Goldilocks: Jobs Rise 199K, Beating Estimates As Striking Workers Return; Unemployment Rate Drops

Ahead of today’s jobs report (which we previewed as being focused mostly on the unemployment rate), we said that the whisper was for a stronger report due to the mandatory political talking points for the White House taking credit for all those strikers coming back to work…

Whisper is stronger number due to impact of strikers returning to work and required political talking points

— zerohedge (@zerohedge) December 8, 2023

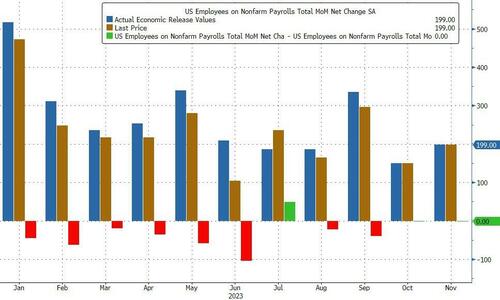

… and lo and behold, that’s precisely what happened, with the total number of job gains in November coming in at 199K, above last month’s 150K and, more importantly, well above the consensus forecast of 183K.

This number included about 47K formerly striking auto and motion picture workers (see below for details).The BLS noted that “job gains occurred in health care and government. Employment also increased in manufacturing, reflecting the return of workers from a strike”, which as we noted above will be today’s White House main talking point. Still as Omair Sharif, founder of Inflation Insights LLC, notes, “if you strip out the strike impact, over the last two months, private payrolls averaged 118,000. That compares with a six-month average of 130,000. So the direction of travel is weaker. The pace is “relatively soft” and will probably be welcomed by the Fed.”

Of course, as has been the case every month this year, previous months’ data was revised lower, with September down by 35K from 297K to 262K and October remaining flat at 150K (the BLS is getting a little “shy” of all these downward revisions taking place the next month) and will instead be revised lower in January. So expect today’s “beat” to be revised to a miss next month… when it won’t matter.

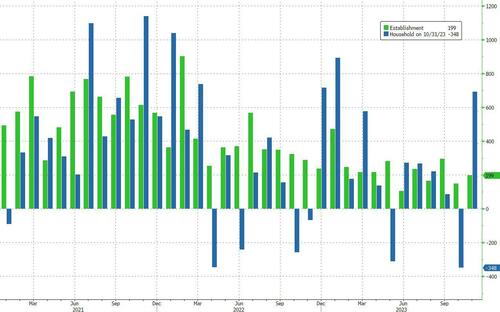

Still, the number was solid especially when considering that the number of employed workers as counted by the Household survey surged by 747K to 161.969 million, following several months of disappointing prints, including last month’s 348K drop, and rising to the highest on record. This was the third biggest increase in the Household survey this year.

But more importantly, recall that as we explained in our preview, a 4.0% unemployment rate after last month’s 3.9% would have triggered the popular “Sahm’s rule” recession indicator (which is why there was more attention on the unemp rate than even the NFP number), and sure enough the BLS reported that the unemployment rate actually dipped 3.7%, well below the estimate of 3.9%.

The drop in the unemp rate was thanks to the abovementioned jump in employed workers, which surged by 747K to 162 million, as well as the increase in the participation rate, which rose to 62.8%…

… while the number of unemployed workers actually dropped by 215K, to 6.3 million.

Turning the wages, the monthly increase was slightly higher than expected as average hourly earnings for all employees rose by 12 cents, or 0.4% to $34.10, higher than the 0.3% expected with only 3 out of 62 forecasts in the Bloomberg survey calling for a 0.4% gain in average hourly earnings. Everybody else was slower than that. Over the past 12 months, average hourly earnings increased by 4.0%, in line with expectations and unchanged from the downward revised 4.0% in October. At the same time, average hourly earnings of private-sector production and nonsupervisory employees rose by 12 cents, or 0.4 percent, to $29.30.

Some more details from the jobs report:

- The number of persons employed part time for economic reasons decreased by 295,000 to 4.0 million in November. These individuals, who would have preferred full-time employment, were working part time because their hours had been reduced or they were unable to find full-time jobs.

- In November, the number of persons not in the labor force who currently want a job was 5.3 million, little different from the prior month. These individuals were not counted as unemployed because they were not actively looking for work during the 4 weeks preceding the survey or were unavailable to take a job.

- Among those not in the labor force who wanted a job, the number of persons marginally attached to the labor force changed little at 1.6 million in November. These individuals wanted and were available for work and had looked for a job sometime in the prior 12 months but had not looked for work in the 4 weeks preceding the survey. The number of discouraged workers, a subset of the marginally attached who believed that no jobs were available for them, was 421,000 in November, essentially unchanged from the previous month.

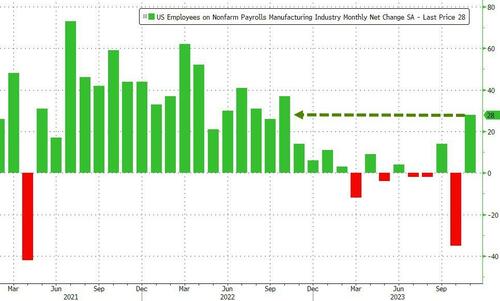

Looking at the composition of jobs, the big highlight is that manufacturing payrolls rose 28k after falling 35k in the prior month, reflecting the return of workers from a strike.

A closer look at other industries reveals the following:

- In November, health care added 77,000 jobs, above the average monthly gain of 54,000 over the prior 12 months. Over the month, job gains continued in ambulatory health care services (+36,000), hospitals (+24,000), and nursing and residential care facilities (+17,000).

- Government employment increased by 49,000 in November, in line with the average monthly gain of 55,000 over the prior 12 months. Employment continued to trend up in local government (+32,000) and state government (+17,000) over the month.

- Employment in manufacturing rose by 28,000 in November, reflecting an increase of 30,000 in motor vehicles and parts as workers returned from a strike.

- In November, employment in leisure and hospitality continued to trend up (+40,000), almost entirely in food services and drinking places. This is amusing considering ADP reported just the opposite.

- Employment in social assistance continued to trend up in November (+16,000). The industry had added an average of 23,000 jobs per month over the prior 12 months. Over the month, employment continued to trend up in individual and family services (+9,000).

- Retail trade employment declined by 38,000 in November and has shown little net change over the year. Employment decreased in department stores (-19,000) and in furniture, home furnishings, electronics, and appliance retailers (-6,000) over the month.

- In November, employment in information changed little (+10,000). Motion picture and sound recording industries added 17,000 jobs, mostly reflecting the resolution of labor disputes in the industry. Overall, employment in the information industry has declined by 104,000 since reaching a peak in November 2022.

- Employment in transportation and warehousing changed little in November (-5,000). A job loss in warehousing and storage (-8,000) was partially offset by a gain in air transportation (+4,000). Employment in transportation and warehousing has declined by 61,000 since a peak in October 2022.

Employment showed little change over the month in other major industries, including mining, quarrying, and oil and gas extraction; construction; wholesale trade; financial activities; professional and business services; and other services.

According to Bloomberg, payroll gains this month were broader than in October. The diffusion index — which measures how many industries are hiring — rose to 63.4% last month from 52.2% in October.

Commenting on the report, Wall Street was generally happy with the numbers:

- Dominic Konstam, head of macro strategy at Mizuho Securities: “Clearly the early Fed easing cycle risk is put back and the labor market is slowing, is well off strength in early 2023, but not the extreme weakness seen in October.”

- Priya Misra, portfolio manager at JP Morgan Investment Management: “Strong number, solid wages and higher participation should keep the soft landing narrative alive. We knew that strikes would add to this number. Some of the near-term Fed rate cuts will get taken out but we think people will buy the dip. Not many had the opportunity to buy 10y Treasuries at 5% but even 4.25% is not a bad level heading into a slowing growth and inflation world. Good number for risk assets.”

- Ira Jersey, Bloomberg Intel rates strategist: “The better-than-expected employment report may cause the market to price out some early-2024 rate cuts and bear flatten the yield curve. Next week’s CPI will be needed for confirmation, but unless core CPI falls a lot, we think perhaps the bottom of a near-term yield range has been set about 4.1% on the 10-year Treasury.”

- Dennis DeBusschere, founder of 22V Research: “too strong on the day across the board. Not a disaster at all for markets though. Clearly rates are highly unlikely to move much lower from here given the payroll data. That being said, it is not a done deal that the Fed needs to push back aggressively against the recent FCI easing. If CPI still trends lower, one stronger-than-expected payroll report is not an issue. A bunch of strong payroll reports and wages staying at current levels would be a clear issue.”

- Omair Sharif, founder of Inflation Insights LLC: “if you strip out the strike impact, over the last two months, private payrolls averaged 118,000. That compares with a six-month average of 130,000. So the direction of travel is weaker. The pace is “relatively soft” and will probably be welcomed by the Fed.”

- Ali Jaffery, economist at CIBC Capital Markets: “Today’s report will certainly raise some eyebrows in the FOMC and is a reminder that the labor market remains tight. But with inflation persistence less of a challenge, the Fed will continue to remain patient.”

- Ana Galvao, Bloomberg economics: “The drop in the unemployment rate was unexpected, but once the dust settles Bloomberg Economics’ Macro-Finance SHOK tool, suggests the impact on yield forecasts will be muted. The model shows an upward move in 10-year Treasury yields of less than 1 basis point over the medium term.”

- Alan Ruskin, chief international strategist at Deutsche Bank: “3mo averages of private NFP are quite stable, consistent with growth down a notch but no major deceleration. Three-month annualized measures of aggregate hours worked are very steady, consistent with the idea that underlying growth is more stable rather than decelerating significantly…. The data definitely works with rhetoric that the tightening cycle may not be over, even if this is regarded as unlikely, and that it is premature for officials to be talking about easing. In short, the data extends the likelihood of a longer than usual plateau in rates.””

- BMO Capital Markets’ Ian Lyngen: “Overall, it was a strong report that has predictably reduced the odds of a March hike to <50% territory.”

- Rubeela Farooqi, chief US economist at High Frequency Economics: “In terms of Fed policy, we do not think these data change the outlook; rates are at a peak and the Fed’s next move will be a rate cut, likely by the middle of next year.”

- Neil Dutta of Renaissance Macro Research: “The US labor markets are fine. November’s employment figures were firmer than expected and as a result, bond yields are rising. (People saying recession need to have their heads examined). However, in our view, the labor market is not the primary driver for monetary policy right now. Indeed, there is an asymmetry in the Fed’s policy reaction function: stronger employment will not push them away from a cut as much as weaker inflation will push them towards one. The solid economy puts a ceiling on how many cuts we’ll get, but it will not stop cuts altogether. That’s what a recalibration of policy is about.”

- UBS strategist Simon Penn: “Fed’s Powell Can’t Be Anything Other Than Hawkish. Fed Chair Powell’s message next week is going to have to reference: the continued strength of the labor market, the continued strength of wage growth, and the persistence of inflation (core CPI is likely to print 4.0% on the first day of the FOMC meeting).Meanwhile, the decline in yields since November’s meeting rather undermines the prior argument of yields being a form of financial tightening.It is hard to find the circumstances under which Powell says anything other than: It’s far too early to think about cuts; policy will need to remain restrictive; inflation remains well above target; the Fed will need to see a period of sub-trend growth.Relative to the pricing markets have talked themselves into, that’s all going to sound pretty hawkish.”

Finally, the number is largely in line with Goldman’s market reaction matrix sweet spot:

- >250k S&P sells off at least 50bps

- 200k – 250k S&P sells off 25 – 50bps

- 150k – 200 S&P + / – 25bps

- 50k – 150k S&P rallies 100+bps

- <50k S&P sells off at least 50bps

And with payrolls largely a non-event (especially after this week’s dismal labor market reports) attention now turns to next week’s CPI report.

Loading…

[ad_2]

Source link

The Real Threat to Dollar Dominance

The Fed Can’t Win: SchiffGold Friday Gold Wrap Dec. 30, 2022