These Crazy Rallies on Hawkish Fed Plans Are Good Because Crashing Stocks & Seizing Credit Markets Would Cause the Fed to Wobble in its Inflation Crackdown

There was a time when markets tried to force the Fed’s hand by crashing. Now markets are enabling the most hawkish Fed in 40 years.

By Wolf Richter for WOLF STREET.

It was an amazing show today – how markets reacted to headlines that exuded “dovish” somehow after Fed Chair Jerome Powell, speaking at the Brookings Institution, hit all the hawkish buttons: likely a 50-basis-point rate hike at the December meeting, to 4.5% at the top end of the range for the federal funds rate, then more rate hikes (plural) next year, to a higher “ultimate level” even than projected during the shocker September meeting when the Fed had issued projections that the upper end of the federal funds rate target might hit 4.5% by December, and 4.75% or 5.0% by the end of 2023, far higher than expected.

But Powell moved the “ultimate level” even higher today than the projections in September. He said, “it seems to me likely that the ultimate level of rates will need to be somewhat higher than thought at the time of the September meeting.”

“It is likely that restoring price stability will require holding policy at a restrictive level for some time. History cautions strongly against prematurely loosening policy. We will stay the course until the job is done,” he said.

Other Fed governors spoke before him this week, and they agreed with Powell: Even higher than projected at the shocker September meeting, and keeping it there for even longer. The range is 5% to 7%, according to Bullard, and Powell today moved into that range.

Just about everything in the speech was hawkish, including Powell’s frustration that core PCE inflation hasn’t come down over the past 12 months, that it has “mainly moved sideways.”

“Despite the tighter policy and slower growth over the past year, we have not seen clear progress on slowing inflation,” he said.

“So when will inflation come down?” he asked.

He cited the forecasts of declining inflation and added, “But forecasts have been predicting just such a decline for more than a year, while inflation has moved stubbornly sideways.”

“For starters, we need to raise interest rates to a level that is sufficiently restrictive to return inflation to 2 percent,” he said.

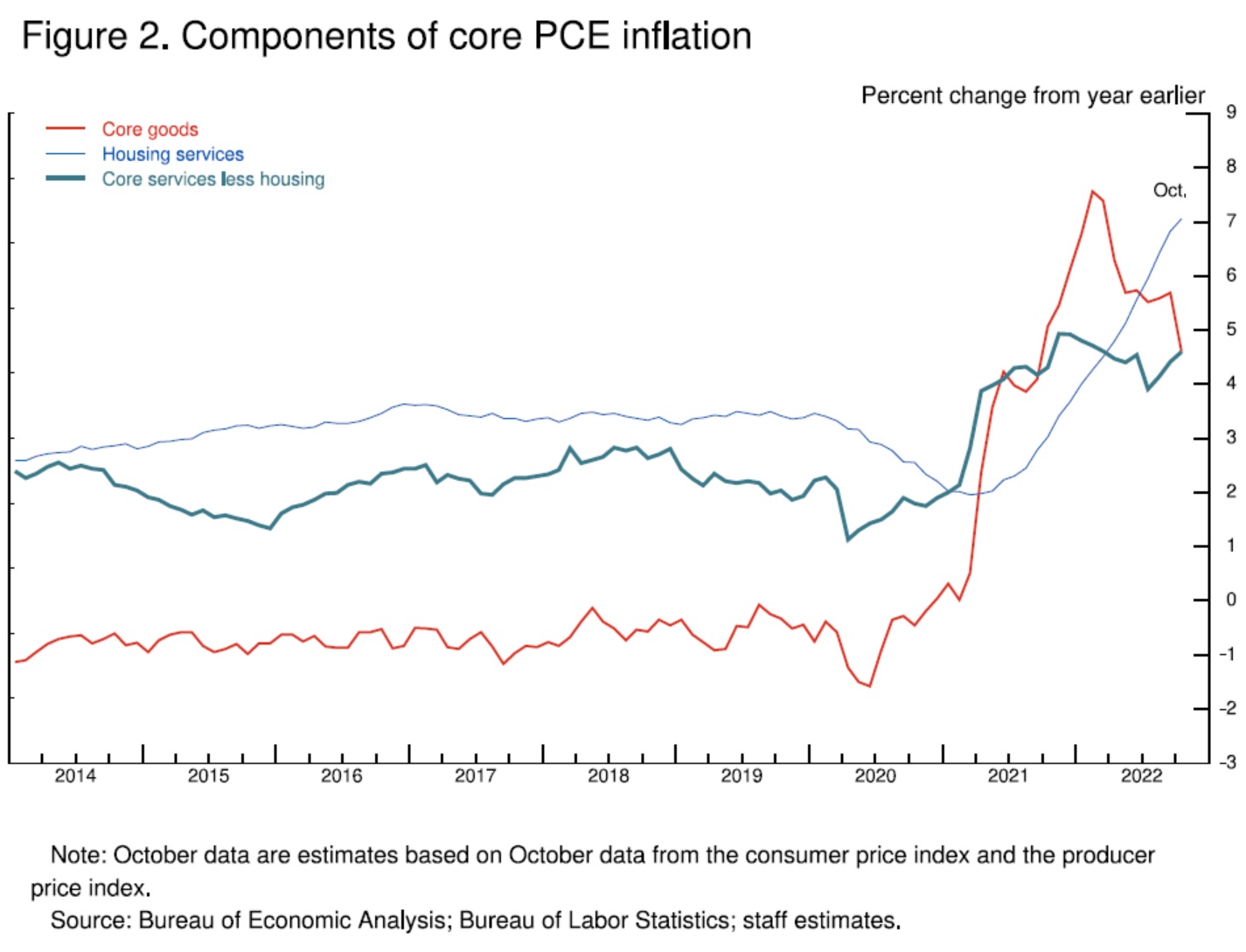

He spent a good amount of time on analyzing what might cause core inflation, as measured by the core PCE price index, to refuse to fall in 2023, even as inflation in core goods is backing off: housing inflation and inflation in “core services less housing.”

He expects housing services inflation (rents) to continue rising “well into” 2023. But his bigger concern was inflation in “core services less housing.”

Core services less housing account for more than half of the core PCE price index; it’s insurance, healthcare, education, haircuts, auto repairs, hospitality, etc. And core services inflation has risen in recent months. “This may be the most important category for understanding the future evolution of core inflation,” he said.

“Because wages make up the largest cost in delivering these services, the labor market holds the key to understanding inflation in this category,” he said.

He provided this chart, showing the three categories of the core PCE price index:

- Core goods (red line) where inflation has backed off from the spike

- Housing services (thin blue line) that continued to surge

- Core services less housing (fat green line):

Given how important wage increases are to inflation in “core services without housing,” he discussed the labor market. And the labor market is still too hot. He cited the figures we’ve been looking at in amazement for months.

“In the labor market, demand for workers far exceeds the supply of available workers, and nominal wages have been growing at a pace well above what would be consistent with 2 percent inflation over time,” he said.

“Thus, another condition we are looking for is the restoration of balance between supply and demand in the labor market,” he said.

“For the near term, a moderation of labor demand growth will be required to restore balance to the labor market,” he said.

“Wage growth, too, shows only tentative signs of returning to balance. Some measures of wage growth have ticked down recently. But the declines are very modest so far relative to earlier increases and still leave wage growth well above levels consistent with 2 percent inflation over time,” he said.

“To be clear, strong wage growth is a good thing. But for wage growth to be sustainable, it needs to be consistent with 2 percent inflation,” he said.

So Powell and the Fed governors are largely speaking in unison: Rates will have to go even higher than projected during the shocker September meeting; they will have to stay there longer; and rates will need to rise enough to where the real federal funds rate (federal funds rate minus core PCE rate) will be positive.

And fireworks broke out on Wall Street.

The S&P 500 jumped 3.1%, the Nasdaq jumped 4.4%, the 10-year Treasury yield – hilariously, on hearing that rates will have to go higher and stay higher for longer – plunged 17 basis points. And all this was dressed up in a headline that exuded “dovish” somehow. It was quite a show.

But think of it this way: When financial conditions loosen, as they did today, the Fed is going to have to raise higher and keep it there longer because monetary policy works through tightening financial conditions, and for inflation to come down, financial conditions have to tighten, not loosen.

I mean, markets are shooting themselves into the foot with these rallies, and Powell knows this too. Let them, he’s thinking while raising to 4.5% in December and to 5% and even higher next year, which no one had envisioned a year ago.

These crazy rallies are a good thing.

The last thing we need is a crash that would cause the Fed to wobble in its determination to crack down on inflation. These rallies will keep QT going, and they will keep the rate hikes coming, and they will keep the Fed focused on inflation instead of having to deal with a market meltdown.

There was a time when markets tried to force the Fed’s hand by spiraling down. Now markets, with these sporadic rallies, are supporting the Fed’s crackdown, and they’re enabling the most hawkish Fed in 40 years to keep going.

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the beer and iced-tea mug to find out how:

Would you like to be notified via email when WOLF STREET publishes a new article? Sign up here.

![]()

[ad_2]

Source link

Morgan Stanley’s Shalett Sees ‘Massive Disconnects’ in Stocks

The commodity supercycle is still young, these strategists say.