The Acceleration of Inflation in the Second Half Has Begun, “Disinflation” Honeymoon Terminated

Month-to-month CPI spikes, core CPI and core services CPI accelerate, despite ongoing massive health insurance adjustment.

By Wolf Richter for WOLF STREET.

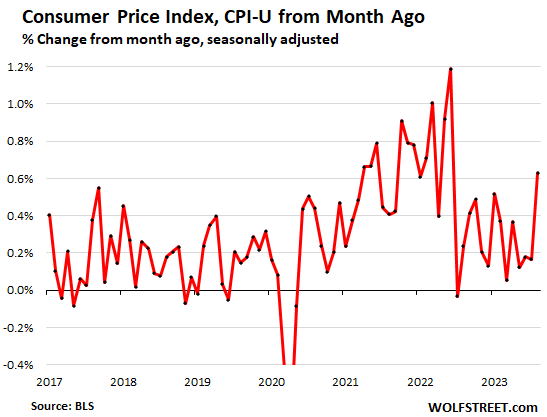

The Consumer Price Index (CPI) jumped by 0.63% in August from July, the biggest month-to-month increase since June 2022. Annualized, this amounts to a red-hot 7.8%.

This jump comes despite the still ongoing ridiculous monthly adjustment to the health insurance CPI that caused it to collapse by 33.6% year-over-year. The September CPI, to be released in October, will be the last month with that adjustment; with the October CPI, to be released in November, it will flip, which will add upward momentum to the CPI readings. CPI, core CPI, and core services CPI have been understated significantly since October last year, when the monthly health insurance adjustment started, one of the biggest data distortions coming out of the pandemic (more in a moment).

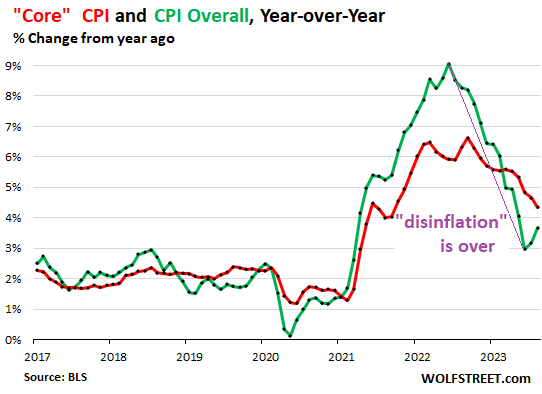

With this month-to-month spike, the year-over-year CPI rate accelerated to 3.7%, the second year-over-year acceleration since June 2022, according to the Bureau of Labor Statistics today (green in the chart below). July had already marked the end of the period of “disinflation” when the year-over-year inflation rate accelerated for the first time since June 2022.

The “Core” CPI, which attempts to track underlying inflation by excluding the volatile food and energy products, rose by a still hot 4.3% in August, compared to a year ago (red in the chart).

Given the narrower focus of core CPI, and the therefore proportionally bigger weight of health insurance in it, core CPI was even more distorted than overall CPI by the 33.6% collapse of the health insurance CPI.

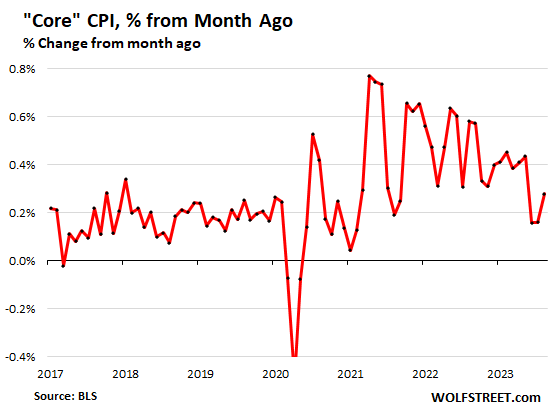

Core CPI, month-to-month, was held down by the collapse of the health insurance CPI, and yet, it still accelerated to 0.28% in August from July.

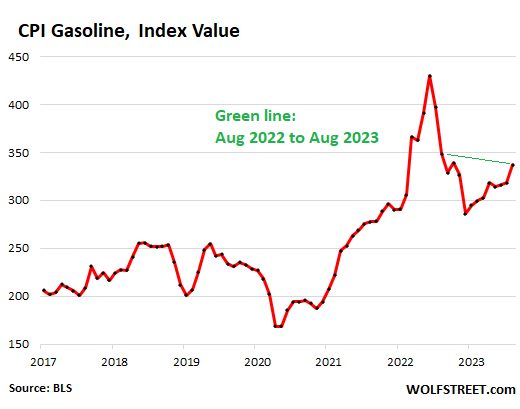

Fuel prices will push CPI up further, even core CPI.

Starting with April, the year-over-year plunge in energy prices at the time, particularly gasoline, pushed the overall CPI increases below those of core CPI.

But on a month-to-month basis, gasoline prices have been surging all year – they jumped 10.6% in August from July – thereby whittling away at the year-over-year plunge as we went. In August, gasoline CPI was still down by 3.3% from August 2022.

Given how the gasoline CPI plunged in late 2022, we know that on a year-over-year basis, gasoline CPI will turn sharply positive later this year. The green line in the chart connects August 2023 and August 2022:

Gasoline accounts for about half of the total energy CPI. Note that gasoline, and energy overall, are still negative year-over-year, despite the sharp month-to-month increases. They will flip to positive, and become bigger drivers of CPI inflation over the coming months:

| CPI for Energy, by Category | MoM | YoY |

| Overall Energy CPI | 5.6% | -3.6% |

| Gasoline | 10.6% | -3.3% |

| Utility natural gas to home | 0.1% | -16.5% |

| Electricity service | 0.2% | 2.1% |

| Heating oil, propane, kerosene, firewood | -12.4% | 8.4% |

How fuel prices filter into “core” CPI.

Diesel has also been surging this year on a month-to-month basis. The price of diesel over time filters into the prices of consumer products that are shipped by truck and rail, as are nearly all consumer products. Jet fuel has been surging similarly, and that filters into products that are shipped by air, and into services via air fares. These products and services are reflected in core CPI, which is how core CPI reacts indirectly to rising energy costs.

The tougher second half has started.

We’ve been warning here about this for months while the media was touting the story that inflation was “vanquished” or whatever. We knew CPI would worsen dramatically in the second half for at least three reasons:

- Energy prices won’t plunge forever, and in fact gasoline prices began surging again.

- The “base effect,” which pushed down year-over-year CPI in the first half, is finished.

- The ridiculous “health insurance adjustment” that started with October 2022, will swing the other way, starting with the October CPI, to be released in November. More in a moment.

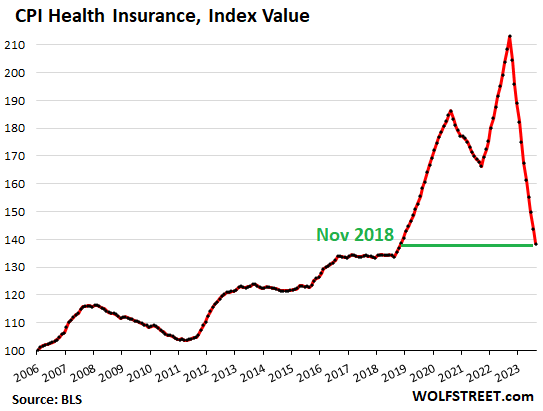

The collapse of the health insurance CPI.

The monthly adjustments to the health insurance CPI, which started with the October CPI last year, will swing the other way with the October CPI this year, to be released in November (I discussed the details a month ago here).

The adjustment pushed down the health insurance CPI every month on a month-to-month basis by 3.4%-4.3%, which has now caused the year-to-year health insurance CPI to collapse by 33.6%, despite maddening price increases of health insurance in the real world. I’ve called these monthly adjustments “odious” and “ridiculous” because that’s what they are. They’re one of the worst data distortions that came out of the pandemic.

A 4% month-to-month plunge, as opposed to a 1% month-to-month rise, as would be the case, represents a month-to-month swing of 5 percentage points!

The 33.6% year-over-year collapse, as opposed to something like a 12% increase, as would be the case, represents a swing of 45.6%.

The deeper we go into CPI and the narrower the metric – overall CPI, core CPI, services CPI, core services CPI – the worse this adjustment distorts the figures.

The health insurance CPI as a price index itself (not percent change) in August collapsed to the price level of November 2018, despite massive health insurance increases since then. This is why I have been so furious about this metric from day one: it renders core CPI and even more core services CPI essentially useless as an indicator of where underlying inflation is going. This is just effing nuts:

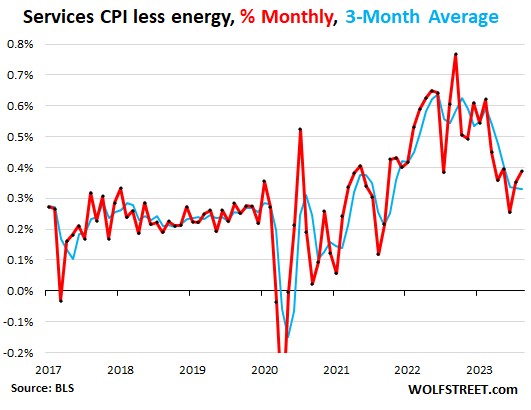

Core Services CPI accelerated, despite collapse of health insurance CPI.

The index for core services (without energy services) accelerated to 0.39% in August from July, the second month in a row of acceleration, despite the adjustment to the CPI for health insurance of -3.6% in August from July.

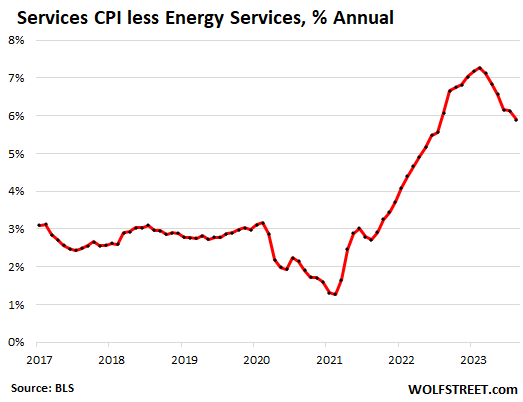

Year-over-year, the core services CPI rose by a still red-hot 5.9%, despite the 33.6% collapse of the health insurance CPI within it.

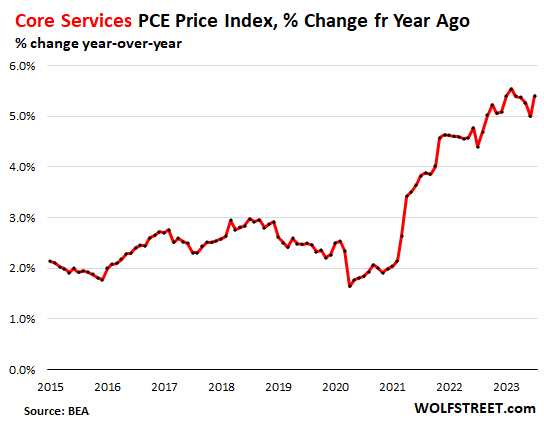

What happens when the health insurance adjustment flips?

Our other major inflation index, the PCE price index, which the Fed favors, uses different methods to track health insurance. It has its own flaws, but it is not distorted by this ridiculous health insurance adjustment. In the most recent release, the core services PCE price index spiked to the second worst level since 1985, an indication of what awaits core services CPI after the health insurance adjustment flips:

Services CPI by category.

You can see in the table how hot many price increases are. The table is sorted by weight of each service category in the overall CPI. The CPI for medical services is the third largest item, with a weight of 6.4% in overall CPI. Its weight in the services CPI is over 10%, and it has been repressed by the collapse of the health insurance CPI within it, and turned negative year-over-year.

| Major Services without Energy | Weight in CPI | MoM | YoY |

| Services without Energy | 62.4% | 0.4% | 5.9% |

| Owner’s equivalent of rent | 25.6% | 0.4% | 7.3% |

| Rent of primary residence | 7.6% | 0.5% | 7.8% |

| Medical care services & insurance | 6.4% | 0.1% | -2.1% |

| Education and communication services | 4.9% | 0.1% | 2.6% |

| Food services (food away from home) | 4.8% | 0.3% | 6.5% |

| Recreation services, admission, movies, concerts, sports events | 3.1% | -0.1% | 6.1% |

| Motor vehicle insurance | 2.6% | 2.4% | 19.1% |

| Other personal services (dry-cleaning, haircuts, legal services…) | 1.4% | 0.7% | 6.4% |

| Motor vehicle maintenance & repair | 1.1% | 1.1% | 12.0% |

| Hotels, motels, etc. | 1.1% | -3.6% | 3.0% |

| Water, sewer, trash collection services | 1.1% | 0.5% | 5.8% |

| Video and audio services, cable | 1.0% | 0.6% | 5.9% |

| Airline fares | 0.6% | 4.9% | -13.3% |

| Pet services, including veterinary | 0.6% | -0.6% | 8.5% |

| Tenants’ & Household insurance | 0.4% | 0.3% | 1.5% |

| Car and truck rental | 0.1% | 1.3% | -6.8% |

| Postage & delivery services | 0.1% | 0.0% | 4.7% |

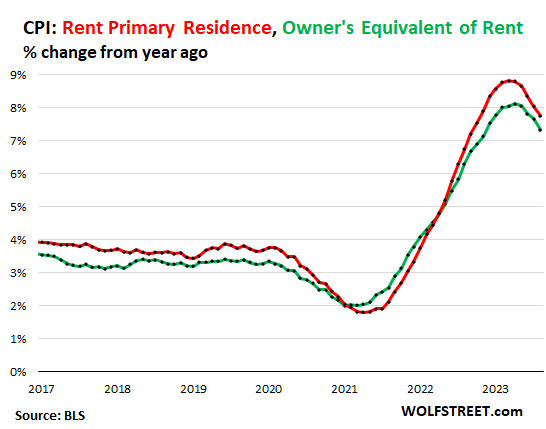

The two CPIs for housing as a service (“shelter”).

“Rent of primary residence” re-accelerated to +0.48% for August. Year-over-year, +7.8% (red in the chart below). The August rate of 0.48% amounts to an annualized growth rate of 5.9%.

The survey follows the same large group of rental houses and apartments over time and tracks what tenants, who come and go, are actually paying in these units.

Owners’ equivalent rent: +0.38% for August, +7.3% year-over-year (green). This is based on what a large group of homeowners estimates their home would rent for.

The chart shows the year-over-year percentage change of both:

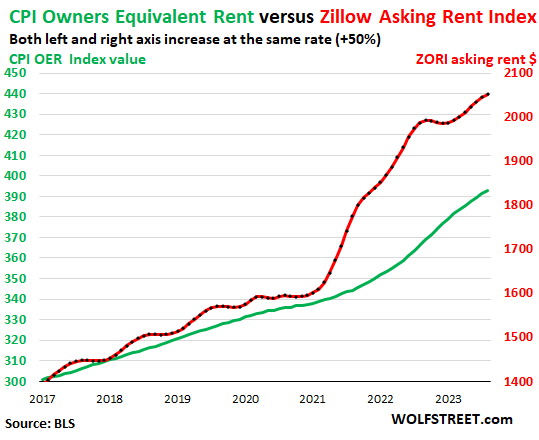

“Asking rents…” The Zillow Observed Rent Index (ZORI) and other private-sector rent indices track “asking rents,” which are advertised rents of vacant units on the market. The ZORI’s spike in 2021 through mid-2022 never fully made it into the CPI indices because rentals don’t turn over that much, and not many people actually ended up paying those spiking asking rents.

In late 2022, asking rents in dollar-terms began to dip, but quickly began to rise again this year, and started hitting new records in dollar-terms months ago. On a month-to-month basis, asking rents have been rising in a range of 0.33% to 0.62% (annualized 4.0% to 7.7%) over the past six months with some seasonality in it. So asking rents continue to increase at a fairly sharp clip, but not as fast as in 2021 and early 2022.

The chart shows the OER (green, left scale) as index values, not percent change; and the ZORI (red, right scale). The left and right axes are set so that they increase each by 50%, with the ZORI up by 47.3% since the beginning of 2017 and the OER up by 30.5%:

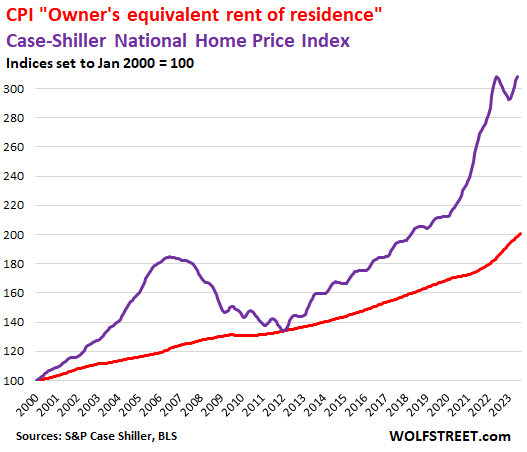

Rent inflation vs. home-price inflation: The red line represents the OER. The purple line represents the Case-Shiller Home Price Index. Both lines are index values set to 100 for January 2000:

Durable goods prices stabilize at nosebleed levels.

The CPI for durable goods, after blasting into the astronomical zone, has been slowly meandering lower, but remains in the astronomical zone.

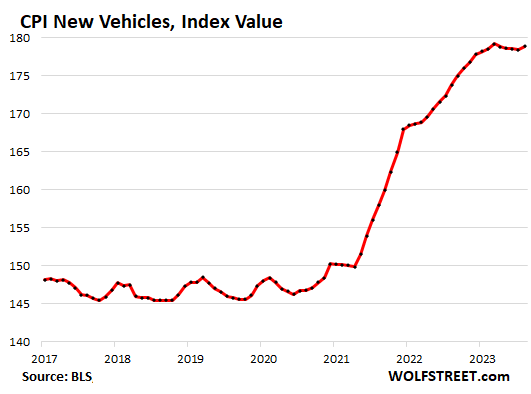

New vehicles CPI, after easing just a bit, rose again in August from July, and the price index is now just a hair away from setting a new high. Year-over-year, it’s up by 2.9%.

Thankfully, there are now changes underway. Tesla is massively cutting prices, while gaining market share at a blinding speed (it’s already #2 in California, and at this pace will surpass Toyota as #1 in 2024). And so now Tesla’s price cuts, followed by some other automakers, are whacking the industry’s oligopolistic pricing behavior.

For many years before the pandemic, the new vehicle CPI was essentially flat with some ups and downs, despite large increases of actual vehicle prices. This is the effect of “hedonic quality adjustments” to the CPIs for new and used vehicles, consumer electronics, and other products (here’s my infamous chart and detailed explanation of hedonic quality adjustments).

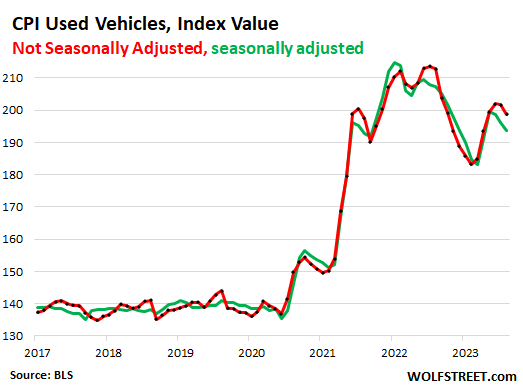

Used vehicle CPI has gone through some major gyrations after the historic 53% spike in used vehicle prices that started in 2020 and peaked at the end of 2021. In August, the used vehicle CPI fell by 1.2% seasonally adjusted from July and was down by 6.6% from a year ago. From the peak, it has now fallen by 10%.

The chart shows the seasonally adjusted (green) and not seasonally adjusted (red) index values. The past three years were wild pricing turmoil. You can also see the effects of the hedonic quality adjustments in the years before the pandemic.

| Durable goods by category | MoM | YoY |

| Durable goods overall | -0.3% | -2.0% |

| New vehicles | 0.3% | 2.9% |

| Used vehicles | -1.2% | -6.6% |

| Information technology (computers, smartphones, etc.) | -0.8% | -8.7% |

| Sporting goods (bicycles, equipment, etc.) | 0.2% | -1.2% |

| Household furnishings (furniture, appliances, floor coverings, tools) | 0.3% | 1.7% |

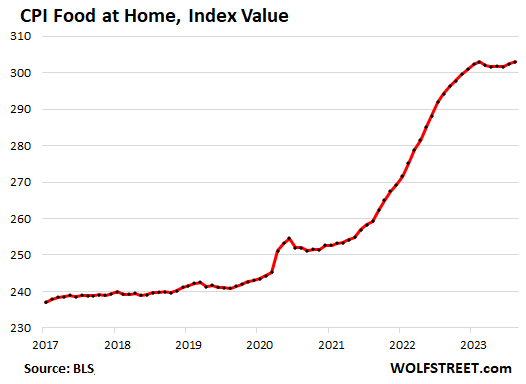

Food at home.

Food prices at grocery stores and markets have calmed down at astronomical levels, following the 24% spike during the pandemic. Instead of plunging to bring them back into line, food prices dipped just a little for a few months and now started rising again at roughly the pace before the pandemic, but on top of these nosebleed levels!

The CPI for “food at home” rose by 0.2% in August from July. The 3.0% year-over-year increase was the smallest in two years.

| Food at home by category | MoM | YoY |

| Overall Food at home | 0.2% | 3.0% |

| Cereals and cereal products | -0.3% | 4.3% |

| Beef and veal | 1.2% | 6.3% |

| Pork | 2.2% | -1.9% |

| Poultry | 1.0% | -0.1% |

| Fish and seafood | 0.1% | -0.8% |

| Eggs | -2.5% | -18.2% |

| Dairy and related products | -0.4% | 0.3% |

| Fresh fruits | -0.3% | 0.6% |

| Fresh vegetables | -0.1% | 1.0% |

| Juices and nonalcoholic drinks | 0.3% | 5.8% |

| Coffee | -0.7% | 0.9% |

| Fats and oils | 0.2% | 4.7% |

| Baby food & formula | 0.4% | 8.4% |

| Alcoholic beverages at home | 0.1% | 2.4% |

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the beer and iced-tea mug to find out how:

Would you like to be notified via email when WOLF STREET publishes a new article? Sign up here.

![]()

[ad_2]

Source link

U.S. goods trade deficit hits record high; Q1 GDP growth estimates slashed