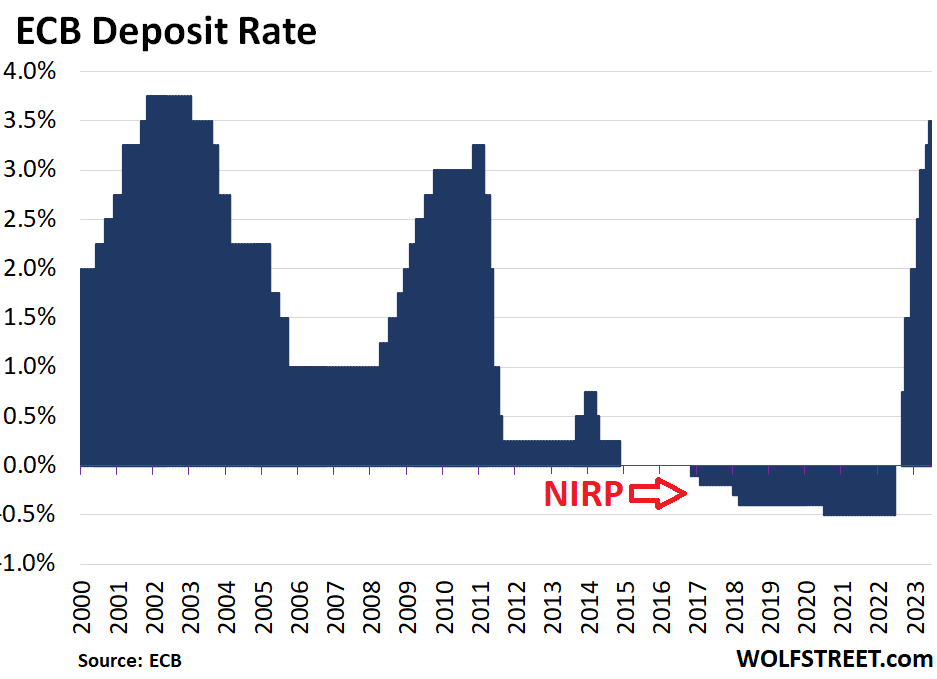

Rate hikes…

The ECB has hiked its policy rates by 4 percentage points in 12 months, bringing its Deposit Rate from -0.5% to +3.5%, the highest since 2003. More hikes are on the table:

Spooked by inflation in services…

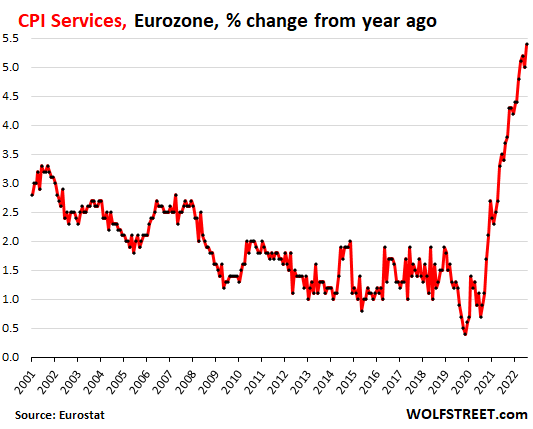

ECB president Christine Lagarde keeps hammering on inflation in services which continues to get worse relentlessly, though energy prices have plunged, red-hot food inflation has started to back off, inflation in goods has moderated, and the overall CPI for the Eurozone has cooled from 10% early this year to 5.5% in June.

But consumers spend the majority of their money on services, and the Eurozone CPI for services in June spiked to 5.4%. In services, inflation is hard to stamp out. This relentless inflation in services explains the continued rate hikes and the large-scale balance sheet reduction.

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the beer and iced-tea mug to find out how:

Would you like to be notified via email when WOLF STREET publishes a new article? Sign up here.

![]()

[ad_2]

Source link

Why the Fed is to blame for the boom in zombie companies

Lumber Price Gets Chopped in Half Amid Chill in Housing Markets