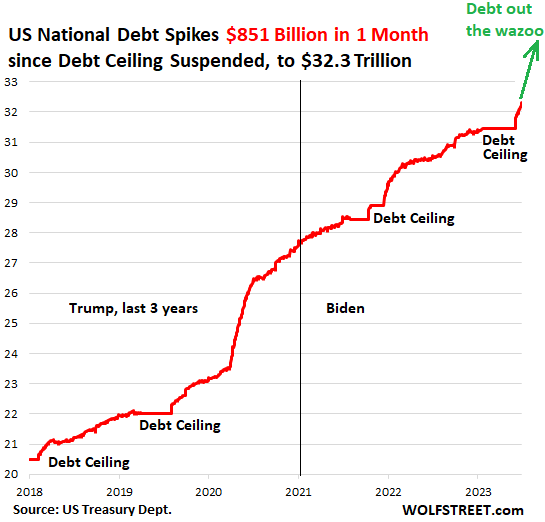

US National Debt Spiked by $851 billion in One Month, to $32.3 Trillion. Flood of New Debt Coming in Q3 to Refill the TGA, Pay for Raging Deficits

While, for the first time, the Fed’s QT and refilling the government’s checking account (TGA) pull liquidity from the markets simultaneously.

By Wolf Richter for WOLF STREET.

So this is a special day: The U.S. national debt spiked by $851 billion since the debt ceiling was suspended a month ago on June 3, and now hit $32.32 trillion, according the Treasury Department on Friday evening. This is just an amazing freakshow:

The US national debt is composed of two types of Treasury securities: “nonmarketable” Treasury securities that cannot be traded in the bond market; and marketable Treasury securities that the government sells via auctions to the public and that can be traded in the bond market.

“Nonmarketable” Treasury securities include the inflation-protected “I bonds” that Americans can buy directly from the Treasury Department. Government pension funds, the Social Security Trust Fund, etc. also invest in nonmarketable Treasury securities. The outstanding balance of nonmarketable Treasury securities rose by $123 billion since June 3, to $6.89 trillion.

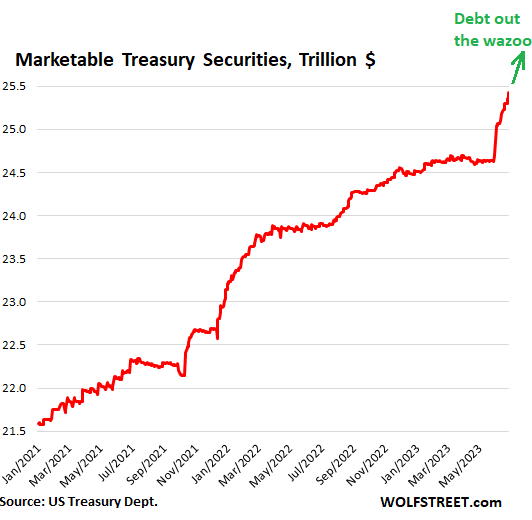

“Marketable” Treasury securities spiked by $728 billion since June 3, to $25.43 trillion.

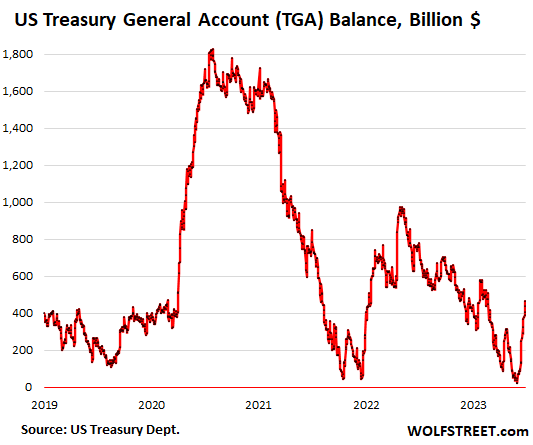

The Treasury Department has been selling vast amounts of Treasury bills and Cash Management bills (CMBs) since June 3, in addition to the long-scheduled issuance of Treasury notes (2 to 10-year maturities) and bonds (over 10 years), to refill its checking account. This “Treasury General Account” (TGA) at the New York Fed had been drawn down to just $23 billion by June 1, nearly nothing compared to the huge amounts that flow through that account on a daily basis.

The Treasury General Account has been partially refilled, from the low on June 1 of $23 billion to $465 billion on Friday, through a combination of this huge wave of new issuance of securities and the quarterly estimated tax payments that were due on June 15.

But wait a minute… For example, in 2022, the June 15 tax payments caused the TGA balance to jump by $140 billion. A month later, the balance was down by $200 billion. This year too, deficit spending will outstrip quarterly tax receipts by a wide margin.

In its Marketable Borrowing Estimates, released on May 1, the Treasury Department expected a TGA balance of $550 billion by the end of June. But Friday was the end of June, and the balance of the TGA was only $465 billion, thanks largely to lower tax receipts.

The Treasury estimated that the cash balance will increase in July, decline in August, and increase again in September (due to quarterly tax payments due on September 15), and by the end of September approach $600 billion, the level that is “consistent with Treasury’s cash balance policy.”

A wild ride of new issuance to get there… In the quarter starting July 1, so right now, the Treasury expected to borrow $733 billion in marketable securities to get to the $600 billion TGA balance by the end of September, assuming tax receipts don’t fall short again. That $733 billion flood of new issuance will start this week.

Draining liquidity.

Refilling the TGA pulls liquidity from the markets, in the opposite way that drawing down the TGA had added liquidity to the markets. Stocks had soared during the drawdown phases, and they had swooned during the first refill phase from late 2021 through April 2022, when the TGA absorbed nearly $1 trillion.

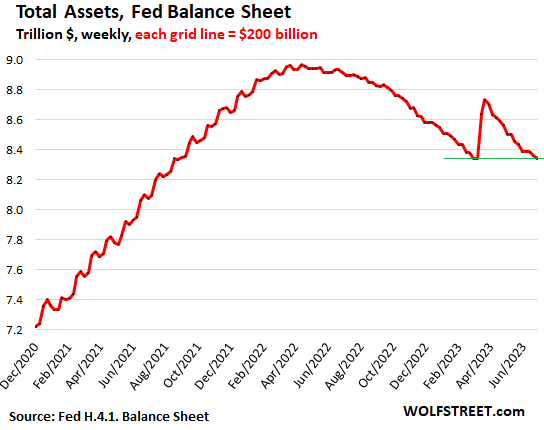

In addition, the Fed’s QT, which also pulls liquidity from the market, is running simultaneously with the refilling of the TGA for the first time, with both now pulling liquidity from the markets together. In terms of the Fed’s total assets, the brief bank-bailout spike has been worked off completely.

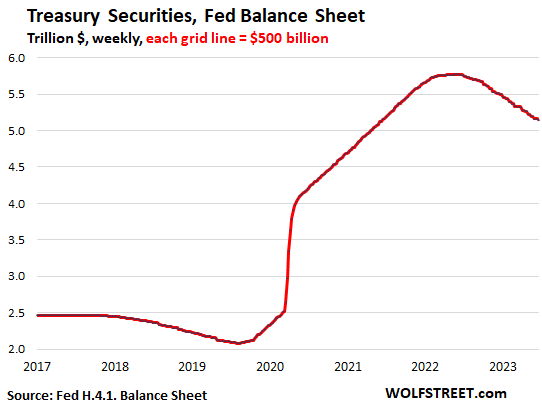

More relevant to the flood of issuance of Treasury securities by the government: The Fed has shed Treasury securities at a rate of about $65 billion a month; its holdings of Treasury securities are now down by $625 billion from the peak a year ago. And it will continue to shed $65 billion a month in Treasury securities:

Who’ll absorb this flood of new issuance plus the piles the Fed is leaving behind?

Don’t worry, it seems. So far, the Treasury market has been amazingly sanguine, amid juicy short-term yields that are beginning to price in a couple of additional rate hikes this year, and long-term yields that are, amid blistering demand, pricing in rate cuts and a return to 2% inflation ASAP.

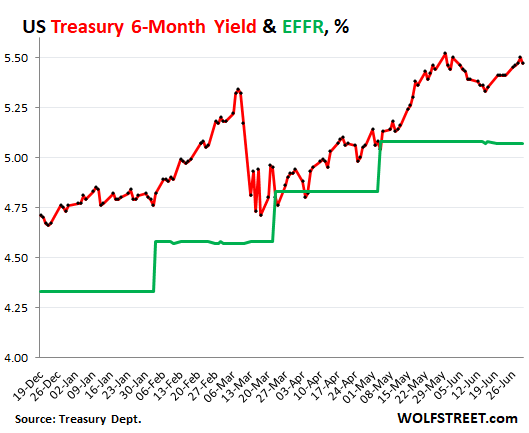

The six-month yield (red line) has bumped into 5.50% over the past three trading days, while the federal funds rate, which the Fed targets, has been at about 5.07% (green):

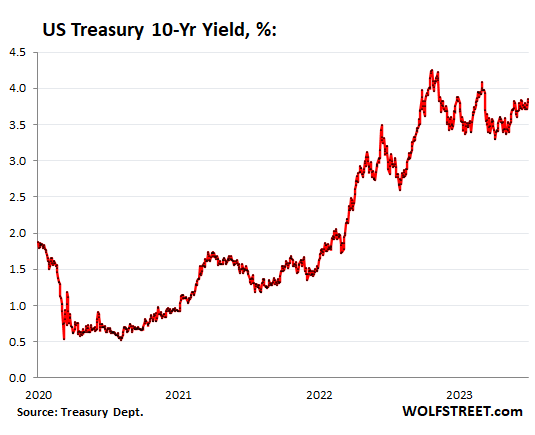

The 10-year yield, at 3.81% on Friday at the close, is pricing in rate cuts and a return to 2% inflation in no time. With similar omniscience back in August 2020, the 10-year yield had dropped as low as 0.5%, pricing in negative interest rates by the Fed, which was, turns out, a complete idiocy that caused some banks that believed it and loaded up on long-term securities to collapse. Since October, the 10-year yield has essentially gone nowhere.

Yield solves all demand problems. If demand sags at current yields, yields automatically rise until sufficient demand emerges. If the yield is high enough, there is always demand:

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the beer and iced-tea mug to find out how:

Would you like to be notified via email when WOLF STREET publishes a new article? Sign up here.

![]()

[ad_2]

Source link

The Treasury Begins Extraordinary Measures (again)

The next market trend could be ‘bigger’ than SVB, expert says