Third Wave of Hotel CRE Defaults Has Started, Triggered by CMBS Maturities and Variable-Rate Mortgages

CMBS holders are on the hook, not banks. Investors in hotel REITs have gotten totally crushed.

By Wolf Richter for WOLF STREET.

The financialization of everything has let to a convoluted setup for hotels and their beaten-up investors at all levels. It goes something like this: The hotel properties are held by a publicly traded hotel REIT that leveraged them up with variable-rate interest-only mortgages during the era of ultra-low interest rates, that were then securitized into commercial mortgage-backed securities (CMBS) and, backed by overinflated property valuations, sold to institutional investors, such as pension funds and bond funds. The hotels themselves are operated by other companies, usually partnering in some way with a hotel brand, such as Marriott.

When the Fed hiked its policy rates, the variable rates of those mortgages – pegged to short-term interest rates, such as Libor – jumped, and so mortgage payments roughly doubled in a year, while hotel property valuations plunged back to earth.

So the hotel REITs have now started to walk away from the properties. They take a total loss on their equity. The CMBS holders take the remaining losses when they sell the properties, with the proceeds not anywhere near enough to cover the loan balance. The companies that operate the hotels continue to do so, and guests might not know the difference.

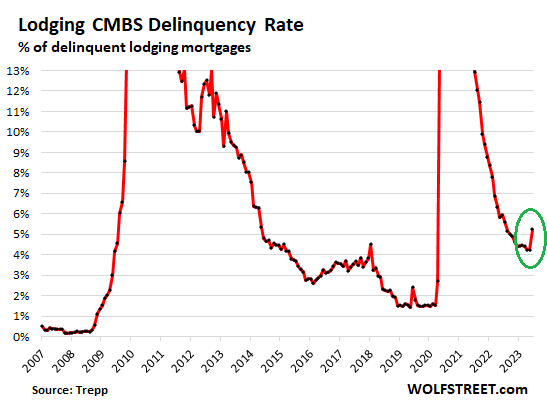

For CMBS holders, this has been a nasty deal for years. During the Great Recession, defaults topped out at 19%, according to Trepp, which tracks and analyzes CMBS. That was the first wave. During the early months of the pandemic, the default rate topped out at 24%; but in that second wave, as hotels reopened, many defaults were cured.

So now we have the beginning of a third wave of defaults in 15 years, this one driven by soaring interest rates, and property owners walking away instead of trying to work out a deal, as they’d often done during the pandemic.

In June, the default rate of lodging CMBS jumped to 5.3% – worse even than the default rate of office mortgages.

The latest was Ashford Hospitality Trust, a hotel REIT headquartered in Dallas. It said on Friday that it intends to walk away from 19 hotel properties in cities across the US.

The mortgages of the 19 hotels are in three mortgage pools that had an initial maturity date in June but could be extended. To extend the loans, the REIT would have to pay down the balance by $255 million.

Those three mortgage pools are part of six mortgage pools, with a combined balance of $982 million, that matured in June. The company decided to make the down-payments totaling $129 million on the other three pools to extend loans for the 15 hotels in those pools.

The interest rate of the three mortgage pools that it intends to walk away from has jumped to 8.8%, and the 19 hotels “were not covering debt service,” the company said.

By walking away, the company will save the $255 million down-payment plus it will save $80 million in capital expenditures at these hotels through 2025, it said.

It tried to sell two of these mortgage pools but did not receive any bids above the loan balances.

“This is a prudent economic decision that reflects a comprehensive capital management process by the Company, which explored and assessed multiple options for these assets including refinancing, extensions, and potential asset sales,” it said, thereby handing the losses to the CMBS holders.

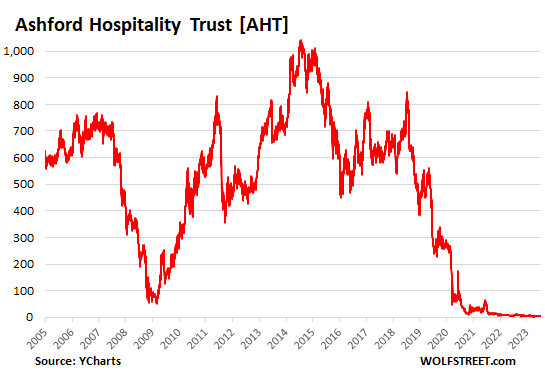

Ashford Trust’s shares [AHT] have completely imploded. To stay above $1, the shares have undergone two 1-for-10 reverse stocks splits, one in 2020 the next in 2021 (whereby 1,000 shares became 10 shares). Shares have collapsed by 99.6% from the reverse-splits-adjusted peak in 2014 of $1,040, to today’s share price of $4.03 (data via YCharts):

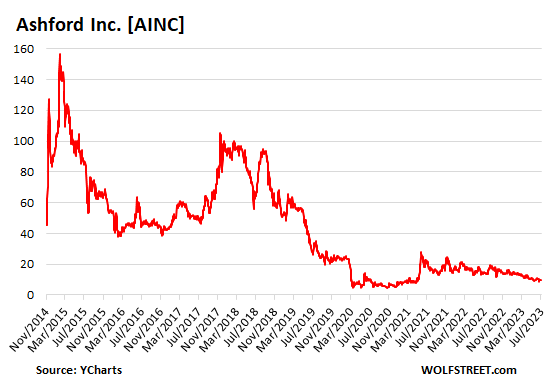

Ashford Trust is externally managed by Ashford Inc. [AINC], which was spun off from Ashford Trust in 2014, at the peak of Ashford Trust’s share price. Ashford Inc’s shares have collapsed by 94% from the peak after the spinoff, to $9.56 today. Both of these stocks are shining heroes in my pantheon of Imploded Stocks:

The 19 hotels that Ashford Trust is walking away from are in these cities:

- Columbus, IN (Courtyard)

- Scottsdale, AZ (Courtyard)

- Phoenix, AZ (Residence Inn)

- Flagstaff, AZ (Embassy Suites)

- Las Vegas, NV (Residence Inn)

- Plano, TX (Courtyard)

- Plano, TX (Residence Inn)

- Plymouth Meeting, PA (SpringHill Suites)

- Basking Ridge, NJ (Courtyard)

- Bridgewater, NJ (Marriott)

- Newark, CA (Residence Inn)

- Newark, CA (Courtyard)

- Hawthorne, CA (SpringHill Suites)

- Oakland, CA (Courtyard)

- Hawthorne, CA (TownePlace Suites)

- Walnut Creek, CA (Embassy Suites)

- Durham, NC (Marriott)

- Atlanta, GA (W)

- Baltimore Airport, MD (SpringHill Suites)

Another big hotel REIT walked away in June.

Hilton-spinoff Park Hotels and Resorts [PK], whose shares have collapsed by over 50% from their spinoff price and by 60% from the peak, made the headlines in June when it walked away from a variable-rate interest-only mortgage of $725 million, backed by two large hotels in San Francisco. With those two hotels gone, Park Hotel is down to 44 hotels properties, from 67 hotels at the time of its spinoff, having gotten rid of 23 properties.

Management of that REIT tried to pull a bag over their investors’ heads with a moronic clickbait line about San Francisco, instead of admitting that they’d grossly mismanaged the company, failed to invest in needed updates, and grossly overleveraged the properties. They should have apologized for having screwed investors in PK. A company that treats its investors that way gets downgraded from a “sell” to a “should have sold a long time ago.” And then, to top it off, they screwed the CMBS holders (such as pension funds and bond funds) by walking away from the properties. I lambasted them and the media coverage of their clickbait sleight-of-hand here.

However hotel-property owners may try to color their situation, what we are watching unfold is the revenge of variable-rate commercial debts in an overleveraged corporate world.

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the beer and iced-tea mug to find out how:

Would you like to be notified via email when WOLF STREET publishes a new article? Sign up here.

![]()

[ad_2]

Source link

Households Burn Through What’s Left of Their Pandemic Savings

Bruising Stock Reversal Shows How Fed’s Pivot May Come Too Late