Social Security Update: Trust Fund, Income, Outgo, and Deficit in Fiscal 2023

Contributions jumped 11.8% (more people working, big pay increases). Outgo jumped 12.0% (more people at retirement age and the 8.7% COLA).

By Wolf Richter for WOLF STREET.

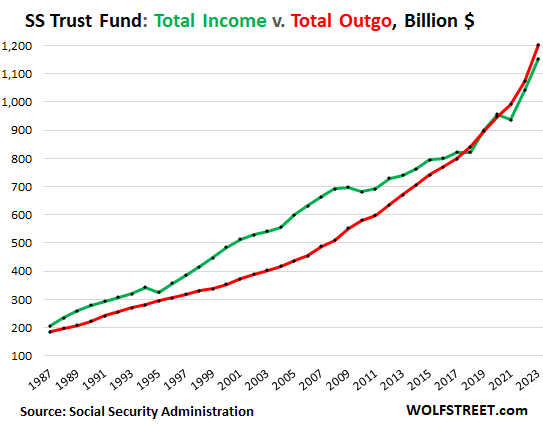

Total income from all sources jumped by $111 billion from the prior year, or by 10.7%, to a record $1.15 trillion in the US government fiscal year ended September 30, according to the Social Security Administration (SSA) today (green line in the chart below). By category of income:

- Contributions jumped by $110 billion, or by 11.8%, to $1.04 trillion due to employment growth and big pay increases in 2022 and 2023.

- Interest income from the securities in the Trust Fund dipped by $2 billion to $63 billion.

- Taxation of benefits rose by $3 billion to $50 billion.

Total outgo rose by $129 billion, or by 12.0%, to a record $1.20 trillion (red line), on the 8.7% Cost of Living Adjustment, the biggest since 1981, and more people at retirement age and drawing Social Security benefits. Benefits paid accounted for 99.2% of the outgo; the remaining 0.8% were made up of transfers to Railroad Retirement programs ($5.6 billion) and administrative costs ($4.3 billion).

When the green line (total income) was above the red line (total outgo), the Trust Fund accumulated assets. When the green line fell below the red line, the Trust Fund shrank.

The gap between income and outgo was $50 billion, up from a deficit of $32 billion in 2022, but down from the $55 billion deficit in 2021, after surpluses in 2020 and 2019.

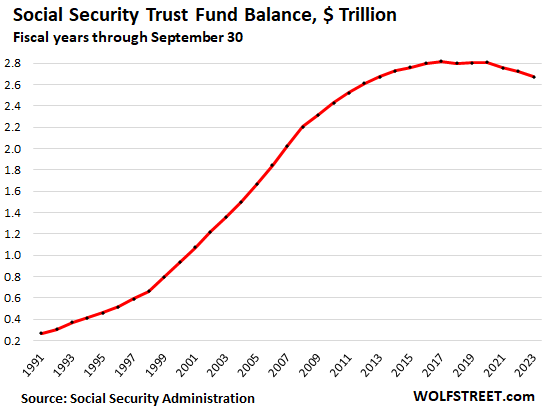

The first deficit in the data going back to 1987 occurred in 2018 ($19 billion). Until then, the annual surpluses had produced the $2.8 trillion in the Trust Fund at the time.

The low 3.2% COLA for next year will slow the growth of the outgo. With the release of the CPI data two weeks ago, the CPI-W was also released. It’s the measure that the COLA calculations are based on, and they were pretty thin: In 2024, the COLA of 3.2% will be bad for retirees, but it will slow the deficit, or may even produce a surplus if employment and pay continue to grow at the current pace.

The Social Security Trust Fund.

Technically known as “Old-Age and Survivors Insurance (OASI) Trust Fund,” it declined by $50 billion, or by 1.8%, during the fiscal year, to $2.67 trillion, according to SSA data.

These figures to not include the Disability Insurance Trust Fund, which by law is a separate entity from the OASI Trust Fund, and is not part of this discussion here.

How the Trust Fund invests the $2.67 trillion.

The OASI Trust Fund invests in interest-bearing Treasury securities and short-term cash management securities. These securities are not traded in the secondary market, similar to the popular I-bonds that many people, including a number of WOLF STREET commenters here, are holding at TreasuryDirect.

It’s a good thing that the securities in the Trust Fund are not subject to the whims and occasional chaos of the secondary market: The value of these holdings – similar to the value of our accounts at TreasuryDirect – doesn’t fluctuate with the prices in the secondary market. The Trust Fund holds Treasury securities until they mature and then gets paid face value for them. Day-to-day price fluctuations are irrelevant for the Trust Fund.

At the end of the fiscal year, the Trust Fund held $2.47 trillion in interest-bearing special-issue Treasury securities and $202 billion in short-term cash-management securities (“certificates of indebtedness”).

Investing in Treasury securities when they’re issued and holding them until they mature is a low-risk conservative strategy that essentially eliminates credit risk.

This strategy allows the SSA to operate the system with ultra-low administrative expenses, amounting to just 0.16% of the assets under management.

The Fed’s interest rate repression created the deficit.

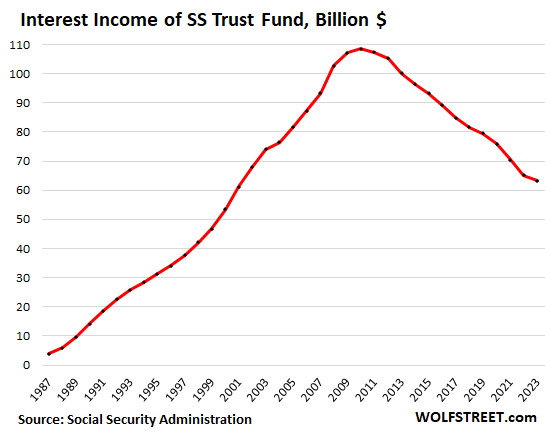

The Trust Fund earned $63 billion in interest on its Treasury holdings in the fiscal year, down by 42% from the peak in 2010, the year of peak interest, though the Trust Fund balance was smaller in 2010 than today.

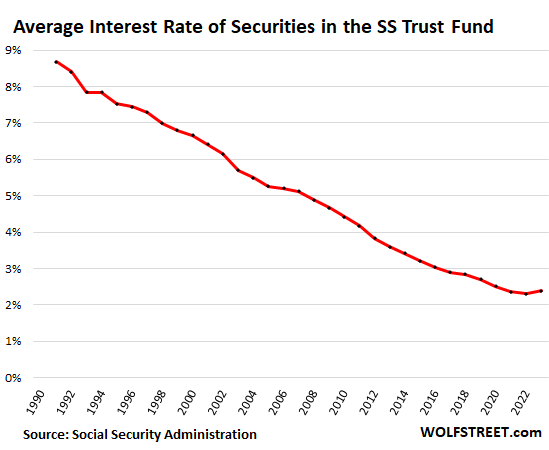

The average weighted interest rate that the Trust Fund earned ticked up to 2.4% this fiscal year, from 2.3% last year, as higher yielding securities began replacing some lower yielding securities in the Fund – but it’s still just a minuscule improvement.

As a result of the Fed’s interest rate repression starting in 2007, the interest rate that the Trust Fund earned was cut by more than half, from 5.1% in 2007, to 2.4% this year.

Because the Fund invests in long-term securities and because interest rates of securities don’t change until the securities mature and are replaced with new securities, there is a lag before changes in long-term yields filter into the “average interest rate” and into the interest-income stream.

The average number of years to maturity used to be around 7 to 7.5 years. But in 2020 it began to drop, and in the fiscal year through September, it declined to 5.67 years, the shortest on record. In other words, the current crop of higher-yielding securities is going to make their way into the Fund a little more quickly.

Today’s interest rates would eliminate the deficit.

If the Trust Fund had earned an average 5% on its balance of $2.67 trillion this year, it would have earned $133 billion in interest income, instead of $63 billion, and the Fund would have had a surplus of $20 billion!

Obviously, what the Trust Fund experienced – that the Fed wrecked its cash flow via interest rate repression between 2007 and 2022 – is precisely what all yield investors, including retirees, experienced on their fixed-income investments.

If longer-term Treasury yields normalize in the 4% to 8% range, as was the case between 1990 and 2007 (they were even higher in the prior 20 years), the Fund’s income and outgo would be back in balance. But it would take a few years before the low-yielding securities would be replaced by higher yielding securities.

Relatively small adjustments would eliminate the deficit.

The current gap is not large – $50 billion this year, or 4% of total income, despite the huge 8.7% COLA. The Trust Fund still has $2.67 trillion in accumulated surplus. At an annual deficit of $50 billion, it’s going to take many years before the fund runs out of money. You can do the math. At that out-of-money point, if no other adjustments are made, benefits would need to be cut by some percentage to match income.

The deficit will likely be smaller next year, based on the 3.2% COLA. And other than higher interest rates, a combination of relatively small adjustments to the plan would bring it back into balance for decades to come.

Several proposals have been floated in Congress over the years. And forbidding the Fed to engage in QE (repression of long-term interest rates) should be part of the solution, and would do some heavy lifting.

It’ll be there, but it won’t be enough.

Social Security was never intended to be the sole source of income in retirement. It was designed as a base layer of income to keep people out of abject poverty or worse when they can no longer work. Social Security will be there when people retire, the spousal benefits will be there, and the survivor benefits will be there. But they won’t be enough.

And the COLAs over the years will not be enough either to fully make up for the loss of the purchasing power of the retiree’s dollar.

Social Security was designed to be supplemented by other sources of income, such as from assets or savings that people put aside during their working lives.

In addition, working for as long as possible, even part-time, is hugely beneficial in all aspects. Our politicians have figured that out too. They’re working well past their full Social Security retirement age – some of them decades past their full retirement age – and they’re obviously having a blast doing it.

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the beer and iced-tea mug to find out how:

Would you like to be notified via email when WOLF STREET publishes a new article? Sign up here.

![]()

[ad_2]

Source link

China calls reports on Chinese-Russian coordination on Ukraine ‘fake news’

Don’t Blame ‘Greedy Corporations’ for Inflation. Blame the Government.