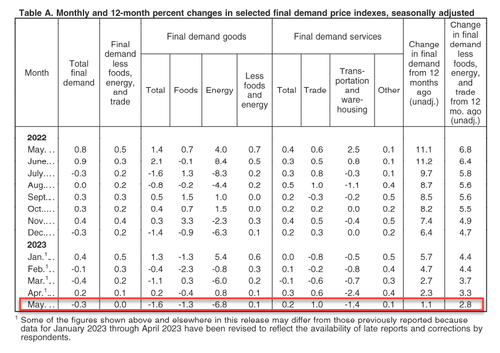

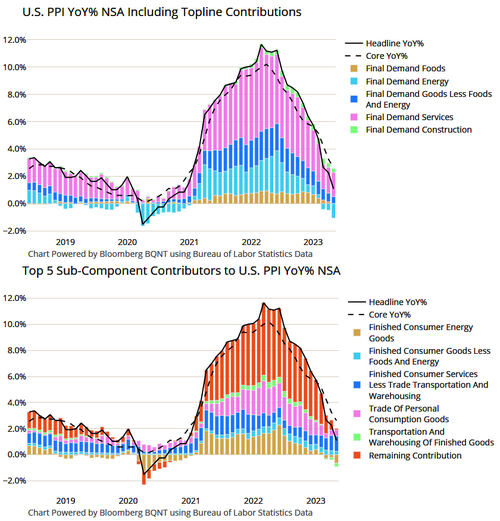

PPI Plunges More Than Expected – Lowest Since Dec 2020

After a mixed picture from CPI data yesterday (headline down big, core still sticky, supercore rising), PPI was expected to continue to decline in data this morning for May, and it did bigly… Headline PPI fell 0.3% MoM in May (way more than the 0.1% drop expected), which dragged the YoY PPI to just 1.1%. That is the lowest since Dec 2020…

Source: Bloomberg

Under the hood, Goods PPI tumbled 1.6% while Services rose just 0.2%…

Sixty percent of the May decline in the index for final demand goods can be traced to a 13.8-percent drop in prices for gasoline.

The indexes for diesel fuel, chicken eggs, jet fuel, fresh and dry vegetables, and iron and steel scrap also fell. Conversely, prices for tobacco products advanced 1.7 percent. The indexes for electric power and for beverages and beverage materials also increased.

Over 40 percent of the May increase in prices for final demand services can be attributed to margins for automobiles and automobile parts retailing, which rose 4.2 percent.

The indexes for fuels and lubricants retailing; apparel, footwear, and accessories retailing; securities brokerage, dealing, investment advice, and related services; machinery and vehicle wholesaling; and food wholesaling also advanced. Conversely, prices for truck transportation of freight fell 2.1 percent. The indexes for portfolio management and for health, beauty, and optical goods retailing also decreased.

Core PPI was unchanged MoM, dragging the YoY change to +2.8% – the lowest since Feb 2021…

Source: Bloomberg

The pipeline for PPI is also increasingly deflationary as prices for intermediate demand goods plunge…

Source: Bloomberg

Finally, M2 suggests this re-acceleration of the deflationary impulse in PPI is set to continue aggressively…

Source: Bloomberg

The question is – does The Fed care about PPI? Or just its latest SuperCore CPI as an inflation ‘signal’?

Finally, we note the following trend – is this the new economy?

Drink more, drive less?

Loading…

[ad_2]

Source link

Fed ‘Flying Blind’ Into ‘Ugly’ Recession in 2024, Only This Will Make Powell Pivot, Hanke: Video

Billionaire investor Carl Icahn says Russia’s invasion of Ukraine isn’t as big a deal for markets as inflation