Gold back in the spotlight thanks to debt, dollars and interest rates

“It may surprise many investors to see gold surge as inflation apparently cools, but some believe the precious metal is getting a lift from the prospect of falling US interest rates in 2024, especially since markets are now pricing in four or even five 0.25% reductions from the US Federal Reserve next year,” says AJ Bell investment director Russ Mould.

“Lower rates reduce the opportunity costs of holding gold – which generates no yield (and must be stored and insured) – and could also weigh on the dollar, which is traditionally seen as a boost for gold. However, the most important factor behind gold’s latest attempt to break above and away from the $2,000 mark is a much longer-running one, namely debt, and especially the ongoing increase in America’s federal deficit.

“America’s latest annual fiscal deficit was $1.7 trillion in the year to September 2023, the third-worst number on record, behind the covid-19-afflicted years of 2020 and 2021. While the US will not default, it will keep raising the debt ceiling and possibly have to print more money so it can do so, especially as the annualised interest bill now stands at $1 trillion and counting.

Source: FRED – St. Louis Federal Reserve database, Congressional Budget Office, LSEG Datastream

“America cannot afford to keep interest rates where they are for long and there is a risk that the Fed has to cut rates to keep the burden manageable and take risks with inflation (or even let inflation help salt down the debt/GDP ratio, if interest rates are kept below nominal GDP growth for long enough).

Source: LSEG Datastream data, FRED – St. Louis Federal Reserve database

“Gold bugs will be on the look-out for any signs of higher spending and higher deficits as justification for their faith in the precious metal as a store of value at a time of fiscal incontinence and after an extended period of money printing.

“The US Federal Reserve, Bank of England and European Central Bank are trying to stick with Quantitative Tightening and sterilise some of the trillions they conjured out of thin air in the wake of the Great Financial Crisis, the European Debt Crisis and the covid-19 outbreak. But financial markets are already showing the strain of that. Gold last touched $2,000 an ounce in spring after blow-ups in cryptocurrencies, gilts and then American and Swiss banks, to name but three.

“Moreover, the US continues to spend more than it generates in tax, even when the economy is strong. This begs the question of what could happen if the economy unexpectedly slides into recession and stock market expectations of a soft landing prove misplaced. Under such circumstances, the US tax income would fall and welfare spending would rise, to further increase an already bloated annual deficit.

“Getting the world to buy US Treasuries in the face of such an onrush of supply could be difficult, at least with yields where they are right now and victory over inflation far from certain.

“That could help force a halt to Quantitative Tightening and central banks’ efforts to run down their bond holdings and reduce their bloated balance sheets. Whether it forces them to return to Quantitative Easing and efforts to suppress bond yields and borrowing costs remains a point for debate.

“But central banks’ appetite for US Treasuries as a haven or store of value seems to be waning.

“In 2022 central banks themselves globally bought the most amount of gold since 1967 at 1,136 tonnes, according to the World Gold Council. That buying has continued in 2023. World Gold Council data shows that central banks bought 800 tonnes of gold in the first nine months of 2023, a record amount for the January-to-September period and 14% more than in the first nine months of 2022.

“China is the biggest buyer by some distance, at 181 tonnes so far in 2023, followed by Poland and Singapore.

“Fans of gold will suggest this buying of gold by central banks themselves is a clue, and they will also point to ongoing merger and acquisition (M&A) activity among gold miners, with the closure of Newmont Corporation’s all-stock offer for fellow gold digger Newcrest Mining in November.

“Whenever a major piece of M&A activity is announced, the single most important items of information are the price paid and the valuation implied. This is because they can determine whether the buyers or potential sellers are getting the better part of the deal and also whether the shares of peers in the same industry or sector are looking cheap or not.

“The gold mining industry has been busy in this respect. Barrick Gold swallowed up Randgold Resources and Newmont snapped up GoldCorp in 2019, while Agnico-Eagle and Kirkland Lake Gold merged in 2021 and Agnico-Eagle and Pan American Silver have just finished buying and divvying up Yamana Gold. Among the few remaining UK gold miners, Chaarat Gold took a look at Shanta Gold last autumn and although nothing came of that it did suggest that someone, somewhere thought there was value on offer.

“Sceptics will dismiss this as an attempt to manufacture growth and momentum where little or none exists, since gold output only grows slowly and the all-in sustained cost (AISC) of producing gold is rising, in no small part due to surging energy and staff costs (trends which rather dent gold miners’ perceived status as a hedge against inflation).

“Gold bugs, however, will argue that the proposed Newmont-Newcrest deal is simply further evidence that gold company executives see value that the stock market is overlooking. The price of gold is up by 33% since the start of 2020 but the NYSE Arca Gold Bugs index, known as the HUI, is down by 3% over the same period.

Source: LSEG Datastream data

“Newmont’s all-paper offer put a price tag of $19.5 billion on Newcrest. That was the equivalent of 1.7 times historic book, or net asset value. The major, US-listed producers trade on 1.3 times and London market’s gold diggers a similar multiple.

Source: Company accounts, Marketscreener, consensus analysts’ forecasts

Source: Company accounts, Marketscreener, consensus analysts’ forecasts

“In many cases, the US-listed miners and producers do look to offer greater scale (and lower all-in sustained production costs) than their UK-listed equivalents, but the relative valuations do look to reflect at least partly that, and also the differing jurisdictions in which the miners operate. It is also possible to argue that junior miners can offer greater leverage into any upside in gold prices.

“Not everyone will be convinced. Many will share Warren Buffett’s opinion that gold is an inert, useless lump which an alien invader would dismiss as worthless were they to trip over an ingot upon their arrival from outer space. At best, those in agreement will be prepared to accept that gold could be worth what it costs to get it out of the ground – around $1,200 an ounce, based on the all-in sustained cost (AISC) at the world’s largest quoted gold miner, Newmont Corporation, in 2022.

“That is some 40% below the current gold spot price and may explain to some degree why gold has underperformed equities so badly, even if inflation has been worrisome and debt has been rising.

“Yet gold has been doing well for some time, as debt has marched higher and fears that ultra-loose monetary policy, money printing and expansive fiscal policy lead to some degree of inflationary outburst have finally been borne out.

“Gold may only be setting new highs in dollars now, but the gains in yen, sterling and euro are more notable still, and the over the last decade, gold has beaten the FTSE 100, Nikkei 225 and Stoxx Europe 600 hands down in those indices’ local currencies. The S&P 500 has outpaced gold in dollars and that may be why gold gets such a bad rap.

Source: LSEG Datastream

“Bulls will counter by saying that this negative perception means there is still value to be had.

“Gold is still trading toward the lower end of its range relative to global equities (as benchmarked by the FTSE All-World since its inception in 1994), while gold miners are trading at near-historic lows relative to the metal’s price (as benchmarked by the HUI and its inception in 1997).”

Source: LSEG Datastream data

These articles are for information purposes only and are not a personal recommendation or advice.

[ad_2]

Source link

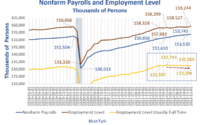

December Jobs: Employment Rises by 717,000 All of Them Part Time – Mish Talk

Deflation Looms for Overstocked Retailers as Household Wealth Shrinks