Westfield Walks from Mall in San Francisco, after Walking from 2 Malls in Florida & others. Screws CMBS Holders, Said in 2021 it’ll Dump All Malls, but Suddenly Blames San Francisco?

Default rate of mall CMBS rose to 7%. Simon Property Group, largest mall landlord, walked from malls for years. Tens of thousands of stores closed. Ecommerce is killing them one by one, not San Francisco.

By Wolf Richter for WOLF STREET.

Back in February 2021, we reported that Unibail-Rodamco-Westfield (URW), the largest property REIT in Europe, had announced that it would dump all its 27 Westfield malls in the US, of which 16 were in California, including the Westfield San Francisco Center. URW had acquired them in 2018 from Australian mall operator Westfield.

Since 2017, I’ve been documenting what I call the brick-and-mortar meltdown in the US, driven by ecommerce, because everything you can buy at the mall, you can buy online, except online, they have everything, and at the mall they don’t. But these morons in Europe didn’t read my stuff, and didn’t know about the brick-and-mortar meltdown in the US. The Australians however did, and they dumped those US malls while they could.

In February 2021, we also reported that these morons at URW had lost €7.6 billion in 2020, after large write-downs of its malls, that URW was buckling under €32 billion in debt, thanks to that Westfield purchase, and that its net rental income had plunged by 28%, and that it axed its dividend, and that it tried to raise funds with a €3.5 billion rights issue, which failed.

By that time, its US unit, Westfield Group, had already started defaulting on its mall loans.

In late 2020, Westfield walked away from two Tampa Bay, Florida, malls – the Westfield Citrus Park and the Countryside Mall. The combined interest-only $278 million of mortgages had been securitized into commercial mortgage-backed securities (CMBS) that had been sold to bond funds and pension funds and whatever. And Westfield walked away from those two malls in Florida and let the CMBS holders eat the losses.

When Westfield walked from those malls, their ownership changed from Westfield to the holders of the CMBS, who are represented by a “special servicer.” Foreclosing on the properties was the only recourse CMBS holders had.

In August 2021, Westfield walked away from the 1-million sq. ft. Westfield Palm Desert Mall in Palm Desert, California. A 575,000-square-foot portion of the mall, not including the anchor stores, served as collateral for a $125 million interest-only mortgage that was securitized in 2014 into CMBS and sold to bond funds and pension funds and whoever. At the time, Wall Street had that portion of the mall appraised at $212 million. By August 2021, it wasn’t worth the loan amount of $125 million?

And so Westfield Group dumped mall after mall, selling some, walking away from others, screwing CMBS holders along the way. And now it’s finally the turn of Westfield San Francisco Center, which it co-owns with Brookfield Asset Management.

A portion of the Westfield San Francisco Center is collateral for, you guessed it, an interest-only $558 million 10-year mortgage that was securitized in 2016 and sold to bond funds, etc.

Malls in the US are in horrible shape. Ecommerce is killing them.

Westfield is in good company: The largest mall landlord in the US, Simon Property Group (SPG) defaulted on and walked away from overindebted malls across the US, no problem, including the 170-store 1.2-million-square-foot Town Center at Cobb in Georgia in early 2021, the 1.1-million-square-foot Montgomery Mall in North Wales, Pennsylvania in mid-2021, and even in 2019, the 1-million-square-foot Independence Center in a suburb of Kansas City, Missouri, which generated what was then the largest loss ever by a retail CMBS loan.

Three publicly traded US mall REITs have filed for bankruptcy since November 2020: the SPG’s spinoff, Washington Prime Group, CBL & Associates Properties, and Pennsylvania Real Estate Investment Trust. And there are zombie malls everywhere across the US.

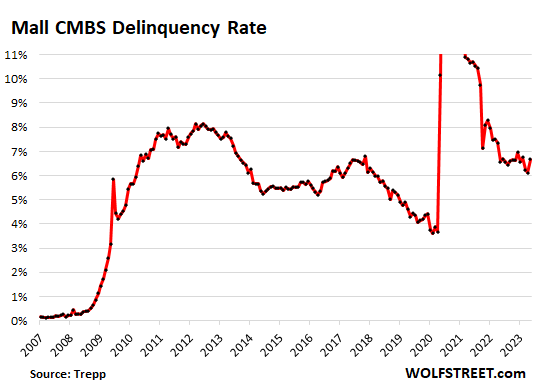

Retail CMBS have had enormous default rates for years. In May, the default rate rose to 6.7%, according to data by Trepp, which tracks CMBS. Retail CMBS are by far the worst of the CMBS categories, far worse than the next worst in line, lodging (4.3%) and Office, which we discuss a lot here at 4.0%:

As so many malls, Westfield San Francisco Center lost one of the anchor stores, Nordstrom.

Nordstrom has been closing lots of stores for years around the country even before the pandemic, like all department stores that are still alive, and the many that aren’t. But when it finally closed two stores in San Francisco, and blamed “the dynamics of the downtown San Francisco market,” rather than its own failure to compete with ecommerce, it became a national clickbait headline circus.

Brick and mortar retail has lost the battle against ecommerce, and more and more retailers will be taken out.

An endless number of retailers, from Sears Holdings and Toys ‘R’ Us on down to Bed, Bath & Beyond filed for bankruptcy and most of them vanished. All regional and nearly all national department store chains filed for bankruptcy and vanished. There are just a few left, including Nordstrom, Kohl’s, and Macy’s.

Macy’s closed hundreds of stores over the years and continues to close stores. J.C. Penney, which finally filed for bankruptcy in 2020, was bought out of bankruptcy by SPG and Brookfield, because they didn’t want shuttered anchor stores doom their malls.

When Nordstrom announced that it would close the two stores in San Francisco, Westfield blamed in part “unsafe conditions” and “lack of enforcement against rampant criminal activity.”

In reality, ecommerce and retail executives’ inability to figure out how to compete with ecommerce have been the real enemy that has been killing mall after mall. Neither Nordstrom nor Westfield blamed their own executives and ecommerce for the failures across the US. They blamed San Francisco, which stimulates the braindead media circus that covers up their own failures.

Nordstrom has a large ecommerce business, and that’s doing fairly well, but its brick-and-mortar stores are doomed. That’s just how it is. And malls are doomed. They have been obviated by the big change in how Americans shop. Ecommerce is turning malls into dead meat, one by one. And San Francisco is the epicenter of ecommerce.

The other big mall in San Francisco, Stonestown Galleria, is being redeveloped by owner Brookfield; it’s adding nearly 3,000 housing units and parks to the retail spaces, at a cost of $2 billion. That’s the future of malls.

But the bitter reality of how ecommerce has been crushing brick-and-mortar retail – and particularly department stores – for years doesn’t make clickbait headlines in the fantasy media circus.

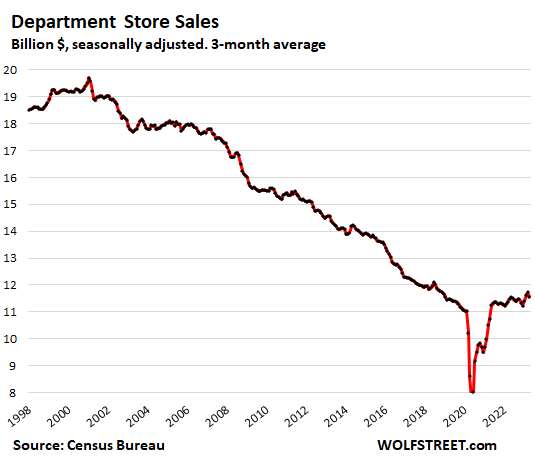

For your amusement, department store brick-and-mortar sales since 1998. That’s where Nordstrom’s brick-and-mortar store are. Do you see what the problem is? It’s not San Francisco:

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the beer and iced-tea mug to find out how:

Would you like to be notified via email when WOLF STREET publishes a new article? Sign up here.

![]()

[ad_2]

Source link

Financial instability: the hunt for the next market fracture

Regional banks face hit from new debt level requirements