The Fed’s Liabilities: QT Pushed Down Reserves & RRPs by $865 Billion. TGA Gets Refilled. Currency in Circulation Hits Record

The flow of cash under QT and government deficits.

By Wolf Richter for WOLF STREET.

Quantitative Tightening drew down two big liabilities on the Federal Reserve’s balance sheet: Reserves and RRPs dropped by a combined $865 billion from the peak.

At the same time, the other two big liabilities on the Fed’s balance sheet went into the opposite direction: the government’s checking account (TGA) and currency in circulation rose.

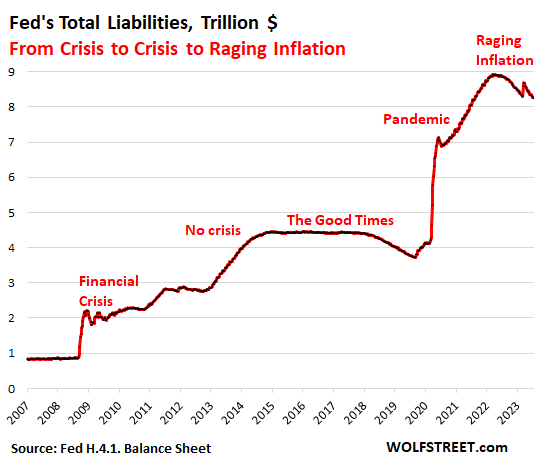

And so total liabilities dropped by $669 billion from the peak, to $8.25 trillion, according to the Fed’s weekly balance sheet released Thursday afternoon. We often discuss the Fed’s assets, such as Treasury securities, MBS, and banking panic loans. Today we’ll take a look at the Fed’s liabilities.

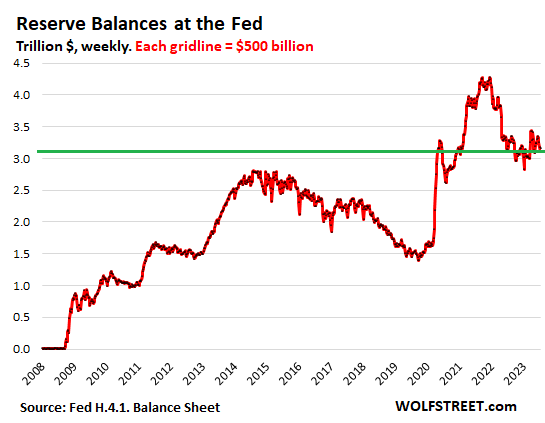

Reserves: $3.17 trillion, -$1.11 trillion since December 2021 peak.

Reserve are cash that banks put on deposit at the Fed; banks earn currently 5.15% in interest on reserves, as of the May Fed meeting.

Reserves are a manifestation of liquidity in the banking system that is not chasing after other assets. QT is draining liquidity from the financial system, and the first place the drainage showed up was in reserves.

In late 2021, when the Fed began “tapering” its QE asset purchases, reserves peaked and then began to fall. QE ended altogether in March 2022. QT started in July 2022. You can see the sharp drop in reserves through March 2023, and then upticks following the banking panic.

Reserves are the most liquid, risk-free interest-paying asset banks can invest in. “Reserves” is Fed lingo. On bank balance sheets, they’re assets called “interest-earning deposits,” “interest-earning cash” or similar.

Banks use their reserve accounts at the Fed to transfer money between banks and to do business with the Fed. Reserves are a liability on the Fed’s balance sheet since the Fed borrowed this cash from the banks.

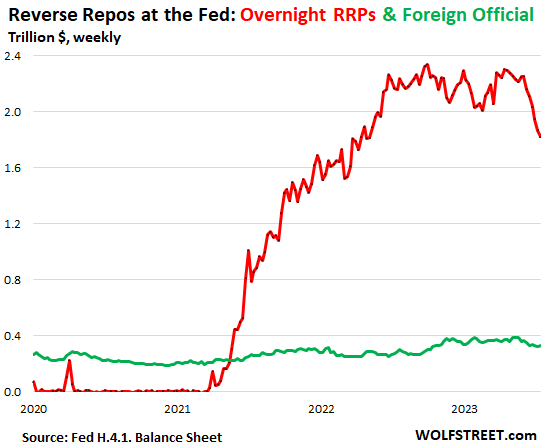

Reverse Repurchase agreements (RRPs), All: $2.15 trillion; -$490 billion from Sep 2022 peak.

The Fed offers reverse repurchase agreements (RRPs) to two groups:

- “Foreign official” accounts, where other central banks can park their dollar cash;

- Overnight RRPs where US Money Market funds, banks, and government-sponsored enterprises (Federal Home Loan Banks, Fannie Mae, Freddie Mac, etc.) can park their extra cash.

The counterparties earn 5.05% in interest risk-free on Overnight RRPs. So that’s a good deal, but not as good as reserves (5.15%). And not as good as Treasury bills (up to 5.5%); but RRPs are more liquid (overnight) than Treasury bills, which have to be sold for liquidity.

So banks park some of their cash in their reserve accounts to earn (5.15%). But money market funds don’t have access to reserve accounts, and so they park the portion of their cash that they want to keep liquid in RRPs to earn 5.05%

Under these RRPs, the Fed takes in cash and hands out collateral (Treasury securities). RRPs are a liability for the Fed because they’re cash that the Fed owes its counterparties.

Foreign official RRPs: $328 billion, -$56 billion from January 2023 peak (green line in the chart below).

Overnight RRPs: $1.82 trillion, -$547 billion from Sep 2022 peak (red line).

The Treasury Department is now issuing a flood of Treasury securities at higher yields than RRPs or reserves. And for some time, money market funds have switched some of their cash that they need for liquidity reasons to RRPs, from their bank accounts since banks are so stingy with the interest they pay.

In addition, bank depositors yanked their deposits out of banks and invested them in money market funds. So banks reduced their reserves, and money market funds increased their RRPs.

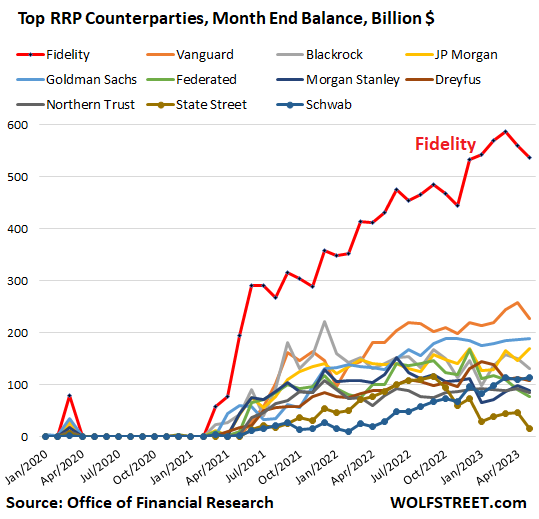

The government’s Office of Financial Research publishes RRP balances by money-market funds on a monthly basis with a one-month delay. The most recent release was for May. At the time, about 25% of RPPs were with Fidelity ($536 billion):

So there was a flow of cash from reserves to RRPs via money market funds, and they should be look at together…

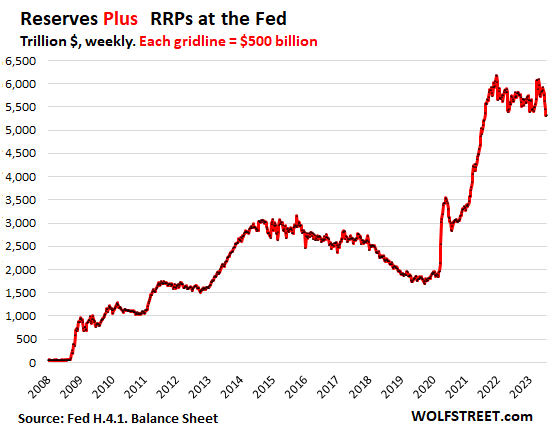

Reserves plus RRPs: $5.31 trillion; -$865 billion from Dec 2021 peak.

The pandemic-era QE had inflated the combined total of Reserves plus RRPs by $4.2 trillion, to $6.18 trillion at the peak in December 2021. Roughly 21% of that surge has now been worked off.

The Fed has shed $664 billion in Treasury securities and $202 billion in MBS, for a combined QT total of $868 billion. At the same time, the combined “Reserves plus RRPs” have dropped by $865 billion. QT in action.

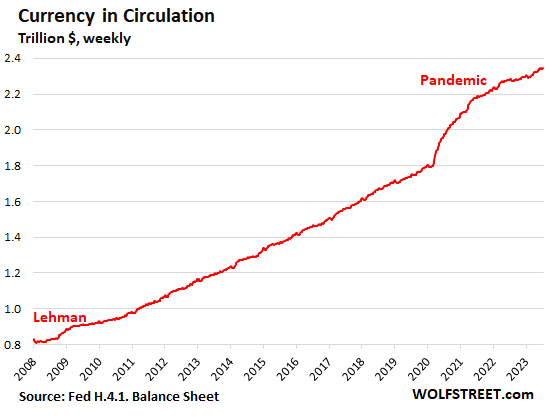

Currency in circulation: $2.34 trillion; new record.

Currency in circulation reflects the paper dollars in wallets, under mattresses, and in safes in the US and globally. It is demand-based through the US banking system. If customers demand paper dollars, the banking system must have enough on hand. Foreign banks have relationships with US banks to get dollars for their customers.

These “Federal Reserve Notes,” as they’re called officially, are a liability for the Fed (“notes”). Banks get those paper dollars from the Fed in exchange for collateral, such as Treasury securities, which are assets on the Fed’s balance sheet.

Before QE, currency in circulation was the primary driver of the increase in assets on the Fed’s balance sheet through the collateral (Treasury securities, etc.) that banks have to post to get these paper dollars.

Currency has been phasing out as payment methods for legitimate purchases as electronic payment systems have taken over. But demand for currency has been huge. A big part of it is stashed around the world for legal and illegal purposes, and part of it is spread across US households.

When there is fear of a crisis, demand for paper dollars surges: It spiked before Y2K, after the Lehman bankruptcy, and massively starting in early 2020.

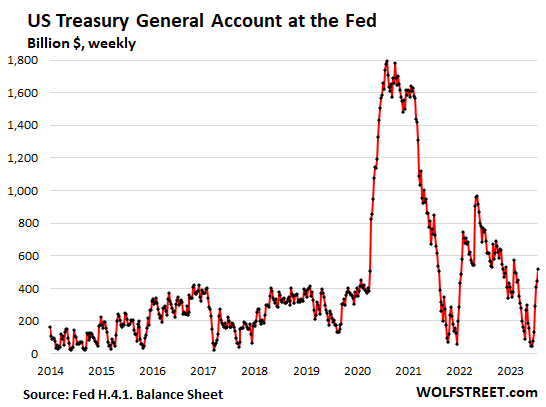

Treasury General Account (TGA): $517 billion.

The Treasury Department has been issuing a flood of Treasury bills and Cash Management bills plus the scheduled notes and bonds since the Debt Ceiling was suspended at the beginning of June to refill its checking account at the New York Fed – the TGA.

The amount in the TGA is money the Fed owes the government and is a liability for the Fed.

June 15 was the due date for estimated taxes; it brought in a pile of tax receipts, which fell short, but boosted the TGA nevertheless for a little while. But deficit spending that must be funded is a huge daily drain on the account.

For the current quarter, the Treasury expects to borrow $733 billion to pay its bills and get the TGA balance to $600 billion by the end of September. We discussed the national debt, deficits, the flood of new issuance even while QT is happening, and the TGA in greater detail here.

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the beer and iced-tea mug to find out how:

Would you like to be notified via email when WOLF STREET publishes a new article? Sign up here.

![]()

[ad_2]

Source link

Robert Kiyosaki Says World Economy on the Verge of Collapse — Warns of Bank Runs, Frozen Savings, Bail-Ins – Economics Bitcoin News

Morgan Stanley Predicts Future of the U.S. Dollar