“Unrealized Losses” on Securities Held by Banks Jump by 22% to $684 Billion in Q3, Oh Lordy

They don’t matter, until they suddenly do.

By Wolf Richter for WOLF STREET.

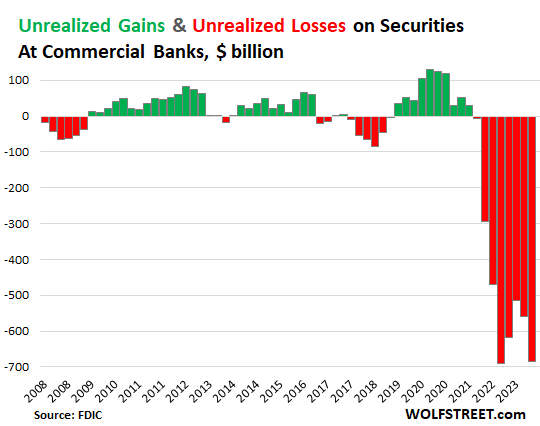

“Unrealized losses” on securities – mostly Treasury securities and government-guaranteed MBS – at FDIC-insured commercial banks at the end of Q3 jumped by $126 billion (or by 22%) from the prior quarter, to $684 billion, according to the FDIC’s quarterly bank data release on Wednesday.

These unrealized losses were spread over the two accounting methods:

- Unrealized losses on held-to-maturity (HTM) securities jumped by $81 billion from the prior quarter, to $391 billion.

- Unrealized losses on available-for-sale (AFS) securities jumped by $45 billion from the prior quarter to $293 billion.

These paper losses occur predictably when interest rates rise. As yields rose in Q3, the market prices of those bonds fell, and the unrealized losses stacked up. For example, the 10-year Treasury yield jumped from 3.81% at the beginning of Q3 to 4.59% at the end of Q3. In periods when yields fell and bond prices rose, banks had “unrealized gains” (green).

“Unrealized losses” on securities held by banks don’t matter because at maturity in 7 or 10 or 25 years, banks will be paid face value, and the losses are only temporary, so to speak. They don’t matter until they suddenly do.

Banks, via a quirk in bank regulations, don’t have to mark these securities to market value, but can carry them at purchase price. The difference between market value and purchase price is the “unrealized gain or loss” that the bank must disclose in its quarterly financial filings, so that we the depositors can see them and get spooked by them and yank our money out, us billionaires and centimillionaires first, on the two fundamental principles of investing: 1, he who panics first, panics best; and 2, after us the deluge.

And thanks to today’s electronic fund transfers, the bank that we yank our money out collapses at lightning speed, see Silicon Valley Bank, Signature Bank, and First Republic.

The accumulated unrealized losses of $684 billion were not a record, but were still $6 billion lower than the record in Q3 2022, because the FDIC took over the three regional banks earlier this year, and sold their assets, including their securities, at something close to market value, and thereby ate those paper losses.

For example, SVB, in its 10-K filing with the SEC for 2022, in a footnote on page 125, disclosed unrealized losses of $15.2 billion on HTM securities and $2.5 billion on AFS securities, for a total of $17.7 billion. These losses vanished from the banking system when the FDIC took over SVB.

The three collapsed banks’ unrealized losses were taken out of the banking system in Q1 and Q2, which is why Q3 2023 wasn’t a huge all-time record.

Those losses v. regulatory capital. The $391 billion in HTM “unrealized losses” amount to:

- 17.5% of total bank equity capital ($2.24 trillion)

- 18.0% of Tier 1 capital ($2.14 trillion)

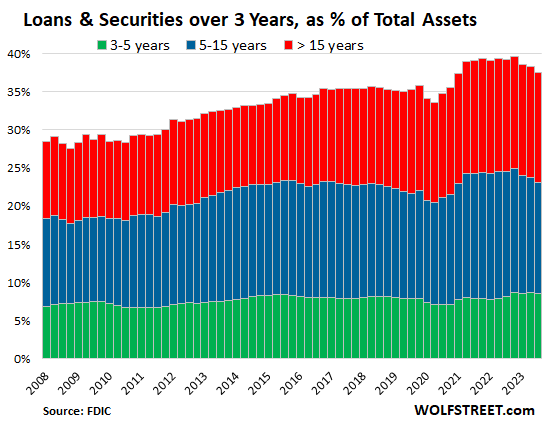

Loans and securities with a remaining maturity of:

- Over 15 years = 14.4% of total assets, lowest since Q1 2021.

- 5-15 years = 14.5% of total assets, lowest since Q4 2020.

- 3-5 years = 8.6% of total assets, roughly stable.

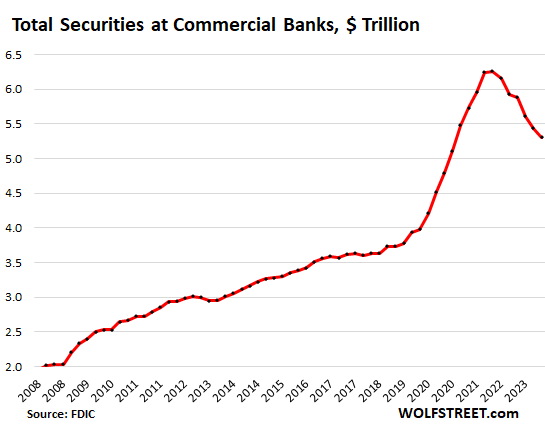

The total pile of securities held by all commercial banks fell to $5.3 trillion at the end of Q3, down by nearly $1 trillion from the peak in Q1 2022, when the Fed’s rate hikes began. They include securities valued at market price and securities valued at purchase price.

Several factors make up the decline, including:

- Securities of the collapsed banks that the FDIC sold to non-banks are no longer part of this.

- Banks have written down AFS securities to market value.

- Banks may have sold some securities.

The $684 billion in unrealized losses above amount to about 13% of the total securities held by banks.

The chart also shows how banks gorged on securities during mega-QE, at the worst possible time just when yields were at historic lows, stimulated by the Fed’s forward guidance at the time of no rate hikes for years to come, even in 2021, as inflation was surging. “We’re not even thinking about thinking about hiking,” Powell had infamously said less than a year before kicking off the fastest rate hikes in 40 years and the biggest QT ever. As has been proven now beyond a reasonable doubt, easy money is like a virus that turns brains to mush.

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the beer and iced-tea mug to find out how:

Would you like to be notified via email when WOLF STREET publishes a new article? Sign up here.

![]()

[ad_2]

Source link

Jeff Clark: The Coming M&A Boom- How Can Investors Profit?

‘The worst is yet to come’: the curse of high inflation